- Date:

- Author:

- Stefan Gerlach

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

In January, EFG Chief Investment Officer Moz Afzal and EFG Chief Economist Stefan Gerlach visited Hong Kong and Singapore to present the EFG Outlook 2024. They took the opportunity to meet with market strategists as well as private and public sector economists to better understand the economic problems China is facing. This issue of Infocus provides a synthesis of what they learned in their conversations. It is a mosaic built from the many views expressed and does not reflect the view of any single person.

Introduction

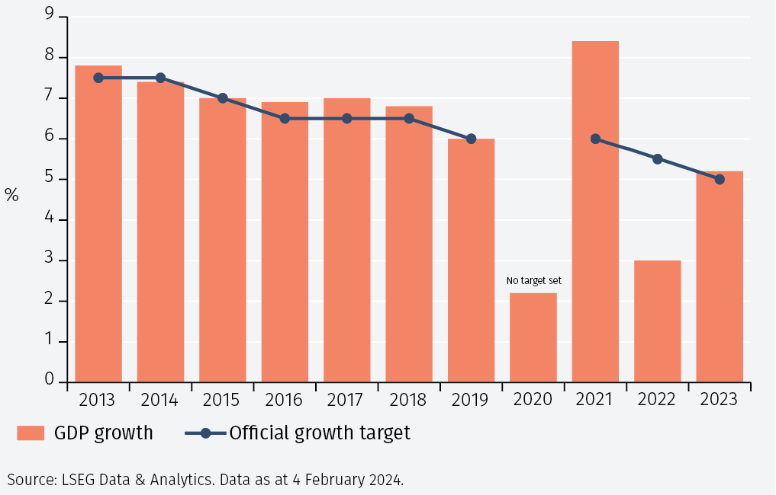

Economic sentiment in China is in the doldrums. The abrupt Covid policy U-turn and the reopening of the economy in late 2022 led only to a brief pickup in economic activity. Stock prices fell sharply in 2023 and difficulties in the property market have reverberated through the economy. While 2024 may be less bumpy for the economy than 2023, real GDP growth is expected to be lower.

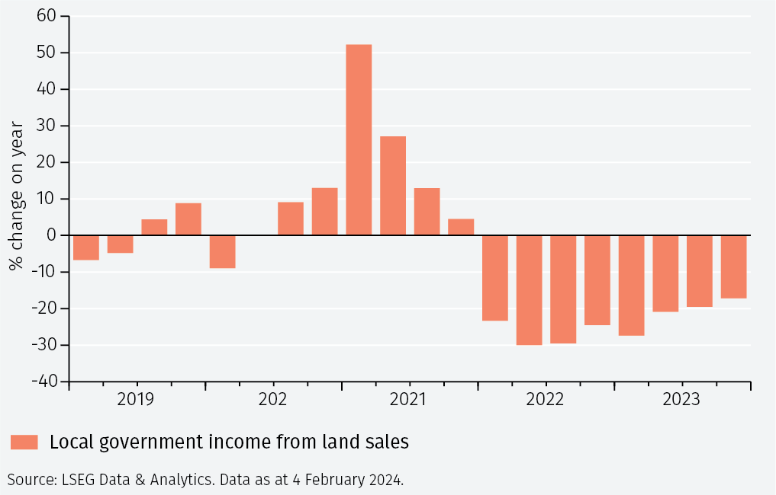

In the past, extensive infrastructure spending - building bridges and roads for which there is little demand - boosted the property market and allowed local governments to sell land at high prices. In response, the private sector took on too much leverage. That cycle has now ended but lingering problems persist relating to prior overinvestment in physical infrastructure and housing.

Declines in property prices have impacted land sales, which are a vital source of revenue for local governments (see Figure 1). This has negatively affected their ability to service the debt of local government enterprises and financial vehicles.

However, the possibility of a complete property market collapse seems remote. The largest banks are state-owned, and the government is trying to stabilise the property market by cutting downpayment ratios, lowering mortgage rates and pushing for the completion of pre-sold flats. In the longer term the shrinking population will reduce housing demand, but this will be offset to some extent by rising income levels and urbanisation.

