- Date:

- Author:

- Joaquin Thul

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

Equity markets had a strong start to the year despite economic data that signals a deceleration in activity across the world, ongoing geopolitical tensions and concerns over persistent inflationary pressures. In this edition of Infocus, Joaquin Thul looks at the drivers of earnings growth and explains the differences in expectations for 2023 among regions.

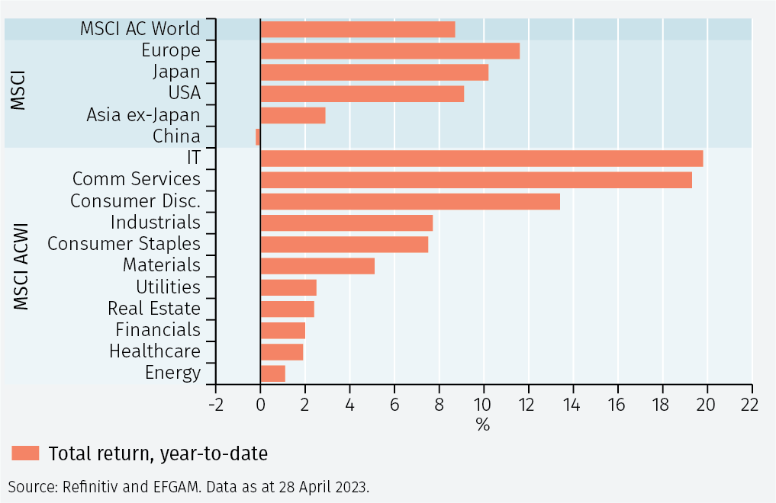

Global equities, measured by the MSCI All Countries World index (MSCI ACWI) are up by over 8% year-to-date (YTD) in local currency terms. The strong start of the year was driven by positive performance from developed economies, led by the European market, which is up over 11% YTD, followed by the US and Japan. Emerging economies, although still in positive territory, have so far lagged developed markets.

The end of Q1 2023 was marked by turmoil in the financial sector, with the failure of two US banks and the acquisition of Credit Suisse by UBS. Despite this, Financials globally are up by almost 2% YTD, being among the worst performing sectors in the year, together with Energy and defensive sectors such as Healthcare and Real Estate (see Figure 1).

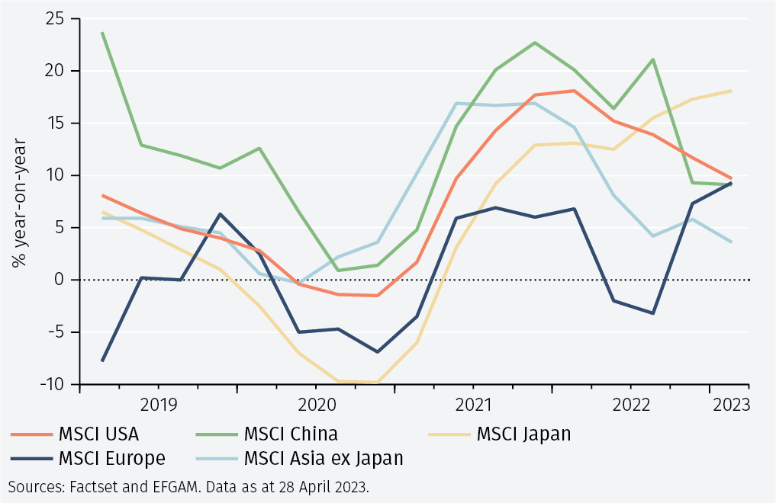

In this context, company earnings in the MSCI ACWI have declined by 6.6% year-on-year (YoY) so far in the reporting season for Q1 2023. However, this decline has not been attributed to a fall in revenues, which have grown by over 8% in comparison to last year, but rather to a reduction in margins across regions (see Figures 2 & 3).

Revenue growth remains positive in all regions, although there are some clear signals of deceleration in sales growth in US and China. In Europe, revenue growth deteriorated in the second half of 2022, but is now showing a strong improvement, with growth of over 9% YoY (see Figure 2). This has been due to the positive spill-over effect from the reopening of the Chinese economy.

