- Date:

- Author:

- Sam Jochim

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

Looking ahead to its policy meeting on 26 April, the Riksbank is in a difficult situation. Inflation is already much above the 2% target and is being fanned further by a depreciating krona, both of which call for higher interest rates. But a weakening economy and the fact the Swedish economy is extremely sensitive to interest rates urge caution. In this issue of Infocus, EFG Chief Economist Stefan Gerlach reviews the situation.

The world’s oldest central bank going back to 1668, the Swedish Riksbank, is facing difficulties. With double-digit inflation, a weakening economy and an unfortunate combination of massive household mortgage borrowing that is highly sensitive to rate changes, the policy meeting on 26 April will not be easy.

The key task for the Monetary Policy Committee is to find a level of interest rates that is high enough to lower inflation, but not so high as to cause difficulties for households facing large mortgage bills.

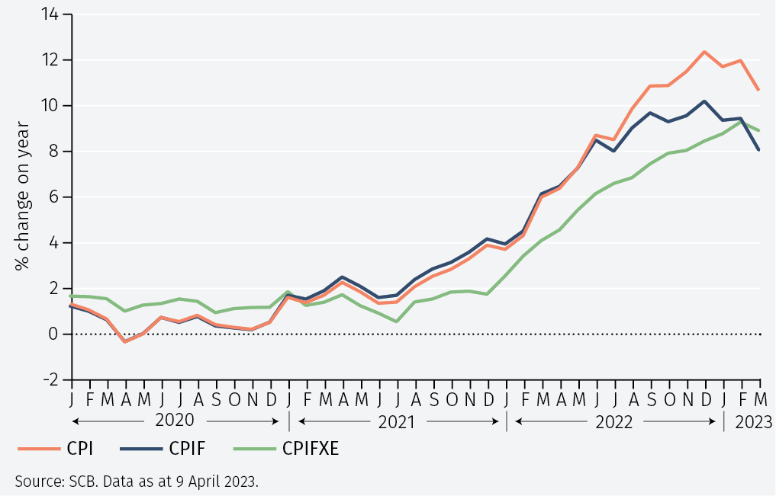

Surging inflation

Measured by the consumer price index (CPI), prices rose by 10.6% year-on-year in March. This measure of inflation will be boosted by the fact that the Riksbank has raised interest rates: looking at the CPI with a fixed interest rate (CPIF), which the Riksbank uses to express its inflation target, prices rose by 8.0% over the same period. To understand the broad-based nature of inflation it is useful to look at the CPI net of energy with a fixed interest rate (CPIFXE). By this measure, prices rose by 8.9% year-on-year in March (see Figure 1).

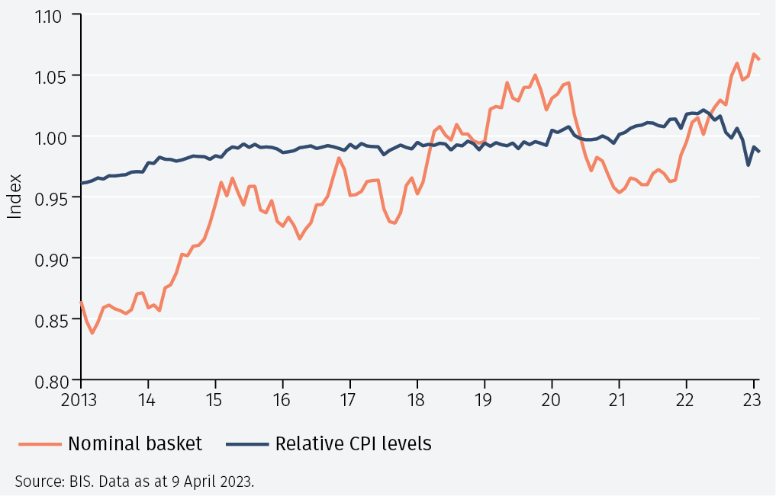

The inflation problem is reflected in the behaviour of the exchange rate. Looking at the last decade of data, Figure 2 shows that the exchange rate against a basket of currencies has depreciated very sharply since 2013 by a cumulative 23%. While the CPI in Sweden has risen marginally faster than the tradeweighted CPIs of its trading partners, the increase in relative prices, 3%, is much smaller than the change in the exchange rate, implying that the real exchange rate has also depreciated.

