- Date:

Infocus - Is Swiss fiscal virtue too much of a good thing?

As the Swiss National Bank prepares to decide on monetary policy, GianLuigi Mandruzzato looks at the medium-term perspectives for the Swiss economy and its monetary and fiscal policy mix. One important conclusion is that exploiting the available fiscal space would benefit the economy and ease pressure on the central bank.

The Swiss National Bank (SNB) is in no hurry to tighten monetary policy as the economy recovers. Rather, persistent low inflation risks de-anchoring inflation expectations.

Swiss GDP fell by 3% in 2020, according to the State Secretariat for Economic Affairs (SECO). Although sharp, the contraction was less severe than initially feared. Furthermore, GDP is expected to rebound by about 3% in 2021 and grow strongly also in 2022. If this materialises, GDP would return to its prepandemic level at the end of this year.

However, the recovery would not be complete even in this favourable scenario, which remains subject to a high degree of uncertainty resulting from ongoing restrictions to contain the virus and the delayed vaccination campaign. The unemployment rate rose to 3.6% in February, the highest since 2010, and is expected to fall only slowly as the economy reopens. Estimates of the output gap put it at around -3% of GDP in early 2021, as activity fell in Q1 from the previous quarter (see Figure 1). Even accounting for the expected strong rebound in GDP from Q2, the output gap would remain negative at the end of the year.

Consumer price inflation has been negative since late 2019 and was -0.5% year-on-year in February. Worryingly, this reflects both a slump in core inflation and in the prices of volatile components like food and energy. Unsurprisingly, households’ inflation expectations seem to have stabilised at a level consistent with inflation hovering at the low end of the 0-2% range the SNB uses to define price stability (see Figure 2). The risk that they fall further seems to be rising, a development to which the central bank should pay more attention than it appears to be doing. The expected rebound in inflation, driven by base effects in the energy sector, should not be an excuse for SNB complacency.

The SNB will delay signalling a tightening to prevent pressure on the Swiss franc.

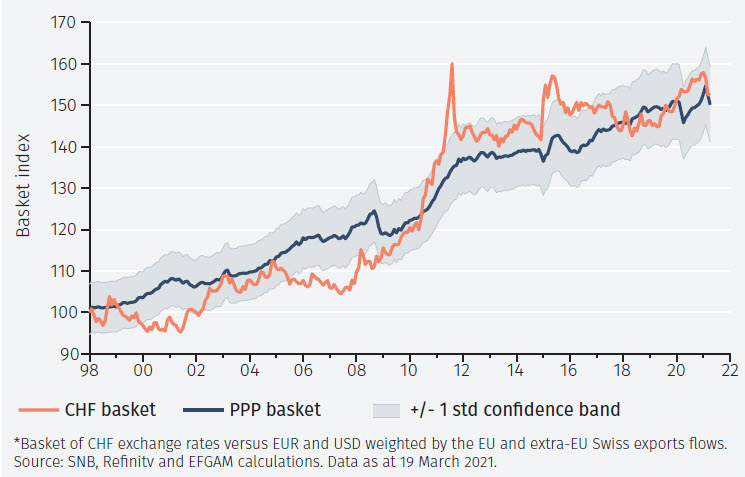

The Swiss franc has weakened recently but remains slightly overvalued on a Purchasing Power Parity basis against a basket of exchange rates including EUR and USD (see Figure 3). The SNB, which stopped intervening last summer, will welcome the decline of the franc. However, it will reiterate that the currency remains highly valued, that foreign exchange risks persist and that, therefore, it stands ready to intervene as needed.

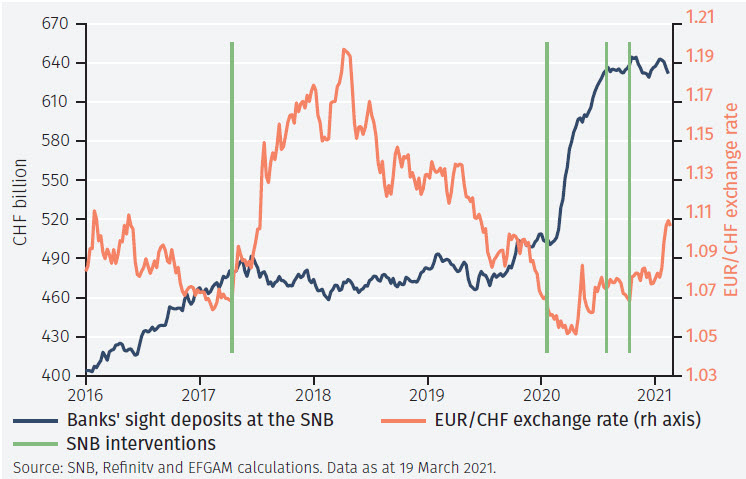

The SNB will not try to micromanage the currency but rather let market forces drive the franc lower. Nonetheless, interventions will start again should the franc strengthen by too much: 1.07 on the EUR/CHF exchange rate seems a critical threshold to the SNB, judging from sight deposit data (see Figure 4).