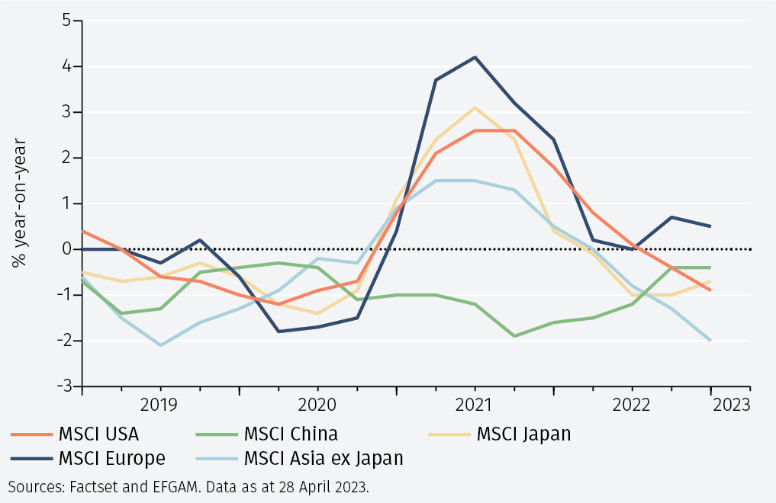

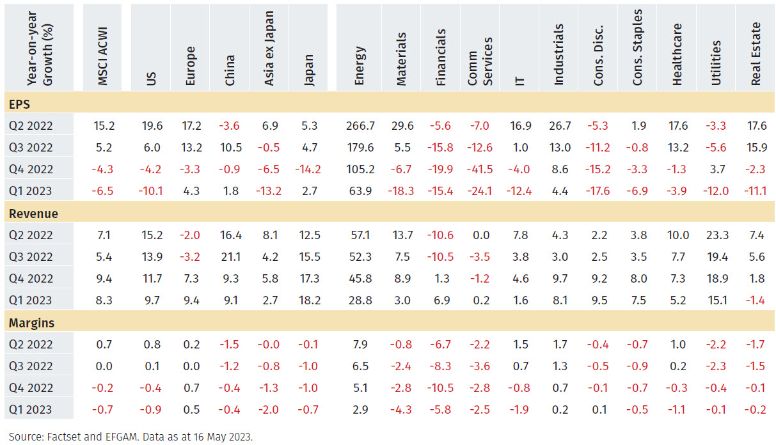

Therefore, the decline in reported earnings is largely explained by a deterioration in margins. Since Q2 2022, margins growth has been declining as companies across the world faced increased cost pressures. Russia’s invasion of Ukraine triggered a surge in energy and food prices, adding to inflationary pressures which were already affected by the aftermath of the Covid pandemic, increasing wage costs for firms and ultimately driving central banks to raise interest rates. As a result, margins declined in the second half of 2022 and are down by 0.7% YoY for the MSCI ACWI in Q1 2023. The context differs across regions and sectors (see Figure 4). Margins in China have been declining for over a year. However, similarly to margins in Europe, they have shown signs of improvement in the first quarter of 2023 (see Figure 3). In the rest of Asia and in Japan margins have declined for four consecutive quarters, and in the US margins growth has declined by almost 1% YoY.

Companies in the Energy sector benefited in 2022 from the increase in oil and gas prices. This helped revenues and margins, which have now started to decelerate as the year-on- year comparison reflects the moderation in energy prices globally. The slowdown in economic activity in the second half of 2022 and the start of 2023 has not only impacted earnings in cyclical sectors such as Communication Services, Technology, Consumer Discretionary and Financials, but also defensive ones such as Consumer Staples, Utilities, and Healthcare. For the latter, their defensive nature meant the decline in earnings has been attributed to a deterioration in margins rather than a decline in revenues.