Despite these problems, in our view the Chinese economy is unlikely to experience a severe downturn. The authorities have many policy levers and, if the economic problems lead to public protests, many commentators believe that the Communist Party would change policy rapidly. Indeed, the avoidance of street protests is seen as a key policy objective.

Politics and the economy

The domestic economic problems are sometimes attributed to a shift away from a market system. Policymakers appear concerned that the free market and the continued growth of the private sector may erode the power of the Communist Party. Moreover, avoiding an increase in inequality and the associated risk of social instability that it could bring is also a key policy objective. China is seen as having difficulty handling social instability because of the lack of a fully democratic system to absorb shocks.

In practice, this shift in the focus of policy has meant that policymaking has been centralised and national security has been prioritised at the cost of economic objectives. Power has shifted away from officials and experts to politicians close to the centre of power with the result that policy institutions, including the People’s Bank of China, have lost influence and independence. While officials are said to have a good understanding of the economic problems and possible solutions, they appear unable to get their views across to the highest political leadership.

As a result, there is a widely held view that current economic policies are not sustainable, but also that the authorities would not hesitate to modify their objectives, even dramatically, if that became necessary to avoid widespread social unrest.

Supporting the domestic economy

The Chinese economy needs a new source of growth. With the focus in the past on exports and more recently on infrastructure investment and housing, supporting consumption should now be the priority. As higher wages draw migrants from the countryside into cities, a growing middle class can generate a domestic source of demand that was not previously possible. Although it is still small, the middle class has been hit hard by falling house prices and the declining equity market.

There are several proposals for supporting domestic consumption in the near term. The first is to focus on social infrastructure investment for the growing urban populations. While physical infrastructure investment has been excessive, Chinese cities need a more sophisticated urban and social infrastructure. In comparison to similar cities outside China, including Hong Kong and Singapore, they often offer little in terms of culture, parks and other amenities.

Second, policy should have a strong element of social welfare. Providing migrant workers with better benefits was often mentioned as a sensible policy step. Several people we spoke with mentioned the idea of the government buying back unsold or pre-sold housing units from developers and turning them into social housing.

For either of these policies to be successful, a change in policy style, moving away from centralisation to the delegation of powers, is likely to be needed.

Finally, many Chinese economists argue in favour of helicopter money (direct fiscal transfers) to stimulate consumption and boost the economy. However, policymakers are concerned by the incentive effects of giving away money.

Longer-term, China faces demographic problems arising from a declining and aging population. Attempts to increase fertility following the one-child policy have so far not been successful. Moreover, while the Chinese population is getting healthier, the retirement age is very low, raising the dependency rate. The impact of this will be a decline in potential output over time. Policies to delay retirement may therefore be helpful.

The anti-corruption drive

Endemic corruption is a key problem in China and combatting it is naturally an important policy objective. Recently, the anti-corruption drive has increasingly focused on the financial sector. The party is worried about a large financial sector that could challenge its dominant role. That is one factor underpinning the shift away from markets to state control.

Some companies offering certain underperforming investment products – such as wealth management products - are concerned that they will attract the authorities’ unwanted attention. In the past, banks were encouraged to lend and engage in housing finance. However, they are now sometimes seen as not having supported the real economy. Many financial institutions now see lending to local governments and small and medium sized enterprises as politically much safer than lending to corporates and households. Overall, the risk of prosecution has weakened the financial sector.

Conclusion

The policies of the Communist Party are key to China’s economic prospects. Prior rapid economic growth placed greater economic power in the hands of those outside the party and generated inequality, something the Communist Party fears could impact social cohesion. This has encouraged a move away from free market policies towards a more centralised approach to governance.

This was perhaps less controversial in a strong growth environment. However, a slowing economy may generate social unrest, challenging the anti-free market stance and causing a dilemma for the Communist Party. While the Party has been flexible and changed policy rapidly in the past, stimulating the economy while maintaining more centralised control will prove a challenge in the near term.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.