- Date:

- Author:

- Joaquin Thul

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

After only 45 days in office, Liz Truss resigned as UK Prime Minister (PM) making her the shortest-serving leader in UK history. Days later, Rishi Sunak was appointed as UK PM and Conservative Party leader. In this edition of Infocus, Joaquin Thul analyses what we can expect from Sunak’s term.

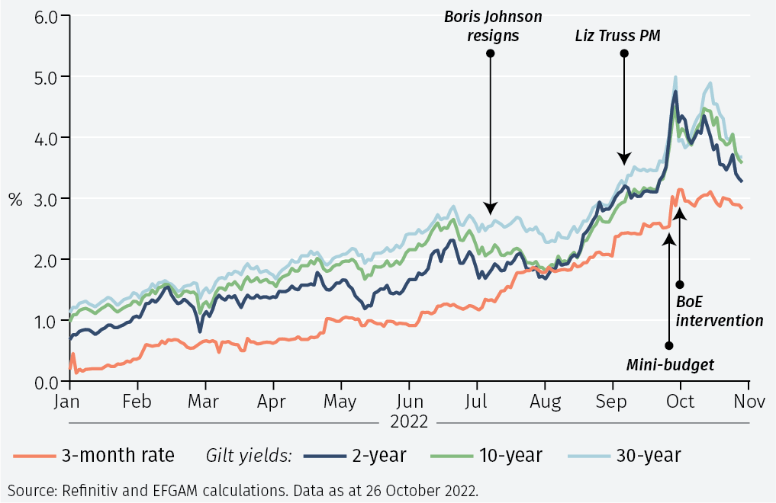

Following several U-turns on economic policies, a series of changes in key cabinet positions and the lost support from some Conservative Members of Parliament (MPs), Liz Truss resigned as PM only 45 days after taking office. Former Chancellor Kwasi Kwarteng had announced a series of economic measures and tax cuts which were received negatively by markets. The yield on 30-year gilts increased by 120 basis points in three days and the pound hit a historical low of USD 1.03, adding to a depreciation of over 20% year-to-date. The selloff in long dated UK government bonds affected domestic pension funds, requiring the intervention of the BoE to purchase long-dated gilts to ensure proper market functioning, see Figure 1.1

The level of discontent with the economic strategy drove Truss to sack Kwarteng and appoint Jeremy Hunt as new Chancellor. Hunt, an experienced official who held cabinet positions for nine years under David Cameron and Theresa May, is perceived as a pragmatic politician within the Tory Party. He reversed the majority of Truss’ mini-budget policies and anticipated a series of tax hikes and spending cuts aimed at stabilizing public accounts. Truss resigned days later.

On 24 October, Rishi Sunak was appointed as UK PM after being the only candidate that gathered the required support from Tory MPs.2 Having previously served as Chancellor under Boris Johnson, Sunak was perceived by markets as the appropriate person to restore trust after the tumultuous summer months.

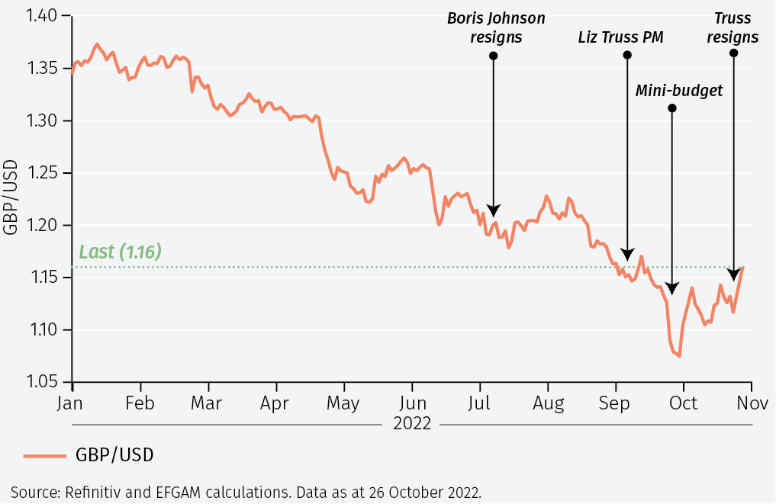

In the following days sterling bounced back to USD 1.16, returning to levels observed before Truss was appointed PM, see Figure 2. On a year-to-date basis, the pound has fallen by 14% against the dollar.

What policies can we expect from Sunak?

After former PM Johnson’s resignation in early July, Sunak campaigned to become the Tory Party leader and PM based on a ten-point plan.3

The main economic aspects of that plan were: beating inflation; and encouraging investment and training to boost productivity and GDP growth.

In the near-term, with energy prices high and supply bottlenecks only slowly easing, there will be no growth boost. Indeed, the latest IMF projections see UK GDP growing only 0.3% in 2023, after 3.6% in 2022.

His ten-point plan involved cutting the basic income tax rate by one fifth and removing VAT on energy for households.

