- Date:

Insight - Although Covid concerns will feature in the first part of the year, we are generally optimistic about the outlook for global economic growth in 2022. With inflation rates set to fall back, the economic backdrop remains generally benign.

OVERVIEW

Global economic growth remains firm and inflation pressures are receding. However, political developments have unsettled some markets and will remain a theme in the second half of 2024.

Although a soft landing for global growth has materialised and inflation pressures are slowly retreating, the legacy of recent economic turbulence resonates with political developments worldwide.

Political turbulence

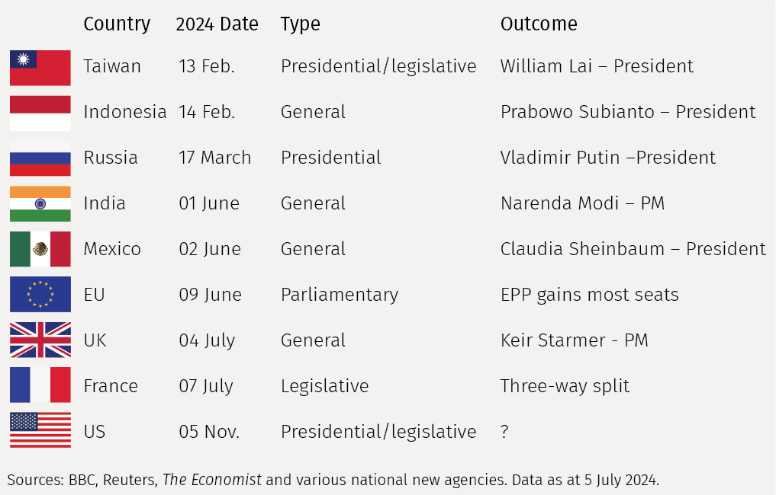

The prospect of political turbulence is one of the ten key themes in our Outlook for 2024.1 It is fair to say that this has proved apposite (see Figure 1) so far, even before the US presidential election on 5 November. In European parliamentary elections, the surge in support for France’s right-wing party, the National Rally, led President Macron to call a snap parliamentary election. In that election, the National Rally was pushed into third place, behind an alliance of left-wing parties and President Macron’s centrists. In the UK, the election of a Labour government after almost 14 years of Conservative rule reflected a general desire for change. Even so, no radical change in the direction of economic policy is planned, not least because the new government has ruled out (for now) any major changes in government revenue or spending. In particular, unchanged rates of individual, corporate and value added taxes have been promised. Such stability from the opposition party is not the case in the US, where President Trump’s agenda includes potentially large changes.

Tariffs and trade

Most significantly, Trump plans either a 10% tariff on all US imports or a 60% tariff on imports from China or, indeed, both. That could partly finance a move to make the individual income tax cuts from the 2017 Tax Cuts and Jobs Act permanent. It remains to be seen whether he is elected (the chance is currently seen as almost 60%2) and whether such plans materialise. Almost certainly, they would prove to be inflationary. One estimate is that a 10% across-the-board tariff, with full retaliation, would raise the US price level by 1.1%.3 It would therefore compound the difficulty of getting closer to the US’s 2% inflation target.

Services: inflation and trade

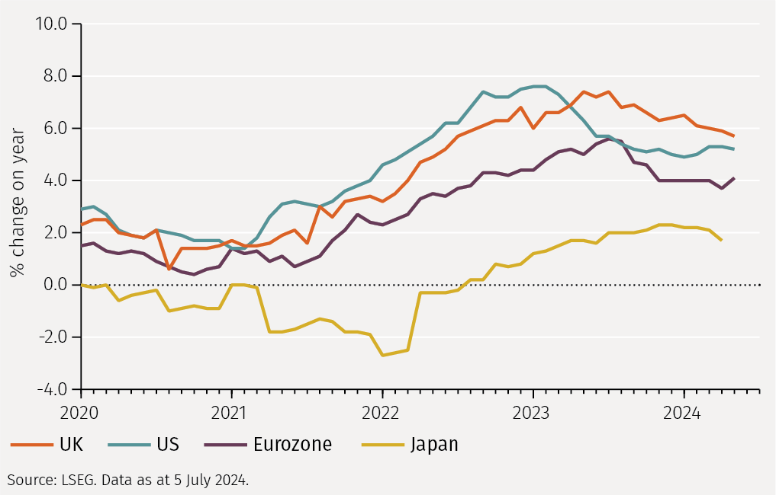

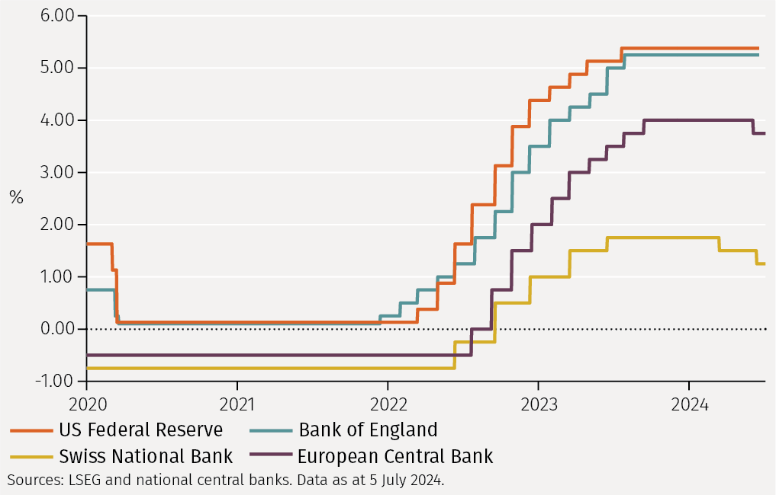

In the US, and around the world, the main reason for a stickiness in inflation is that services price inflation has remained elevated (see Figure 2). US services inflation, as measured by the personal consumption expenditure (PCE) index, peaked at 6.0% year-on-year in January/February 2023 and declined to only 3.9% in May 2024. This stickiness has led to a cautious approach to reducing interest rates, notably in the US and UK (see Figure 3).

Many services prices have a high wage cost element. With wages generally reflecting past inflation (rather than being a predictor of future inflation) and labour markets remaining tight, wage pressures generally remain elevated across all the major economies. The importance of this is that the largest share of spending by consumers (almost 70% in the US) is on services (such as travel, leisure and entertainment).

Services are important in another respect. Although international trade in services is still smaller than goods trade, it is growing more strongly (see Figure 4). Although goods trade has declined relative to global GDP services trade has not. On this basis, deglobalisation (a falling share of trade relative to GDP) is a myth, according to Richard Baldwin.4 Although increases in US tariffs are in prospect, imposing tariffs on services, many of which are digital, dematerialised and easily movable across national borders – is likely to be difficult.

To continue reading, please download the full article.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.