- Date:

- Author:

- GianLuigi Mandruzzato

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

Falling energy prices have recently provided relief to consumers after large increases over the past two years. In this edition of Infocus, Senior Economist GianLuigi Mandruzzato looks at the fundamentals of oil and natural gas markets and considers the near-term outlook.

Oil and natural gas prices have fallen sharply since mid-2022 amid evidence of resilient supply exceeding demand as the global economy slowed. In particular, the weakness of the energy-intensive manufacturing sector reduced the demand for electricity and for the energy raw materials used to produce it. Furthermore, the growth of electricity production from renewable sources further reduced the demand for fossil fuels and added to the downward pressures on their prices.

The oil market

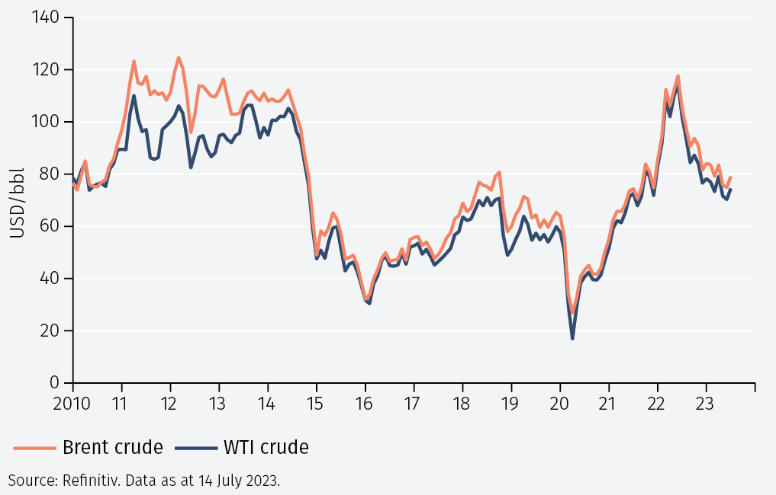

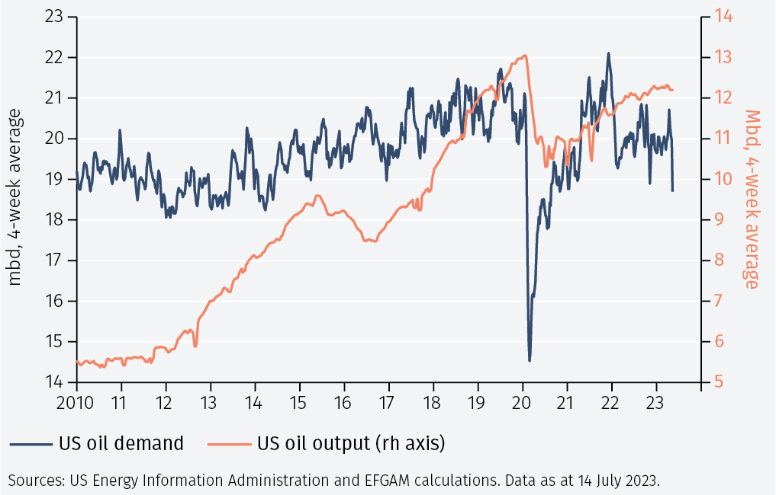

The oil price has returned to levels last seen prior to Russia’s invasion of Ukraine in February 2022 (see Figure 1). This reflects the decline in demand due to the high prices of petroleum products reached in 2022, the weakness of the global manufacturing sector, and changes in consumer habits after the pandemic. This trend is evident in data for the US, the world’s largest consumer of energy products (see Figure 2).

However, prices remain sufficiently high to incentivise production in non-OPEC+ countries, including the US, which in 2023 will see its highest annual production ever, exceeding 12.3 million barrels per day (mbd). Therefore, since the beginning of 2022, the oil market has seen an excess of supply over demand of around 0.5 mbd, which has weighed on prices.

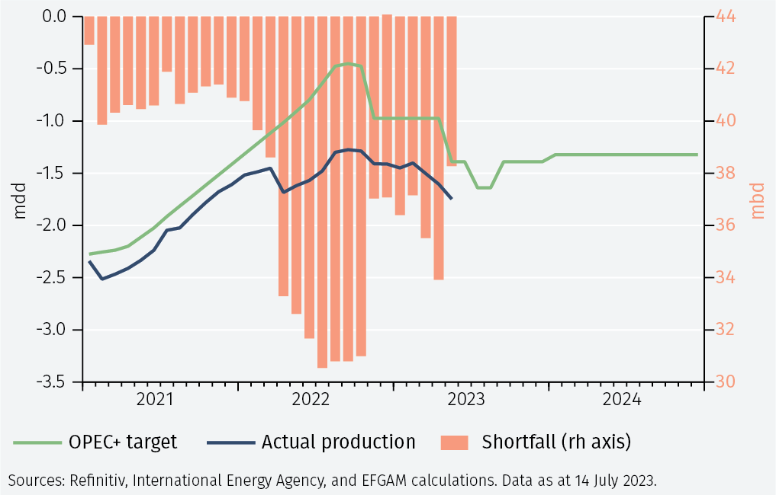

This excess supply has persisted despite the efforts of the OPEC+ cartel, led by Saudi Arabia and Russia, to rebalance the market by reducing production (see Figure 3). The latest cuts, announced in April, June and July of 2023, reduced production quotas by a total 2.66 mdb, or almost 3% of global supply.

