- Date:

- Author:

- Stefan Gerlach

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

Stefan Gerlach

On 26 and 27 July, the Federal Reserve and the European Central Bank will meet to set monetary policy. In normal conditions, setting monetary policy involves weighing the outlook for inflation against the outlook for economic activity. Often there is tension between these objectives as higher interest rates slow both inflation and economic growth, requiring a careful calibration of monetary policy.

Today, with inflation so far from both central banks’ 2% objectives, it is the focus of policy makers’ attention. In contrast, the outlook for economic activity plays little role in the policy decisions. Indeed, both central banks may desire growth to slow as it is a determinant of future inflation.

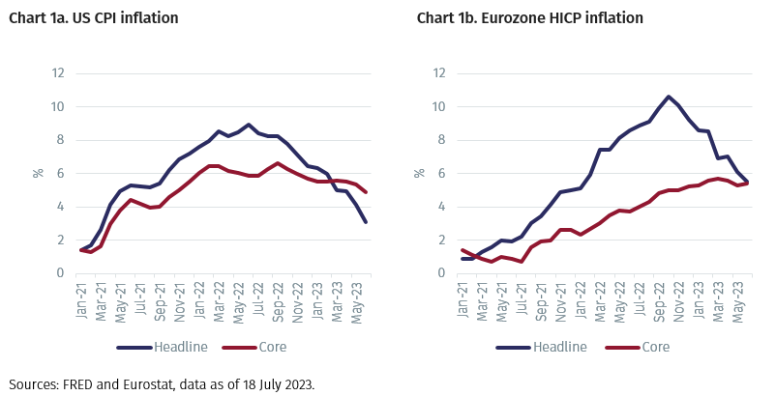

The figures below show just how far from 2% headline inflation (inflation computed using all the components of the CPI) and core inflation (inflation disregarding the volatile food and energy components1) stand.

The figures illustrate that the inflation problem in the eurozone is more adverse than in the US. The peak rate of inflation was higher in the eurozone (10.6%) than in the US (8.9%). The peak in the eurozone is also more recent (October 2022) than in the US (June 2022). Furthermore, headline inflation in June was higher in the eurozone than in the US (5.5% vs 3.1%) as was core inflation (5.4% vs 4.9%)2. Finally, while core inflation rose in the eurozone in June from 5.3% to 5.4%, it fell sharply in the US from 5.3% to 4.8%.

Central banks attach greater focus to core inflation than headline inflation since they view the latter as being subject to temporary erratic swings arising from disturbances to energy and food prices. While headline inflation has fallen sharply in both economies in response to falling energy prices, core inflation has fallen much less, if at all. Excluding its recent decline in the US in June, core inflation has fluctuated between 5.3% and 5.7% in the US and eurozone since December 2022.

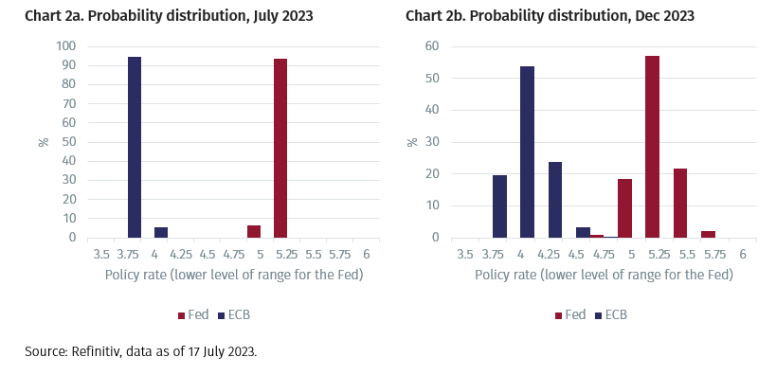

With little clear sign of core inflation declining, the Fed’s Federal Open Market Committee and the ECB’s Governing Council are both expected to raise interest rates this month.3 Market pricing suggests that the perceived probability of an interest rate increase is about 95% in both cases.

Market pricing for December suggests that little change in policy is expected during the autumn. While market participants view the ECB as being most likely to raise interest rates one more time later this year, the Fed is expected to stay put. Of course, in both cases market participants attach some probability to rates being above or below the most likely outcome.4

In conclusion, with core inflation stuck significantly above 2%, market participants expect the Fed and the ECB both to raise rates this month, and the ECB to raise rates once more in the autumn. How policy will evolve in practice will depend on the behaviour of core inflation. If it were to fall more rapidly than is currently expected, the turn in monetary policy could come earlier than expected. And if it were to continue to fluctuate at current levels, further interest rate increases become more likely.

1 For the eurozone measure, the prices of alcohol and tobacco are disregarded too.

2 The data for the eurozone for June 2023 are flash estimates.

3 While the ECB sets interest rates at point (currently 3.5%), the Fed uses a range for its policy rate (currently 5-5.25%). The graph refers to the lower end of that range.

4 Interestingly, the distribution is symmetric, implying that they attach an equal likelihood to interest rates being at a level above or below the most likely outcome.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.