- Date:

- Author:

- GianLuigi Mandruzzato

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

The latest data on growth and inflation in the eurozone were lower than expected and there is a clear risk that the economy is entering a recession. In this Macro Flash Note, Senior Economist GianLuigi Mandruzzato looks at the implications for the European Central Bank’s monetary policy and eurozone bond yields.

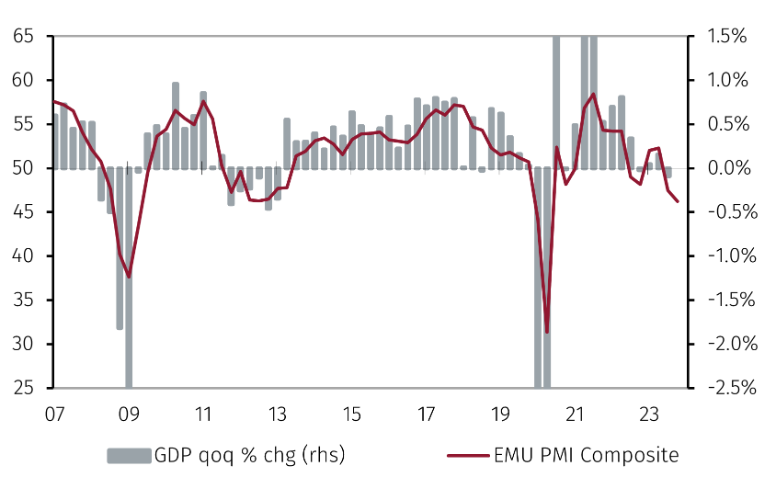

Eurozone GDP fell 0.1% quarter-on-quarter (QoQ) in 2023 Q3, below market expectations of 0.2% growth (see Chart 1). More importantly, the latest GDP data is lower than projected by the ECB in September. Furthermore, the decline in the composite PMI index in October suggests that the risk of a technical recession, defined as two consecutive quarters of negative growth, is high.

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 07 November 2023.

If this scenario materialises, average GDP growth in 2023 would reach at most 0.4%, much less than the 0.7% expected by the ECB in September. Furthermore, the negative carryover into next year makes the central bank's estimate of a growth rebound to 1% optimistic.

The weakness of economic activity during the summer is not surprising and reflects, together with other factors, the tightening of monetary policy that began twelve months earlier. The slowdown in the economy is necessary to rebalance supply and demand and encourage inflation to return towards the 2% target.

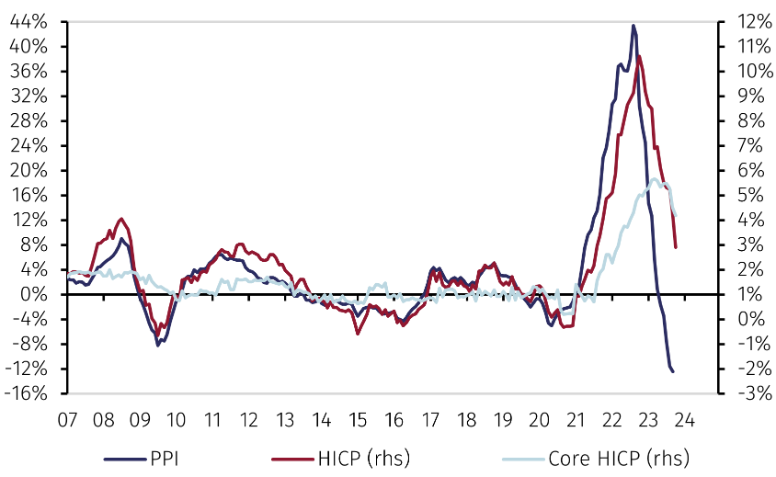

A case in point is the decline in headline inflation to 2.9% year-on-year (YoY) in October, although core inflation remains high at 4.2% YoY (see Chart 2). The ECB's seasonally adjusted data show a sharp slowdown in the most recent monthly changes in both non-core prices - food and energy - and core prices, which are the main focus of the central bank.

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 07 November 2023.

In the last three months, the monthly growth in core prices points to a return of inflation to close to 2% in mid-2024, almost a year earlier than projected by the ECB in September. This scenario is also supported by the double-digit decline in the producer price index (PPI) for manufactured goods and the stagnation of the PPI for services.

The monetary tightening initiated by the ECB in July 2022 is therefore likely to have peaked. If indeed the eurozone slips into recession and inflation continues to fall, it would be normal for the ECB to reduce interest rates as early as next year. Ultimately, self-flagellation is not a monetary policy strategy.

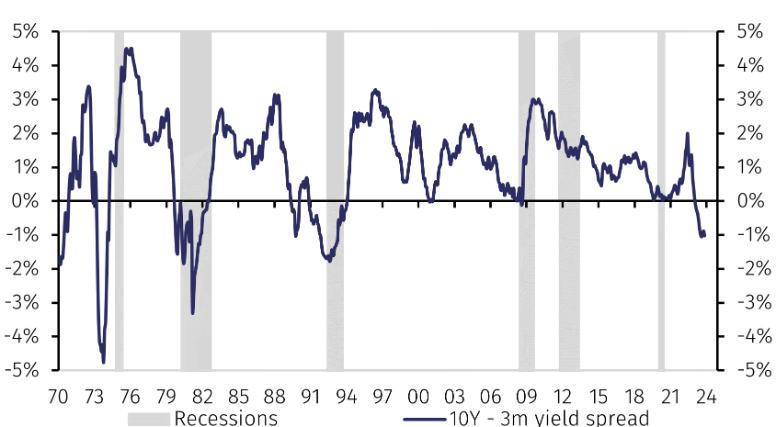

If history repeats itself, we would expect short-term interest rates and long-term government bond yields to fall in the coming quarters (see Chart 3).1 In four of the six eurozone recessions that have occurred since 1970, both short-term interest rates and long bond yields have fallen, with the former decreasing by more than the latter. One exception was the recession in the late 1970s that followed the second oil price shock, when central banks prioritised fighting inflation over supporting growth. The other exception was during the pandemic when interest rates and bond yields were both already negative prior to the recession.

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 07 November 2023.

As a result, the slope of the curve, measured as the difference between the 10-year government bond yield and the 3-month interest rate, would steepen and turn positive (see Chart 4).

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 07 November 2023.

In conclusion, with the eurozone economy likely heading towards a recession and inflation falling, the ECB has no need to raise rates further and will start discussing rate cuts by mid-2024. As a result, it seems likely that bond yields will fall and the yield curve will progressively steepen in the coming quarters.

1 Short-term interest rates and German government bonds are considered here as benchmarks for the eurozone.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.