The failure of OPEC+ to push oil prices higher further undermines its credibility as a market stabiliser. That role is already diminished after the cartel has undershot its production targets and yet global oil supply has continued to exceed demand (see Figure 3). Furthermore, frequent revisions to the cartel’s production targets highlight the difficulty in determining how much oil is needed to balance the market in the post-pandemic economy.

At the same time, the cartel’s strategy of cutting production to increase prices risks being self-defeating. High oil prices support production outside the cartel and accelerate the transition to renewable sources of energy, creating the conditions for a longer-lasting excess supply of oil. In this context, only a significant recovery of the global economy could rebalance the market in the next few months and support significantly higher oil prices, although this seems unlikely.

The natural gas market

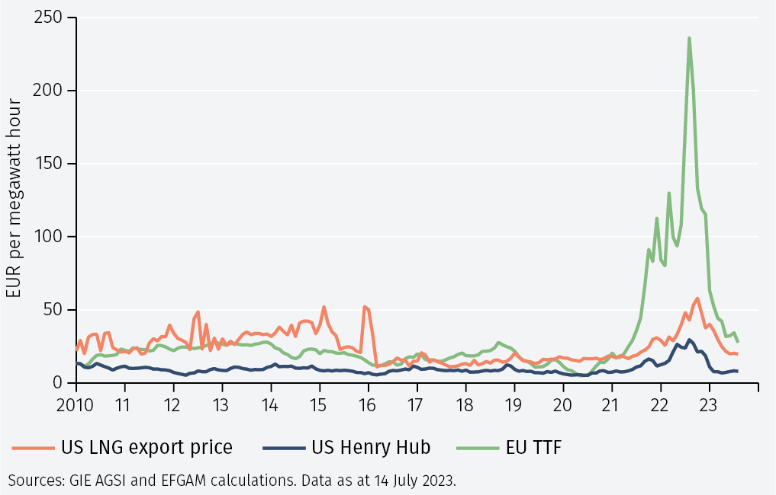

The collapse in the price of natural gas was as spectacular as its surge from mid-2021 to August 2022 (see Figure 4). In Europe, after exceeding EUR300 per megawatt hour (MWh) last year, the price has dropped close to EUR25 MWh, a manageable level albeit at the high end of the pre-pandemic range. In the US, the price on the domestic market and that of exported liquified natural gas (LNG) both fell to the low end of their pre-pandemic ranges.

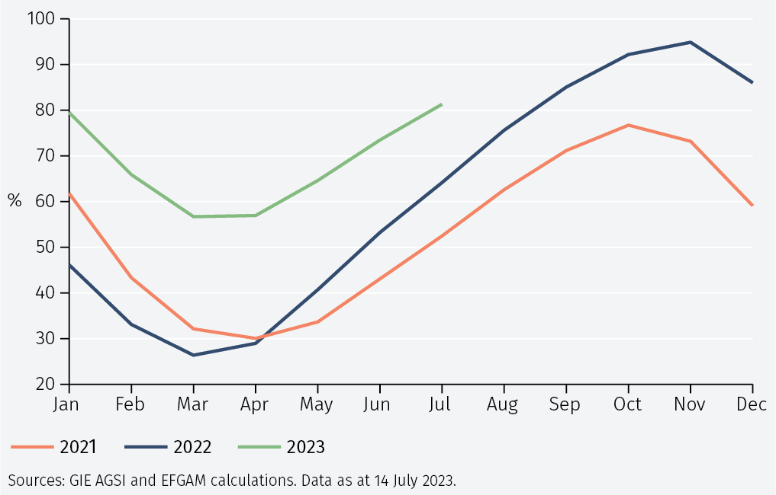

The drop in European natural gas prices reflects a 24% reduction in local consumption in the first half of 2023 compared to 2021 and the diversification of suppliers to replace imports from Russia after the invasion of Ukraine. As a result, in early July EU natural gas storage was at 80% of capacity, much more than in the same period over the last two years (see Figure 5). High storage capacity implies that a daily pace of accumulation of less than half that of the April-June period will be enough to achieve the target of 95% of capacity at the end of October. The resulting moderation of natural gas demand from Europe will help keep prices low globally.

Gas prices received further downward pressure from record US production. According to US Energy Information Administration estimates, US excess supply over domestic demand will be 50% greater in 2024 than in 2022, increasing the availability of US LNG for exports and keeping the global natural gas market well supplied.

Conclusions

Energy prices, including those of oil and natural gas, have fallen sharply since mid-2022 due to weak demand and despite measures taken by OPEC+ to support oil prices. With the energy-intensive manufacturing sector being particularly weak, energy price risks remain skewed to the downside over coming months.

In turn, lower energy prices will help lower inflation. Over time, this should filter through to the core components of consumer price indices, creating the conditions for less restrictive monetary policy.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.