- Date:

Insight - Although Covid concerns will feature in the first part of the year, we are generally optimistic about the outlook for global economic growth in 2022. With inflation rates set to fall back, the economic backdrop remains generally benign.

OVERVIEW

The focus of financial markets can shift quickly from one issue to another. With a quartet of issues dominating the outlook for the rest of the year, we expect market sentiment to be volatile and highly changeable.

The first quarter of 2023 ended with the failure of two US banks (SVB and Signature Bank) and the sudden acquisition of Credit Suisse by UBS. Most likely, these were idiosyncratic events and the relevant authorities have managed, for the time being, to avoid contagion to the rest of the financial system. However, concerns have not been fully dispelled and they are likely to linger for the remainder of 2023. Meanwhile, financial markets’ previous worries about inflation, the resilience of global growth (with the possibility of recession) and geopolitical tensions remain. Attention will undoubtedly return to these. In the post-pandemic world, the global market spotlight has shifted, often rapidly, from one concern to another. We expect that pattern to continue.

A quartet of concerns

This quartet of concerns – financial stability, inflation, growth and geopolitics – is, of course, nothing new. There is scarcely a year without one being in the headlines. The Covid pandemic encompassed all four. Policy, regulation and co-operation can mitigate the risks from each of these sources, but clearly there are limits to the extent to which they can be managed. Financial stability National and global rules and regulations are in place to support financial stability. For banks, these were tightened after the global financial crisis, requiring higher levels of capital and liquidity. Overly-burdensome regulation is often criticised by those being regulated. Yet, the structure in place was insufficient to prevent the failure of SVB in March 2023. The US Fed is investigating the causes and will report in due course.1 It seems clear, however, that exposure to long-duration bonds was a primary reason. That was also the case with the problems faced by pension funds in the UK in September 2022.

When long-term bond yields rise, as they have done recently, the decline in their price can be substantial. The price of the benchmark US 30-year government bond, for example, was about 30% lower in March 2023 when SVB failed than it was at the start of 2022 (see Figure 1).

Inflation

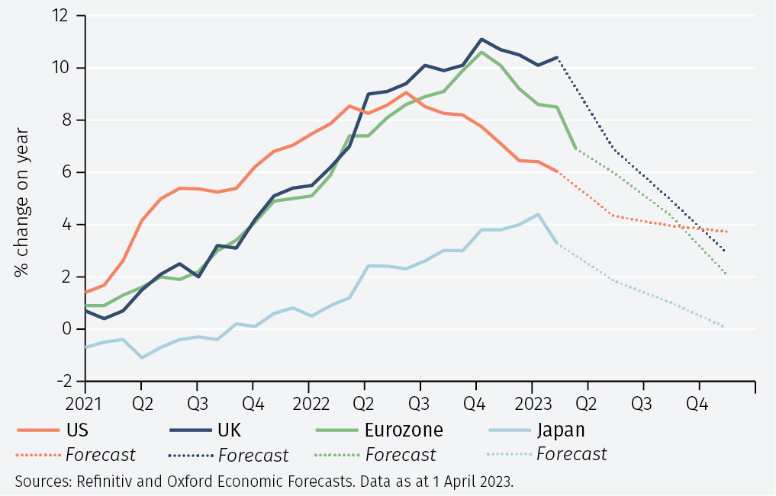

The price and yield of a thirty-year bond depends on expectations of interest rates (and, hence, inflation) over thirty years ahead. That is a long period and such expectations cannot be held with any great degree of confidence. However, such expectations were well anchored, until recently, as central banks targeted, and successfully achieved, low inflation. Their commitment to low inflation remains.2 In the US, a higher inflation target has been suggested by some.3 Now, with inflation rates falling in the major advanced economies and generally expected to be much lower by the end of the year (see Figure 2), it does not seem an appropriate time to move the goalposts.

Recession concerns

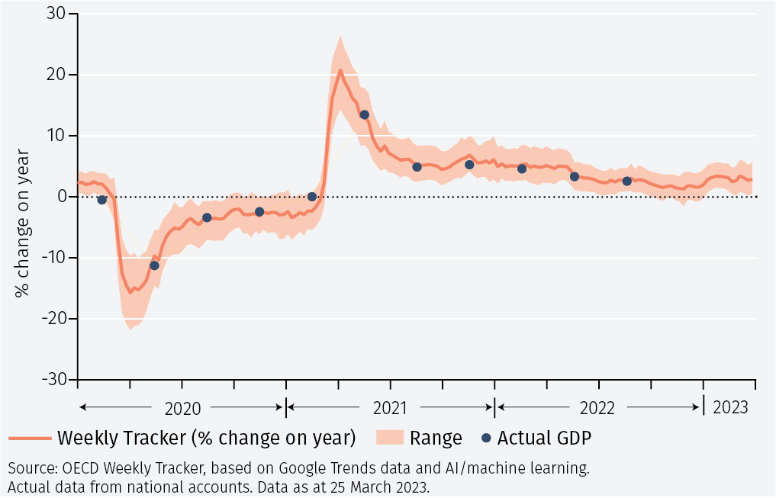

In the main advanced economies, economic growth has remained relatively stable and positive, showing no signs, as yet, of recession. That is the picture from the new weekly tracker of activity in the OECD economies (see Figure 3). China and India, neither an OECD member, are set to grow faster: by 5% and 6%, respectively.4

