- Date:

- Author:

- Stefan Gerlach

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

CPI inflation in Switzerland remains too high and the Swiss National Bank is concerned: inflation at 2.2% in May is above the 0-2% interval that the SNB regards as price stability. The public is also uneasy with inflation at such a level. In response, the SNB has been raising interest rates since June 2022. In this edition of Infocus, EFG chief economist Stefan Gerlach looks at past rates and considers future moves by the SNB.

Inflation in Switzerland

Many central banks pay great attention to measures of underlying, or core, inflation. It can be measured in various ways. The Federal Reserve has an objective of 2% inflation as captured by the deflator for personal consumption expenditures. However, in setting policy it has historically paid greater attention to a consumption deflator that disregards the highly volatile food and energy components that the Fed sees as introducing noise in the measurement of inflation.

The SNB judges itself by inflation as measured by the overall CPI but pays little attention to core inflation, at least in its public statements. Nevertheless, when analysing Swiss inflation, it makes sense to look at various decompositions of CPI inflation. We do so here.

Core inflation

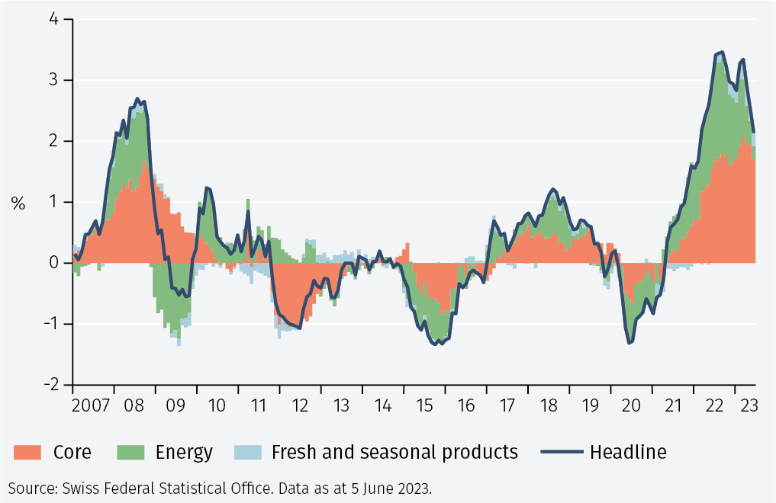

As noted above, the Fed and some other central banks focus on a measure of core inflation that disregards energy and other volatile prices. The Swiss Federal Statistical Office computes a similar measure, which disregards energy and “fresh and seasonal products.”

That measure of core inflation and overall, or ‘headline’, CPI inflation is shown in Figure 1. It shows that although energy prices only have a weight of 6% in the Swiss CPI, they make a large contribution to the fluctuations in overall inflation. Indeed, the graph shows that about half of inflation in 2022 was due to a marked rise in energy prices.

But more importantly, Figure 1 shows that even if the prices of energy and fresh and seasonal products had not risen, inflation in Switzerland would have been 1.7% in May. That is too close to 2% for comfort and suggests that the SNB will tighten monetary policy.

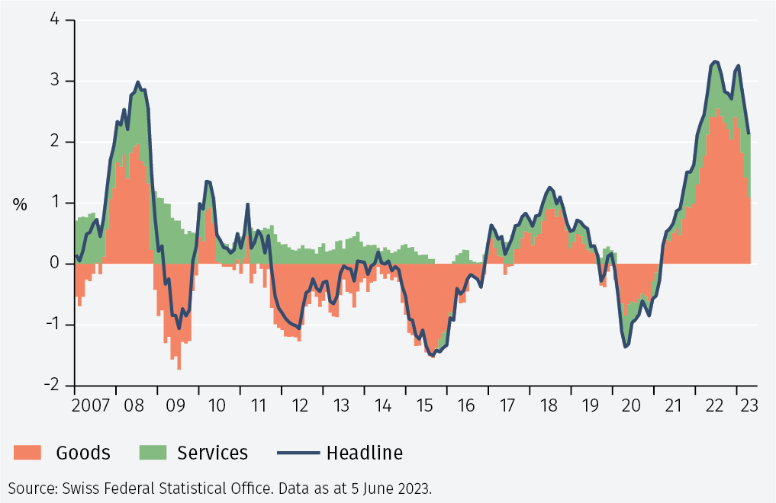

Another way to think about inflation is to make a distinction between goods and services. Goods are often imported and therefore sensitive to exchange rate changes. Because of productivity gains, goods prices are generally stable or falling.