This unfortunate combination of an exchange rate that depreciates much beyond what is suggested by price level differentials has been more pronounced since January 2022: while the trade-weighted exchange rate has depreciated by 7%, inflation in Sweden has been 3% lower than in its trading partners.

Of course, the Riksbank targets inflation and therefore only responds to the exchange rate to the extent it has implications for inflation. But by that standard, monetary policy appears to have been too expansionary in Sweden, at least in recent years.

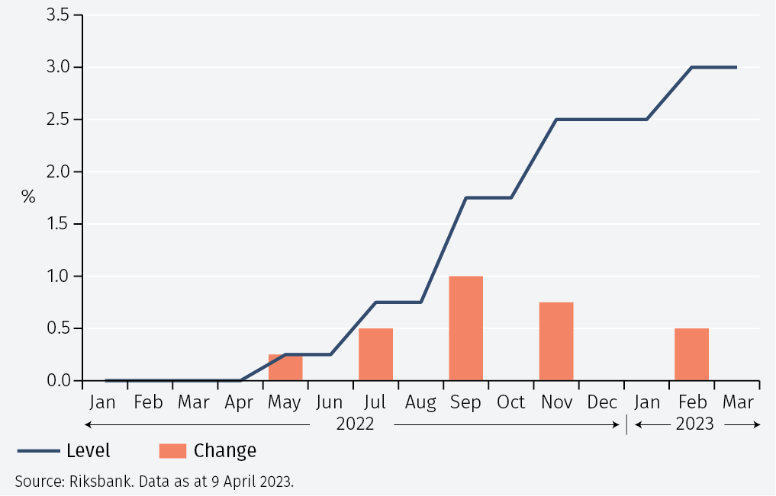

The surge in inflation and the depreciation of the exchange rate has occurred despite the Riksbank having raised interest rates by 300 basis points since May 2022. The first increase came in May 2022 when rates were increased by 25 bps (see Figure 3). Policy was tightened again in July, this time by 50 bps as the Riksbank realised its rates were far too low and had to raise them substantially. In September, it doubled up and raised rates by 100 bps. In November rates were raised again, but by 75 bps, and in February 2023, by 50 bps.

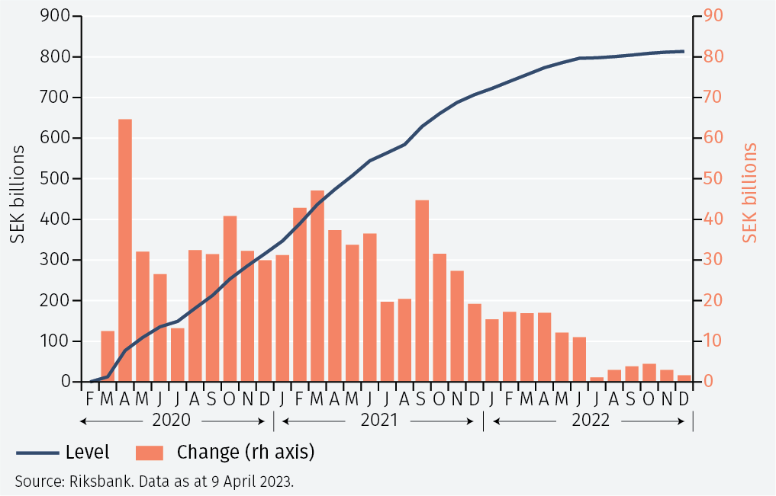

In December 2022, the Riksbank also ended its asset purchase programme, which it had started in March 2020 as the Covid pandemic started. However, purchases had been very limited from July 2022 onward (see Figure 4).

To continue reading, please download the full document.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.