- Date:

Infocus - Commodity prices and inflation in developed and emerging economies

Managing monetary policy in a small open economy is never easy. In this issue of Infocus, EFG Chief economist Stefan Gerlach looks at the Monetary Authority of Singapore’s successful “crawling peg” regime, which this year turns 40.

Much attention is paid to how central banks in large economies, in particular the Federal Reserve and the ECB, set monetary policy.1 Such economies are relatively closed and therefore not much affected by economic developments and disturbances abroad. In particular, the exchange rate is relatively unimportant. The central bank’s focus is therefore on judging the underlying state of demand for goods and services and how it impacts inflation at a horizon of about two years.

But most central banks face different circumstances. They operate in Small Open Economies (SOEs) in which the exchange rate often plays a dominant role in determining economic outcomes. A sharp, unexpected exchange rate change can plunge the economy into recession or lead to a burst in inflation. Indeed, while flexible exchange rates are often thought of as shock absorbers, the experiences of SOEs is often that they function as shock generators.

Managing the exchange rate

There are two main approaches to managing the exchange rate in a SOE. The first is to let it float freely. Since exchange rate changes impact inflation and economic activity, central banks nevertheless monitor the exchange rate and may adjust interest rates to offset any adverse macroeconomic effects it may have. Occasionally, the central bank may intervene in the foreign exchange market to prevent the exchange rate from moving excessively.

This is the approach that Switzerland followed between the breakdown in the early 1970s of the Bretton Woods system of fixed exchange rates and the global financial crisis in 2008. However, few central banks can afford to be aloof to exchange rate changes.

The polar opposite approach is to fix the exchange rate against a foreign currency. While this reduces the risk of unwarranted exchange rate movements impacting inflation and economic activity, it requires the central bank to focus solely on maintaining exchange rate parity. It must therefore disregard any domestic policy objectives. This is known as the “Impossible Trinity,” which asserts that it is impossible to have a fixed foreign exchange rate, free capital movement (without capital controls) and an independent monetary policy. Success is always uncertain, since it also requires prudent fiscal policy, which is outside the central bank’s control.

Fixed exchange rates used to be common but few central banks now operate policy this way. Notable exceptions are Hong Kong, which has operated a currency board against the US dollar effectively since 1983, and Denmark, which operates a fixed exchange rate regime against the euro.

Singapore’s “crawling peg”

Since 1981, Singapore has very successfully followed an intermediate policy strategy. Much like a fixed exchange rate regime, the strategy reduces the risk of damaging short-term fluctuations in the exchange rate. But like a floating exchange rate regime, it allows the Monetary Authority of Singapore (MAS) to gear policy to domestic considerations.

The crawling peg regime is focused on the Nominal Effective Exchange Rate (NEER) of the Singapore dollar as the intermediate target of monetary policy.2 The idea is that by steering the NEER, the MAS can achieve a desirable balance of inflation and economic activity in Singapore. While the MAS has good control of the exchange rate, it cannot precisely control it day-to-day. It therefore allows the exchange rate to move within a band around the target.

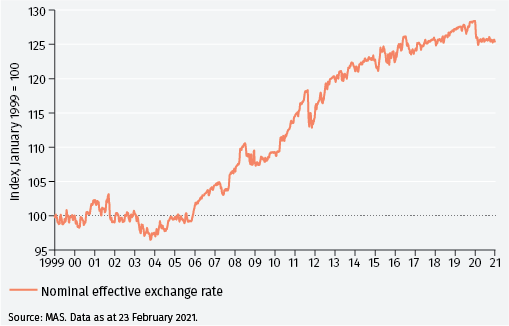

Since the objective of the MAS’s monetary policy is “to maintain price stability conducive to sustained growth of the economy,” the NEER has been allowed to appreciate gradually over time to limit inflation in Singapore (Figure 1).3 The average rate of appreciation of the NEER can be estimated by studying the time periods during which, according to the MAS’s announcements, the desired rate of change of the NEER was positive. Doing so gives an estimate of the average rate of appreciation of about 1.5% per year.4 Market commentary suggests that the width of the band is generally in the order of ± 2%.

The way in which the MAS manages the exchange rate is unique, and reflects the exceptionally high import content of spending in Singapore. Thus, exchange rate changes have immediate and powerful effects on inflation and macroeconomic conditions more broadly.

1 - Singapore’s Nominal Effective Exchange Rate (NEER)

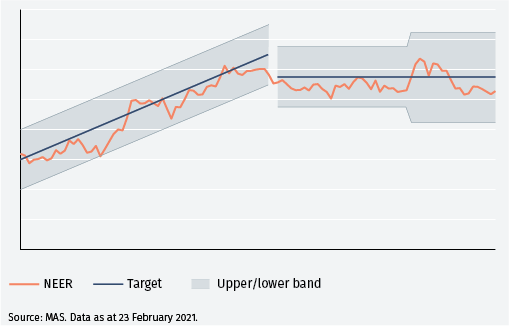

To understand the mechanics, consider the illustration in Figure 2 below.

2 - The mechanics of a crawling peg

To manage policy, the MAS has three choices to make.

- Decide how quickly the target evolves over time, that is, the “rate of crawl.” In the figure this choice is captured by the slope of the target line. As Figure 1 and the table with the announced policy decisions in the Appendix show, in practice the rate of crawl has generally been positive, but on occasion the MAS has reduced the rate of crawl to zero, that is, it has sought to maintain the exchange rate at the current level.

- Whether it would be desirable to shift the entire target band. In the figure, the target band is shifted down in the middle of the graph.

- Determine the width of the band around the target. The MAS allows the exchange rate to deviate from the target within a band, whose width need not be constant. In the figure it is assumed that the band was widened towards the end of the time period considered.

To continue reading please download the full article below.

Footnotes

1 In measuring the openness of the eurozone, it is essential to net out inter-eurozone trade. See, for instance,https://www.ecb.europa.eu/pub/pdf/other/mb199912_focus08.en.pdf

2 The nominal effective exchange rate (NEER) is a weighted average rate at which one country’s currency exchanges for a basket of multiple foreign currencies, where the weights are typically determined by the country’s trade pattern. The nominal exchange rate is the amount of domestic currency needed to purchase the basket of the foreign currencies.

3 See www.mas.gov.sg/monetary-policy/Singapores-Monetary-Policy-Framework

4 Interestingly, the MAS has never indicated that the desired rate of appreciation was negative (that is, that it desired a depreciation of the Singapore dollar).

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.