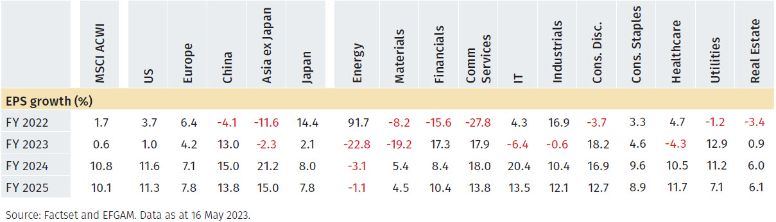

Projections for earnings in 2023 fiscal year (FY) show doubledigit earnings growth in China, with strong expectations also for the coming years. US earnings are expected to decline, but remain positive, reflecting a less negative outlook for the corporate sector. Earnings in Europe and Japan are also expected to be positive for this year (see Figure 5).

EFGAM forecasts for quarterly earnings growth

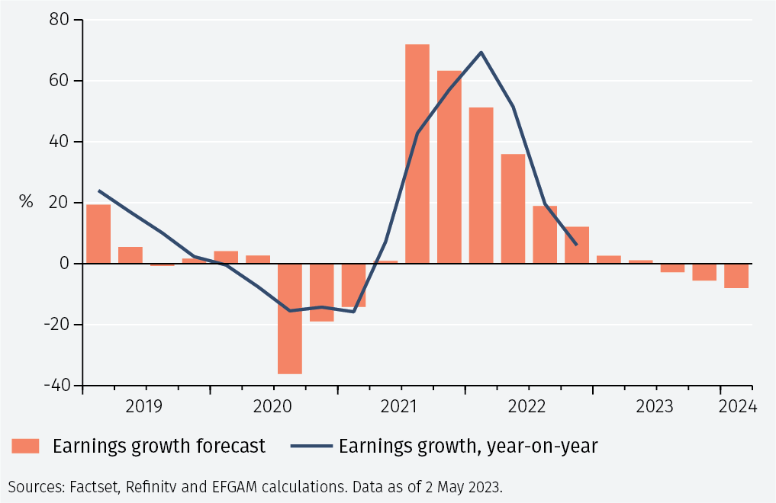

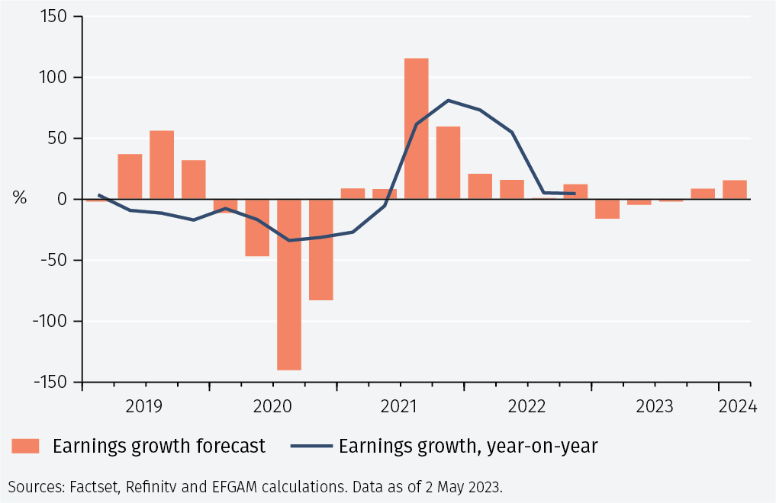

According to our models’ forecasts, earnings growth is expected to differ across countries and regions.1 In the US and UK, earnings growth is expected to decline at least until Q1 2024 (see Figures 6 & 7). In the US, earnings growth is expected to turn negative in the second half of the year, under pressure from the contraction in margins. The MSCI UK index, generates almost 80% of its revenue from outside the UK, and is therefore more exposed to the global economic cycle. Although UK earnings growth is expected to decelerate from the high levels seen in 2022, it is expected to remain positive in the coming quarters. So far in the earnings season, the better-than-expected performance has been driven by positive surprises in Financials and Healthcare.

