- Date:

- Author:

- GianLuigi Mandruzzato

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

The exceptional monetary policy tightening of the past year has restricted access to, and the demand for, bank financing. In this edition of Infocus, GianLuigi Mandruzzato looks at the outlook for bank lending in the US and the eurozone considering the recent banking sector turmoil and concludes that the risk of recession has increased.

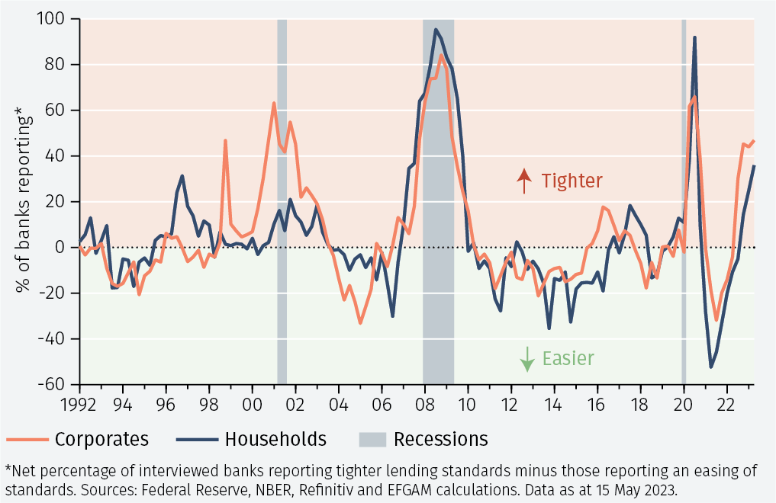

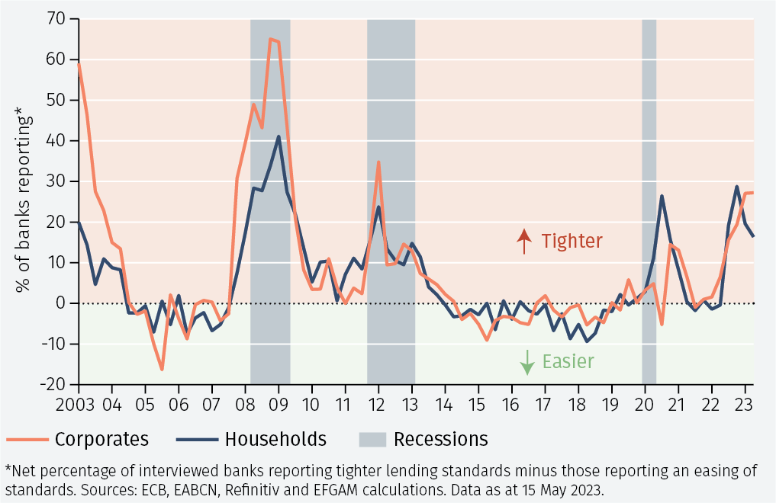

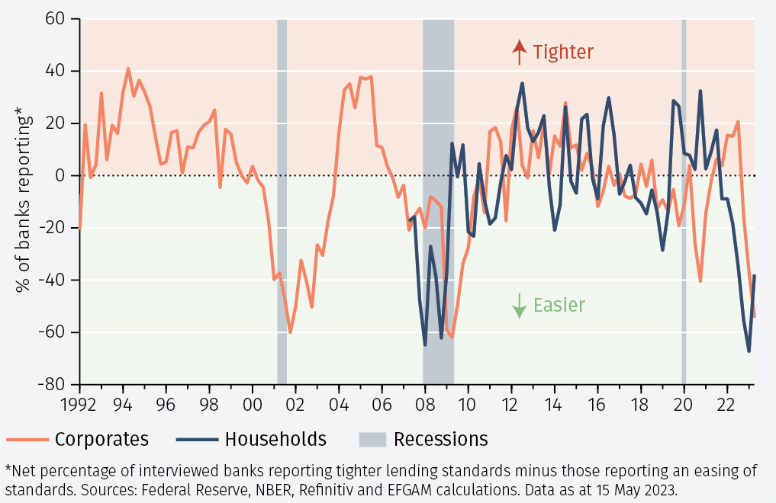

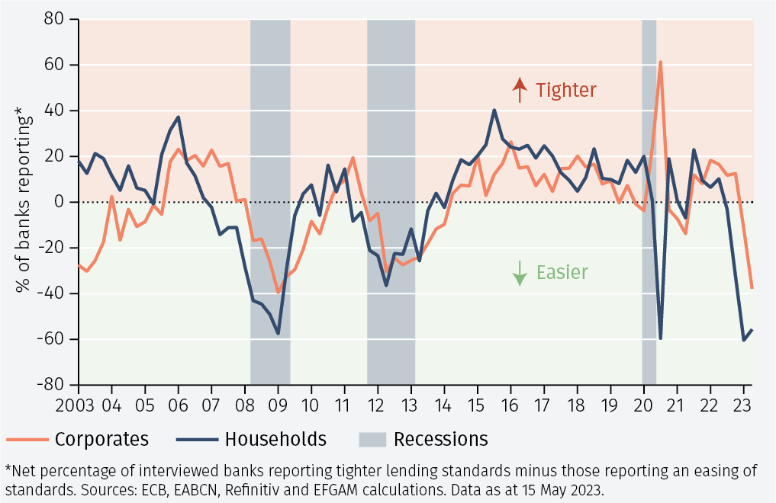

The growth in bank loans is a reliable barometer of the economic cycle. The results of the latest bank lending surveys in the US and the eurozone are therefore worrisome. Between late March and early April, banks surveyed in the Federal Reserve’s Senior Loan Officer Opinion Survey (SLOOS) and the ECB’s Bank Lending Survey (BLS) reported a further, significant tightening in lending standards to businesses and households compared to three months earlier.