Services, by contrast, are labour intensive, often not traded internationally (although trade in services is becoming increasingly important). Low labour productivity growth, coupled with a lack of international competition means that prices are often set on a cost-plus basis. The result is steady services price inflation generally above the central bank’s inflation objective.

As Figure 2 shows, services price inflation has generally been positive, except for during the spring of 2020 when the start of the Covid pandemic led to a collapse in the demand for contactintensive services.

But looking at recent data, it is striking that more than half of inflation has been due to goods prices. These include the prices of imported oil and related products, which are highly volatile and most central banks agree should not be the focus of policy. Distinguishing between goods and services inflation therefore does not seem particularly helpful at the current juncture.

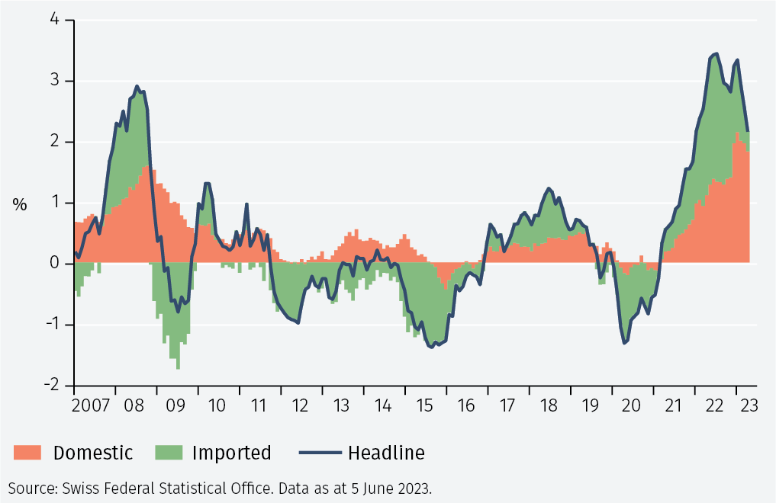

Another way to decompose inflation is to distinguish between domestic and imported prices. Not surprisingly, Figure 3 shows that imported prices have played an important role in the recent increase in inflation. Nevertheless, a large and growing part of that increase is due to domestic prices. Indeed, if imported prices stopped rising, inflation would have been 1.8% in April. Given the SNB’s 0-2% price stability range, that also calls for tighter monetary policy.

Conclusions

Inflation in Switzerland remains above the SNB’s price stability range of 0-2%. That low range reflects the SNB’s long-term focus on achieving and maintaining price stability. But it also reflects other factors that facilitate pursuing a low inflation policy and which now make it easier for the SNB than many other central banks to raise interest rates.

Importantly, the labour market in Switzerland is flexible. Even the surge of the Swiss franc following the abandonment of the exchange rate floor in 2015 had very little impact on unemployment. There are good reasons to believe that the Swiss labour market would endure tighter monetary policy with little problem.

Furthermore, there is solid public support for low inflation, even if that entails raising interest rates. One reason for that is mortgage lending risks appear to be managed very well by the authorities and banks. It seems unlikely that higher interest rates will trigger mortgage defaults.

Similarly, the fact that Switzerland has so little public debt means that higher interest rates have very limited direct impact on public finances. But the indirect impact of higher interest rates on public finances will be large: the flipside of the SNB’s bloated balance sheet is that banks are holding large interest-earning reserves at the SNB. As interest rates rise, banks will earn greater interest income from their reserves and SNB profit transfers to the Confederation and cantons will decline. Indeed, they may well remain at zero for some years to come.

But the SNB’s primary objective is price stability. Tighter monetary policy is called for. Interest rates in Switzerland need to rise to lower inflation from the current level. Expect a 25 bps increase in June, and perhaps another in September. It is also likely that the policy tightening will involve the SNB selling foreign currency, which puts upward pressure on the Swiss franc and dampens imported inflation.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.