- Date:

- Author:

- Sam Jochim

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

Inflation in Japan has been above the Bank of Japan’s 2% target since April 2022. Despite this, the central bank has remained the global outlier and maintained ultra-loose monetary policy. In this Macro Flash Note, Economist Sam Jochim looks at what can be expected from the BoJ’s meeting on 28 July.

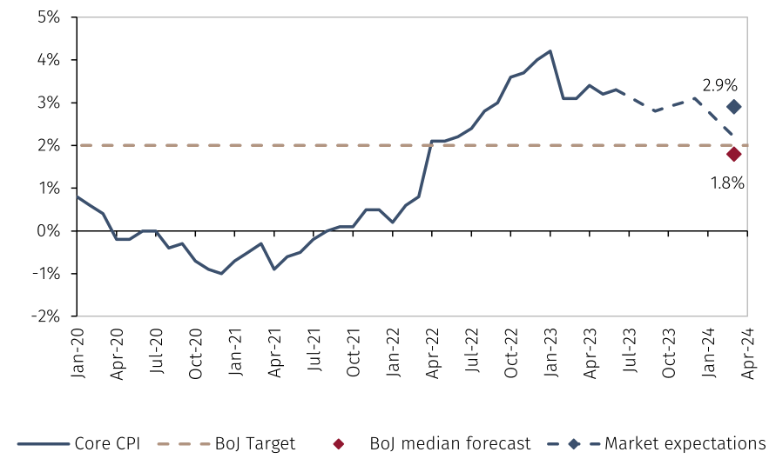

At its meeting on 16 June, the BoJ maintained its policy rate at -0.10% and announced that it would continue to target a yield of 0% on Japanese government bonds (JGBs) with a 10-year maturity, allowing the yield to fluctuate 0.5 percentage points either side of this.1 This decision came despite core inflation, which excludes fresh food prices, having been above the BoJ’s 2% target for 13 months (see Chart 1).

Source: Refinitiv, FactSet and EFGAM calculations. Data as at 21 July 2023.

In justifying its decision not to alter monetary policy in June, the BoJ pointed to expectations that the inflation rate will decline towards the middle of fiscal year 2023 (FY23).2, 3 The previous meeting in April saw the median BoJ policy board member forecast core inflation of 1.8% in FY23.4

However, core inflation in the first three months of FY23 averaged 3.3%. Although markets expect a deceleration in the remaining nine months, they predict core inflation will average 2.9% over the entire fiscal year. It is likely the inflation forecasts produced at the July meeting continue to project a decline in the second half of FY23.

Given the upside surprises to inflation data so far, and an apparent change in corporate price setting behaviour, the BoJ is unlikely to forecast average core inflation below 2% in FY23. However, this does not mean the BoJ will raise interest rates in July. While it has noted upside risks to inflation due to the possibility of firms passing on cost increases for longer than expected, there are also downside risks due to slower than expected growth in the US and China.

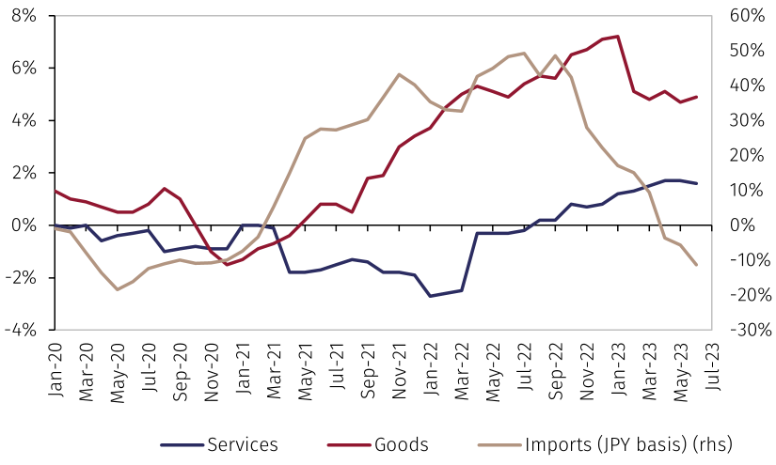

Furthermore, the BoJ views high CPI inflation at the start of the fiscal year as being driven by a pass-through of cost increases led by a rise in import prices, and not by a pass-through of wage increases to services prices, as evidenced by goods inflation outpacing services inflation (see Chart 2). Import prices have fallen recently although there is a lag with which these appear in consumer prices.

Source: Refinitiv and EFGAM calculations. Data as at 21 July 2023.

It is interesting to note that BoJ Governor Ueda has a history of voting against tightening monetary policy. He previously did so in August 2000, arguing it was too early to tell if inflationary pressures would be sustained and that the cost of waiting was low.5 Any move away from negative interest rates is likely to be well signalled and could follow the completion of the broad review of the impact of the BoJ’s monetary policy over the last 25 years.6 This is expected to be completed in Q2 or Q3 2024.7

While the cost of maintaining negative interest rates is viewed as low, the same is not true of the BoJ’s yield curve control (YCC) policy. 10-year JGB yields currently sit just below 0.50%, requiring purchases by the BoJ to defend the upper bound of its target. The desire to prevent volatility in interest rates means tweaks to the upper and lower bounds are likely before changes to the target. A small adjustment could happen at the meeting in July. However, to prevent pre-emptive selling of 10-year JGBs, the BoJ is disincentivised from providing advanced notice of this.

To summarise, inflation in Japan has remained above the BoJ’s 2% target since April 2022 but has been driven largely by supply side factors that are not strongly influenced by monetary policy. The BoJ is likely to raise its inflation forecasts at its meeting on 28 July. However, given uncertainty surrounding the inflation outlook, the ongoing review of monetary policy that is expected to conclude in 2024, and the perceived low cost of waiting, the BoJ is highly unlikely to increase interest rates; any move away from negative interest rates is likely to be well signalled. However, a tweak to the YCC policy is possible in July or at future meetings in 2023. This may well be a precursor to a more meaningful shift in policy next year once the monetary policy review is complete.

1 The Bank of Japan’s policy which targets a 0% yield on 10-year Japanese government bonds is commonly referred to as yield curve control (YCC).

2 ‘Summary of Opinions at the Monetary Policy Meeting on June 15 and 16, 2023’ https://www.boj.or.jp/en/mopo/mpmsche_minu/opinion_2023/opi230616.pdf

3 Fiscal year 2023 began on 1 April 2023 and ends on 31 March 2024.

4 'Outlook for Economic Activity and Prices, April 2023’ https://www.boj.or.jp/en/mopo/outlook/gor2304b.pdf

5 'Japanese monetary policy: 1998-2005 and beyond’ https://www.bis.org/publ/bppdf/bispap31i.pdf

6 'Review of Monetary Policy from a Broad Perspective’ https://www.boj.or.jp/en/mopo/bpreview/index.htm

7 'Statement on Monetary Policy, 28 April 2023’ https://www.boj.or.jp/en/mopo/mpmdeci/mpr_2023/k230428a.pdf

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.