- Date:

Inview - In this publication we consider

significant developments in the world’s markets,

and discuss our key convictions and themes for

the coming months.

Editorial

Welcome to the November edition of Inview: Monthly Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

The correction in world equities continued in October with a decline of 3% in MSCI World over the month. Selling pressure was also evident in government bond markets, pushing the 10-year US Treasury yield above 5%, a level not seen since 2007. The rise in US yields also affected European bonds despite growing evidence regarding the relative weakness of the European economy.

The increase in US yields is partly explained by better-than-expected data on economic growth and the labour market. However, a portion of the rise in yields reflects an increase in the risk premium investors are now demanding for holding Treasuries. This in turn reflects ongoing Fed balance sheet shrinkage and may also be related the dangers associated with ongoing government shutdowns and large budget deficits.

The rise in longer dated bond yields helped create a more dovish environment for central banks, with tighter market financial conditions reducing the need for further interest rate increases.

In addition to the rise in yields, stock markets were affected by the increase in risk aversion due to tensions in the Middle East and concerns about a possible regional widening of the conflict. Such an escalation would have global repercussions if the security of energy supplies was no longer guaranteed.

Within a diversified portfolio, the allocation should continue to favour a slightly overweight exposure to both equities and bonds. Conventional and inflation protected bonds are attractive in our view at current yields. Seasonality is favourable to equities in the last quarter of the year and US firms’ reported earnings for the third quarter have beaten market expectations. Valuations have improved, particularly in the US, where an underweight exposure does not look warranted anymore. In contrast, the lack of catalysts for Swiss equities and increased uncertainty ahead of Mexican elections point to a reduced exposure to the Swiss and Latin American markets.

Asset Allocation

Global Allocation

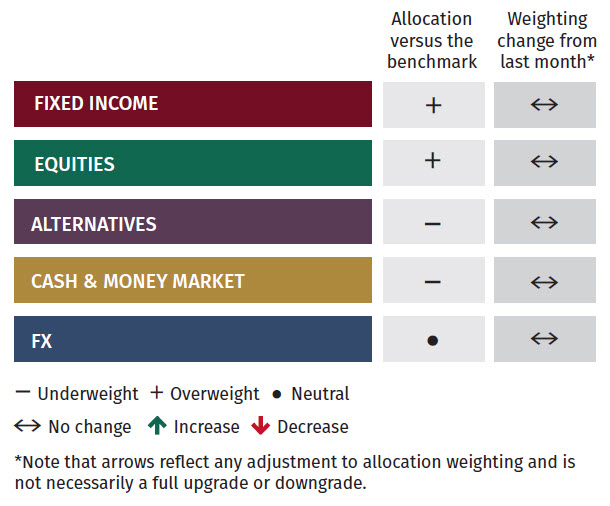

We maintain a positive outlook for equities in the coming months. This is based on factors such as historical seasonality in Q4 for equities, attractive valuations and the fact that investors have remained underweight in equities for the majority of the year and the recent sell-off, combined with positive economic data could drive a change in positioning. These could all be supportive for equities. However, we have decided not to increase further our current equity positioning, given that we are already overweight. This is due to the current positive correlation between equities and fixed income. Therefore, we decided to maintain our current overweight to equities and bonds. Our underweights to alternatives and cash were also held.