The SNB’s foreign currency reserves, above 900 billion francs, will not deter further interventions if deemed necessary. The SNB has emphasised that the size of its balance sheet depends on the macroeconomic outlook and interventions needed to achieve the inflation objective.

Stronger fiscal support would help the SNB’s pursuit of price stability.

Last December, the US Treasury noted that Swiss “fiscal policy should be deployed to reduce the economy’s reliance on the SNB’s policy measures, rebalance its external sector, and boost potential growth”. These observations echoed the 2019 IMF Article IV Consultation conclusions that “sustained structural fiscal surpluses amid moderate public debt and negative interest rates, have consistently overperformed the debt brake rule target, proving an unwarranted drag on growth during cyclical downswings” and warned against the risk of fiscal “underspending”.

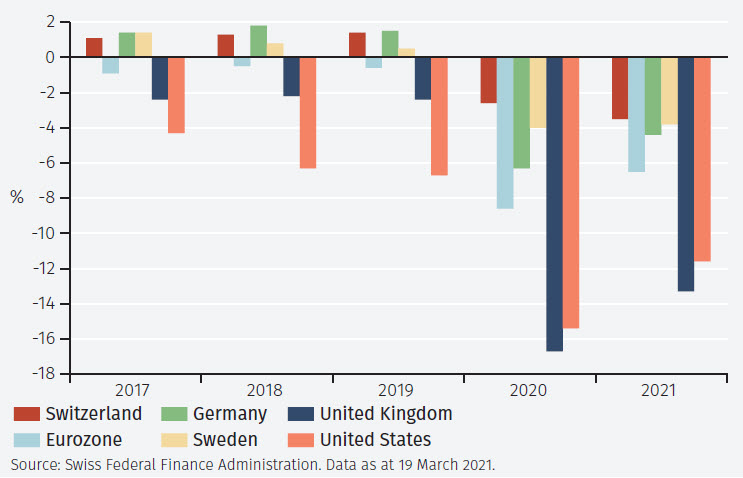

The latter risk is apparent, given the fiscal policy response to the pandemic. Despite the large resources deployed, the Swiss response is moderate compared to that of other developed countries. According to the Swiss Federal Finance Administration, in 2020 CHF16.9 bn, or 2.4% of GDP, was spent to fight the pandemic. For 2021, a further CHF22.6 bn, or 3.1% of GDP, has so far been budgeted. These extraordinary expenditures are the main reason for the historically large deficit recorded in 2020 and expected in 2021. However, Swiss budget shortfalls look small in comparison to those in Germany, the UK and the US (see Figure 5).1

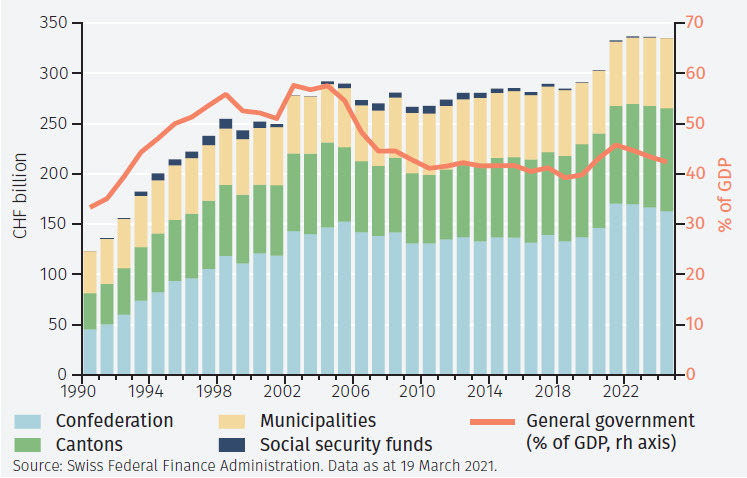

Furthermore, the Swiss authorities seem determined to return quickly to fiscal rectitude. The 2022-24 financial plan of the Federal Council envisages a balanced budget in 2022 and a small surplus in the following two years. This plan complies with the so-called debt brake in place since 2003. The rule, which aims at stabilising the debt by means of a balanced structural budget, was key in reducing the debt-to-GDP ratio to 39.8% in 2019 from 57.6% in 2002 (see Figure 6).

However, the rule gives the Federal Council six years to offset any excessive budget shortfall. This flexibility should be fully exploited as a premature fiscal tightening would risk dampening the recovery, with adverse consequences for equality, inclusion, social cohesion and the long-term potential of the Swiss economy. And too tight a fiscal policy would leave the burden of supporting the economy on monetary policy, complicating the SNB’s exit from negative interest rates and foreign exchange interventions that attract so many critics.

Footnotes

1 Comparing the deficit ratios is a rough approximation of the size of resources deployed to mitigate the pandemic; a more accurate comparison should relate the expenditure incurred to the decline in GDP.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.