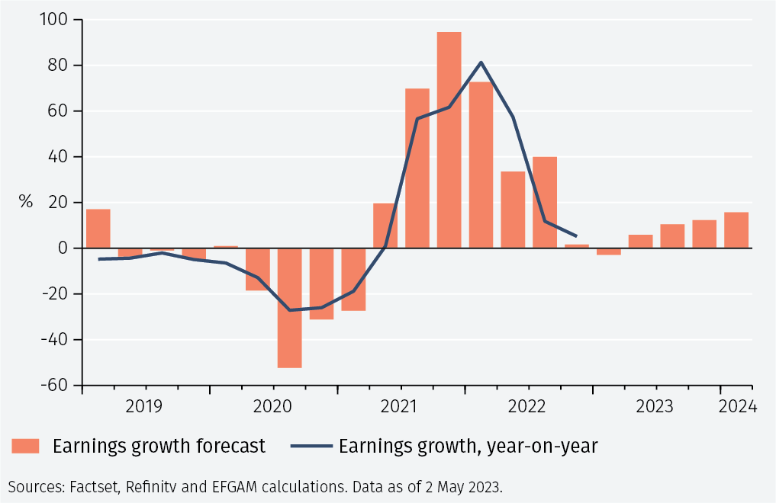

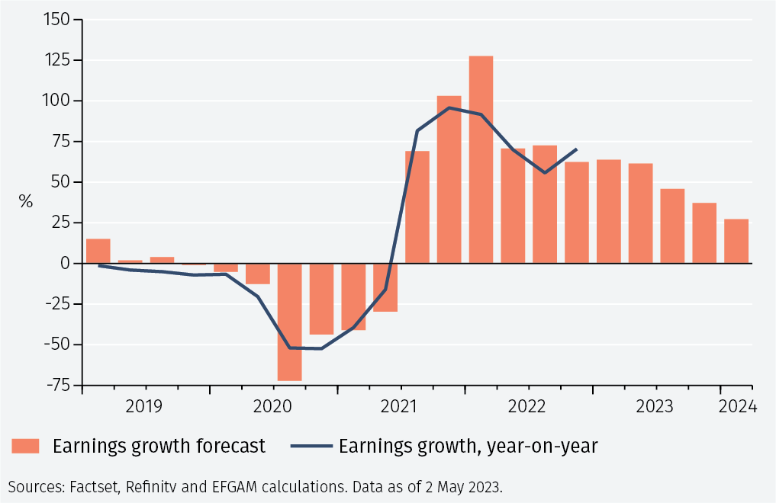

Conversely, in Europe ex-UK and Japan, earnings growth is expected to decline in the first two quarters of 2023 before picking up again in the second half of the year (see Figures 8 & 9). Expectations for a short-lived pain in Europe ex-UK reflects both strong revenues and improving margins in recent months, possibly associated with the deceleration of cost pressures and a positive impact from China’s reopening economy. In Japan, weaker earnings guidance from companies has set expectations low for 2023. The Japanese yen has weakened against the US dollar by over 3% YTD, contributing to the positive stock market performance. Although weak margins are expected to weigh on earnings in the coming months, the latest BoJ survey of the Japanese corporate sector showed expectations for improved economic conditions in non-manufacturing sectors.2

Conclusion

Earnings reports have started to reflect a deceleration in economic conditions across the board. This has been mostly attributed to a contraction in margins, rather than a decline in revenues. Looking at fiscal year (FY) projections for earnings in 2023, China is expected to reflect double-digit earnings growth close to 13% following the reopening of the economy since November 2022. Europe and Japan are the other two regions where analysts currently expect positive earnings growth for this year, supported by our models’ forecasts. However, earnings projections in the US are expected to be weak in FY 2023, before a recovery in FY 2024 and FY 2025. Nevertheless, consensus estimates for US earnings reflect expectations of a mild recession. As such, it remains important to be selective in the regional exposure to equities.

1 Using quarterly data since Q4 2003, EFGAM’s models include GDP YoY growth, headline annual inflation, share buybacks YoY and interest rates as independent variables to forecast quarterly earnings growth YoY.

2 BoJ Tankan March 2023 Survey https://www.boj.or.jp/en/statistics/tk/gaiyo/2021/tka2303.pdf

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.