Such tax reform proposals are unlikely to be fully implemented in the near term.

Jeremy Hunt, the new Chancellor (finance minister) has delayed the autumn fiscal statement to 17 November, when the forecasts from the Office for Budget Responsibility will also be released. He is expected to announce tax hikes and spending cuts to meet fiscal needs of approximately £40- 50bn, equivalent to around 2% of GDP, depending on how the economy performs next year. Other measures, such as increasing the windfall tax rate on oil and gas producers or extending this levy beyond the December 2025 deadline, could also be proposed.

On foreign policy, Sunak committed to deliver on the Brexit plan set out by former PM Johnson, changing the EU laws that, in his view, constrain the UK economy. He also pledged to modify the Northern Ireland protocol and find a compromise with the EU on custom borders.4 Although Sunak does not want this dispute to escalate, he will be pressured by Eurosceptic Tory MPs to take a hard line with Brussels in these negotiations.

Additionally, Sunak supported tightening the rules on asylum seekers, capping the number of refugees allowed into the UK and backed the controversial Rwanda Partnership announced in April.5 Suella Braverman, reappointed as Foreign Secretary, supports Sunak’s policy on asylum rules, but legal constraints still restrict the implementation of this plan.6

Sunak will also need to deal with a difficult geopolitical scenario, dominated by relations with Russia, the crisis in Ukraine and the potential need to increase government spending on defence if tensions continue to escalate.

Finally, on domestic issues, Sunak has committed to reduce backlogs on the NHS and introduce fines for missed appointments, implement tighter controls on crime, and new policies on education. He also proposed to strengthen the Union within the UK nations by increasing investment in Scotland, Wales and Northern Ireland.

Sunak’s relative inexperience may become an issue given the busy agenda he now faces as PM and party leader.7 Beyond governing the country, he also has the difficult task of increasing the popularity of the Conservative Party. In the last year, the polls show that the support for Tories dropped to 22% from 35% of voters while the Labour Party support rose to over 50% of voting intentions.8

Sunak stated the nominations for his new cabinet show “unity, experience and continuity”, with the intention of keeping all factions of the party involved in the policy decisions. If he maintains the support from Conservative MPs, he will benefit from the large majority that Tories currently have in the House of Commons, with enough time for the Party to recover before the next General Election, to be held no later than January 2025.

Conclusions

Recent political events are rare in the UK. The speed with which Truss lost the support from both the public and the Conservative Party highlighted her mistakes and those made by her economics team. In comparison, Sunak seems a more pragmatic, if less experienced, politician compared to some of his recent predecessors. The reappointment of Jeremy Hunt as Chancellor points to continuity with the recent policy announcements which were well received by markets.

Nevertheless, equity markets in the UK have underperformed in the last month due to the domestic political noise. The FTSE 100 index was up by 2% in October, underperforming the MSCI World index which was up by 7.5%. However, in a year of volatile markets, UK equities are down by only 5% on a year-to-date basis, helped by the value characteristics of the UK market. The pound has recovered its lost ground against the US dollar since September and we maintain a positive outlook for the currency in the near term as the BoE continues to tighten monetary policy and expectations of a peak in US interest rates in Q1-23 will weaken the dollar. However, long term prospects remain challenging given some of the previously stated problems facing the UK economy.

It is uncertain how Sunak will fare as PM but considering the difficulties faced by the last three British PMs and the circumstances in which they resigned, the bar for him is very low. The UK economy will weaken in the coming months, and the necessary fiscal restraint will be compounded by Bank of England monetary policy tightening. However, more pragmatic policies and political stability will be welcome after a tumultuous year.

1 This was explained by Sam Jochim in a previous Macro Flash Note: https://www.efginternational.com/uk/insights/2022/uk-mini-budget-sparks-gilt-market-mayhem.html

2 Rules of the Conservative Party established that candidates required the support of at least 100 Tory MPs to be nominated for the Party’s leadership.

3 See https://www.ready4rishi.com/ten_point_plan_for_great_britain

4 The Northern Ireland Protocol, signed by Boris Johnson in January 2020 as part of the UK’s Withdrawal Agreement with the EU, keeps Northern Ireland in the EU’s single market for goods and prevents a hard border with the Republic of Ireland. However, it requires the implementation of checks and controls on goods which come into Northern Ireland from Great Britain, creating a border in the Irish sea

5 On 14 April 2022, the UK government announced a partnership with the government of Rwanda to send illegal immigrants seeking asylum in the UK to the Republic of Rwanda. The policy is intended to deter illegal smuggling of people into the UK.

6https://www.theguardian.com/politics/2022/oct/26/suella-braverman-five-controversial-statements-home-secretary

7 Rishi Sunak was first elected MP in 2014, appointed as Chief Secretary to the Treasury in 2019 before becoming Chancellor in 2020.

8 Data from Politico.eu, as of 28 October 2022.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.