Fixed Income

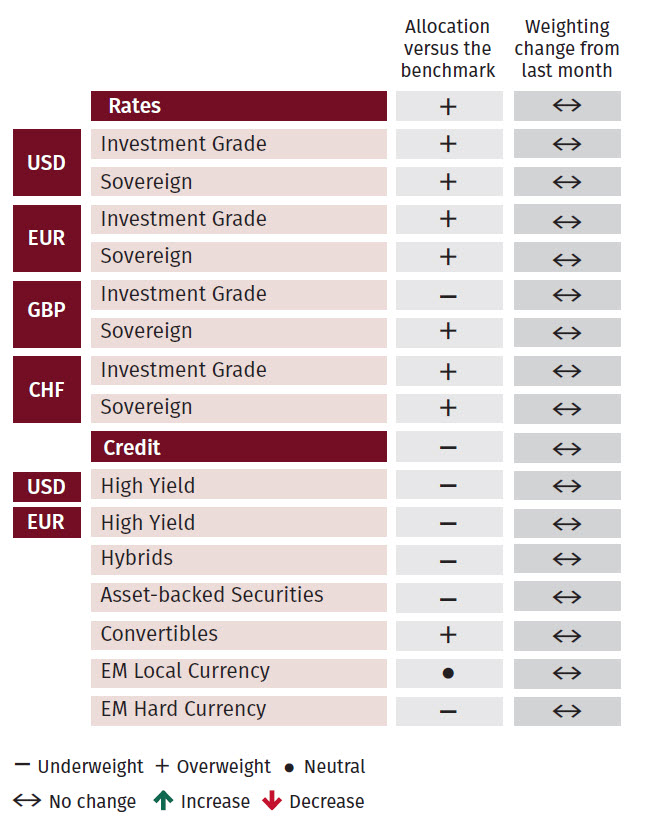

No changes are being made to the sub sectors in fixed income this month. The recent underperformance of US government bonds is not what would normally be expected in an environment of geopolitical uncertainty. We continue to favour sovereign bonds, with duration maintained at around 6.5 years. There is a preference for the middle part of the curve, while the normalization of the yield curve and pressure from investors keeps us more cautious on the long end. Exposure to indexed-linked bonds should be considered given higher real yields for USD and GBP portfolios. We maintain a positive view on investment grade bonds and convertibles, while we remain cautious on high yield credit despite the outperformance of the asset class.

Equities

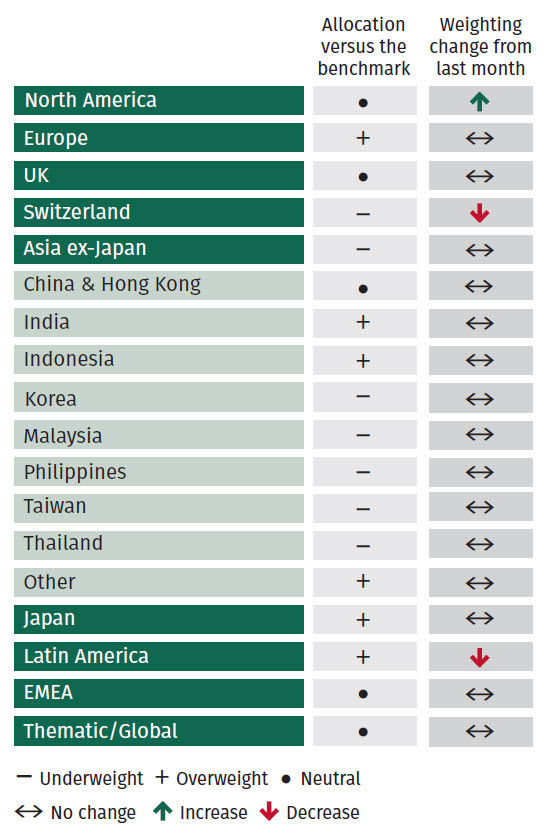

Within our allocation to equities, exposure to US equities is to be increased by 2%, bringing the position back to neutral to take advantage of seasonality effects, the pause expected from the Federal Reserve for the rest of the year and improvements in valuations. The increase is focused on US large cap growth companies. In order to fund this, our allocation to Swiss equities is to be reduced by 1% given the lack of catalysts in this market to remain neutrally positioned, as well as taking profits from the currency gain. In addition, we are also reducing Latin American equities by 1%, although it will maintain a small overweight. Within Latin America, political uncertainty in the region has played a part in the recent underperformance. However, Latin American equities have benefited from returns of over 4% year-to-date.

Alternatives

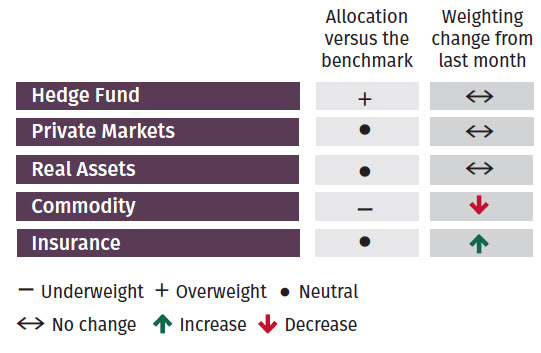

Within alternatives, commodity exposure is being reduced to an underweight position. The reduction to gold and broader commodities is due to the higher US interest rate environment and continued slowdown in the global economy that might curb demand. Meanwhile insurance-linked securities were upgraded up to neutral. Current yields in the asset class around 13% make this an attractive asset class with no correlation to other parts of the market.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document. The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.

Independent Asset Managers: in case this document is provided to Independent Asset Managers (“IAMs“), it is strictly forbidden to be reproduced, disclosed or distributed (in whole or in part) by IAMs and made available to their clients and/or third parties. By receiving this document IAMs confirm that they will need to make their own decisions/judgements about how to proceed and it is the responsibility of IAMs to ensure that the information provided is in line with their own clients’ circumstances with regard to any investment, legal, regulatory, tax or other consequences. No liability is accepted by EFG for any damages, losses or costs (whether direct, indirect or consequential) that may arise from any use of this document by the IAMs, their clients or any third parties.