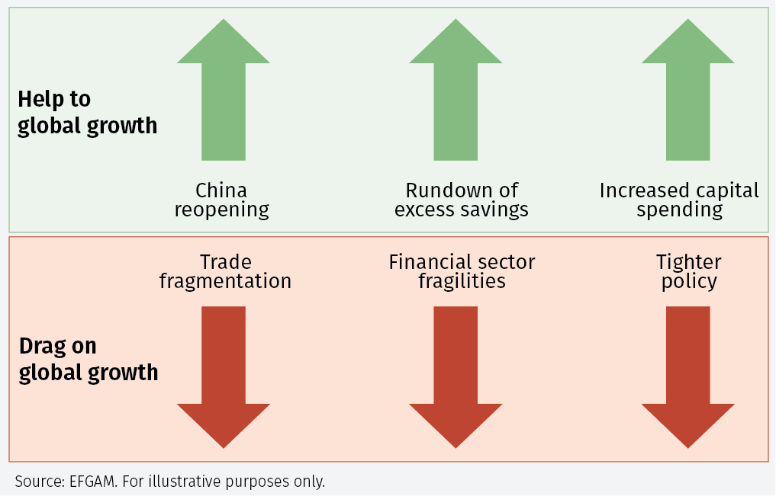

China’s reopening is one of the three main factors supporting global growth this year (see Figure 4). There, as elsewhere, excess savings built up in the pandemic can be run down to support consumer spending, the second support for growth. Global excess savings amount to almost USD 5 trillion, according to our estimates.5 Third, capital spending is being increased in three main areas: on green infrastructure; defence spending; and building new capacity as production is reshored.

Reshoring, of course, reflects the greater fragmentation of global trade. US and European domestic production of semiconductors may well be justified on grounds of national security but is almost certainly less efficient than using highly integrated global supply chains. It is most likely a drag on global growth. With financial sector fragilities still a concern and the lagged effects of tighter policy now starting to be apparent (in the housing market, most notably) global growth clearly faces headwinds. The balance between these three supportive and three dragging factors will determine the path of the global economy for the rest of the year.

Geopolitical tensions

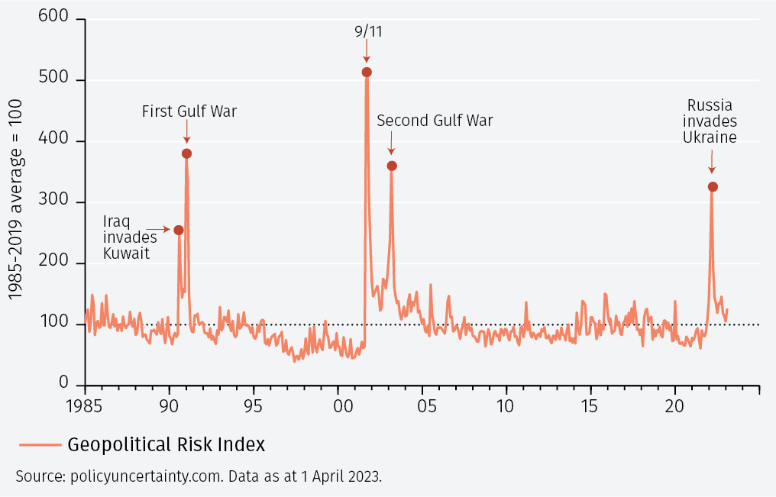

Geopolitical tensions have, according to one measure (see Figure 5) eased, although they still remain above their long-run average level. Of course, future prospects are difficult to gauge, but easing tensions is one of our key themes for 2023.

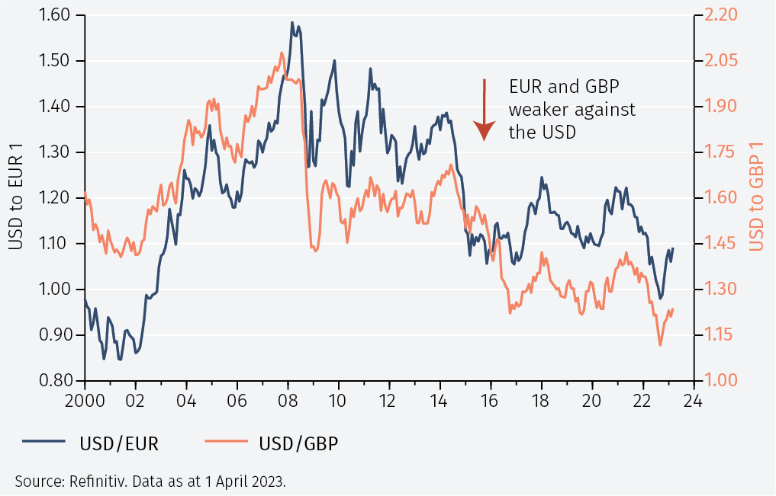

US dollar weakness

This quartet of concerns will play out in prospects for global currencies. The decline in the value of sterling and the euro against the dollar since the global financial crisis of 2008 (see Figure 6) has been a reflection of the dollar’s general strength, augmented by specific regional concerns (the euro crisis of 2009-2015 and Brexit in 2016). In the first quarter of 2023, however, both currencies recovered against the dollar. It remains to be seen whether this marks a change of trend.

1 The Federal Reserve Board review will be released on 1 May. https://www.federalreserve.gov/newsevents/pressreleases/bcreg20230313a.htm

2 The commitment was expressed by the ECB which tweeted, on Valentine’s Day, 14 February 2023, “Roses are red, Violets are blue, We will stay the course, And return inflation to 2”.

3 Olivier Blanchard, for example, has recently suggested a 3% target, lower than his earlier call for a 4% target. At a 3% rate prices double every 24 years; at a 2% rate, every 36 years . See https://tinyurl.com/yxu6emh2

4 IMF World Economic Outlook forecasts; January 2023.

5 Source: Refinitiv and EFGAM estimates as at 1 April 2023. Global excess savings are estimated as those in excess of the 2018-2019 average savings rate in the period from Q1 2020 onwards.

To continue reading, please download the full article.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.