- Date:

- Author:

- Sam Jochim

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

The latest Federal Open Market Committee (FOMC) minutes provide a window into the Fed’s thinking at its February meeting. In this Macro Flash Note, Sam Jochim examines the implied policy bias of the Fed with the help of EFGAM’s Fed Hawkishness Indicator.

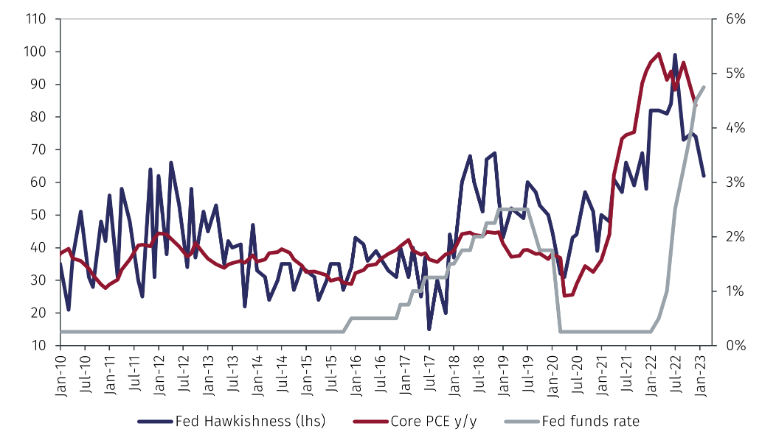

The EFGAM Fed Hawkishness Indicator (FHI) aims to track the policy mood inherent in the FOMC meetings (see Chart 1). It does so by counting the number of times key terms such as “elevated”, “robust”, “high”, and “strong” are repeated in FOMC meeting minutes. The output simply represents the number of times each key term appears.

Source: Fed, Refinitiv and EFGAM calculations. Data as at 23 February 2023.

A notable characteristic of the indicator is its volatility. While large meeting-to-meeting moves may reflect a rapidly changing economic environment, they also imply a level of caution is needed when interpreting the indicator. Looking past short-term volatility to longer term trends is more informative.

One of these trends is the correlation between the FHI and the core personal consumption expenditure (PCE) price index. From January 2010 to December 2022, the FHI has a correlation with year-on-year core PCE inflation of 72%. Unsurprisingly, the recent downward trend in core PCE inflation was associated with a reduction in the FHI.

The relationship between the FHI and the Fed funds rate is also notable. The FHI rose rapidly before the Fed funds rate was increased in March 2022. The FHI appears to have peaked in July 2022, when the FOMC voted to increase interest rates by 75 basis points for a second time. As the FHI declined, the Fed continued to hike by 75 basis points at each of the two following meetings, before slowing the pace of rate increases to 50 basis points in December and 25 basis points in February. It appears that in the most recent monetary policy cycle, the evolution in the tone of the FOMC has signalled changes in the size of interest rate increases.

Despite the recent easing of the FHI, the indicator remains elevated, and its decline should not be overstated. The minutes of the February FOMC meeting highlighted that the Fed is attentive to inflation risks, and cautious not to under-tighten or stop before inflation is sustainably returning towards its 2% target.1 Communicating this effectively is further incentivised by the desire to anchor long-term inflation expectations.

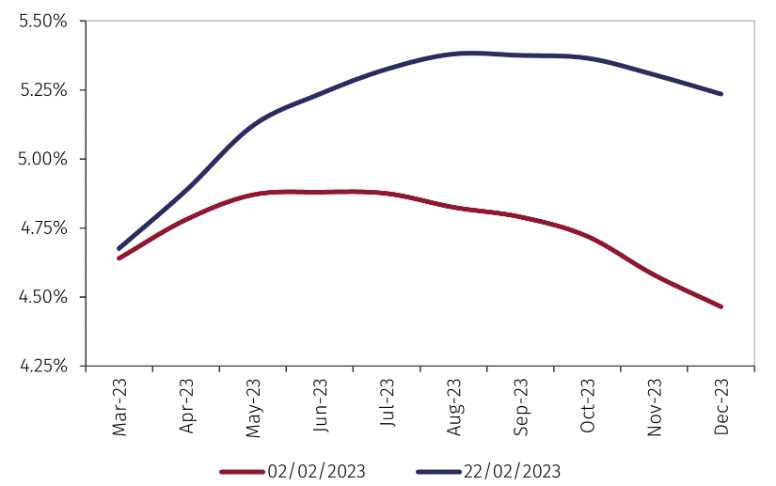

Market expectations based on Fed funds futures on 22 February pointed to uncertainty regarding whether the Fed would hike by 25 or 50 basis points at its next meeting (see Chart 2). Furthermore, expectations for the Fed funds rate at the end of 2023 have increased significantly. The upward shift in expectations relative to 2 February reflects recent stronger-than-expected data, with the labour market notably continuing to remain tight.

Source: Refinitiv and EFGAM calculations. Data as at 23 February 2023.

Despite this, the FOMC minutes pointed clearly to continued tightening at a pace of 25 basis points. The bar will be high for the Fed to raise rates by 50 basis points again as it would indicate a material deterioration in the inflation outlook.

To conclude, the hawkishness of the FOMC remains elevated, although it has recently eased. Markets are uncertain about the size of the Fed funds increase at the March meeting, with a 20% probability attached to a 50 basis point move. The minutes of the February FOMC meeting, as captured by the FHI, point to continued rate increases of 25 basis points until the Fed sees sufficient evidence that inflation is sustainably headed towards the 2% target.

1 https://www.federalreserve.gov/monetarypolicy/files/fomcminutes20230201.pdf

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.