The survey results show that the banking sector turmoil that broke out in early March has made banks more cautious. Despite a downward shift in the expected path of interest rates in the coming quarters, financing conditions have become more restrictive. This increases the likelihood of a slowdown in credit flows and the risk of recession in the second half of 2023 (see Figures 1 & 2).

The recent tightening of bank lending standards is similar to that seen prior to recessions in the US and eurozone over the past 30 years.

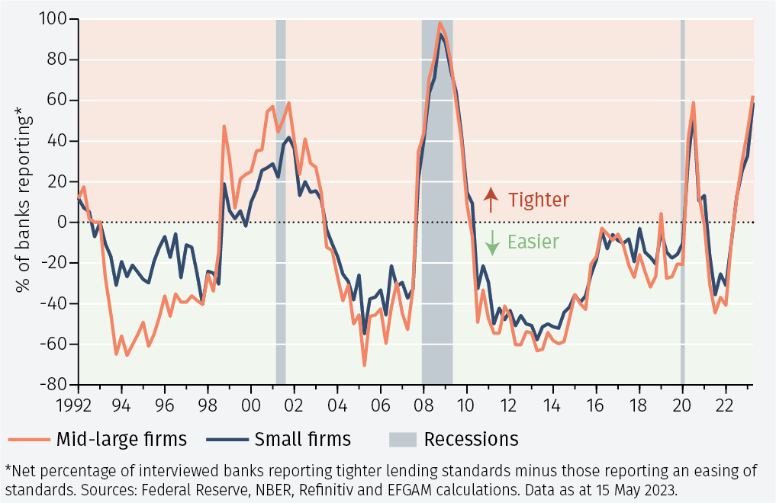

The surveys show that a growing share of commercial banks in the US and eurozone have raised interest rate spreads on loans relative to their cost of funding (see Figure 3). Furthermore, the latter has increased both because of central bank rate hikes and also as a consequence of the recent increase in banking sector uncertainty. The result is that for non-financial firms and households the cost of credit has increased more than indicated purely by central banks’ policy tightening. This matters when assessing the need for further monetary policy tightening.

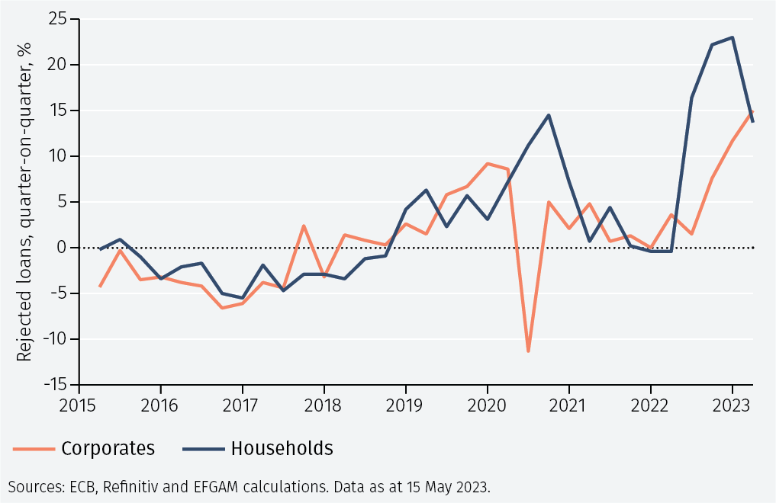

The granularity of bank lending surveys shows that US banks have reduced the size and duration of loans granted relative to requests from firms and households. In contrast, in the eurozone, commercial banks increased the share of rejected credit applications. In the case of corporate loans, this occurred at the fastest pace since this question was added to the survey in 2015 (see Figure 4).

Finally, the surveys show a sharp decline in credit demand in the US and the eurozone (see Figures 5 & 6). It is evident that declines in demand for bank loans are correlated with recessions and that the collapse in demand reported by commercial banks is equal to or greater than that recorded during the recessions of the last 30 years.

According to the ECB survey, in early 2023 loan demand from firms and households fell mainly due to increased interest rates. President Lagarde said this showed that the measures taken by the ECB since July 2022 made eurozone monetary policy restrictive even before interest rates were increased again on 4 May.

In conclusion, the evidence from the last 30 years shows that tight lending standards have preceded recessions in the US and eurozone. The tightening reported in the latest bank lending surveys therefore increases the risk of recession in the second half of 2023.

Even if a recession is avoided, moderate growth will tame inflation. The implications for monetary policy are that there is less need for further interest rate increases on both sides of the Atlantic.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.