- Date:

Review of 2021 Outlook

Each December, we review the Outlook we presented a year earlier. Overall, we scored 8/10.

1Correct |

Synchronised global economic recoveryWe thought that there would be a synchronised recovery in world economic growth in 2021. That did happen. World growth will be 5.7% in 2021 on the basis of the IMF’s latest forecasts (made in October). All of the main regions are set to have grown by 5%- 6%, a degree of synchronous growth which has rarely been seen in the past.

|

2Correct |

Digital consumersWe saw changing consumer spending patterns as a big theme for 2021 – some a continuation of pre-pandemic trends, others part of a bigger structural change. The trend move to online retail sales continued, despite a reduction in the online share in the immediate aftermath of re-opening (notably in the UK market). The move to online sales of services is not captured in most statistics, which cover just sales of physical goods. But the growth in such sales (of financial products, online gaming, video downloads and social media content, for example) is arguably just as important a trend.

|

3Correct |

Climate change and creative destructionWe expected 2021 to be a year when the forces of creative destruction (with new technologies replacing old ones) and the requirements of climate change would come together. But the speed with which this has become an urgent issue has surprised many. The IEA World Energy Outlook estimates that limiting global warming to 1.5°C will require a surge in annual investment in clean energy projects and infrastructure to nearly USD4 trillion per year by 2030.

|

4Incorrect |

Inflation stays lowWe expected inflation to stay low. In most economies it did not (Japan being a notable exception). At the end of 2021 there was a keen debate about whether the rise would prove transitory or more permanent. We think it will be transitory. Furthermore, forward inflation expectations still remain well anchored, close to central banks’ 2% targets.

|

5Correct |

Big government stays bigGovernment spending remained a large share of GDP in 2021, as we expected. There are now measures to either increase taxes to pay for higher spending (as in the US and the UK) or restrain spending to some extent. But this comes up against the need to spend on the clean energy infrastructure (governments will play their part although most of the financing will come from the private sector).

|

6Correct |

Fixed income opportunities remainWe thought that, despite low yields in the major developed government bond markets and little prospect for capital gains, there were attractive opportunities in three other areas of the fixed income markets: exposure to wealthy nations, convertible and emerging market debt. These areas did produce higher returns than global government and investment grade bonds.

|

7Partly correct |

Small is beautifulWe looked for small companies to do well relative to large cap companies. In China, emerging markets and Asia ex-Japan that was the case: small cap stocks significantly outperformed large cap stocks. But large cap stock returns beat small cap returns in the US and Japan; and returns from the two sectors were broadly similar in Europe.

|

8Correct |

Big tech consolidatesWe expected that big US tech companies would consolidate their market position in 2021. We thought that such companies’ strong cash flow generation and their strong balance sheets justified their valuations and such companies could continue to do well after several years of strong performance. That did happen, with the tech sector producing marginally higher returns than the overall market (ex-tech) in 2021.

|

9Partly correct |

Healthcare opportunitiesDespite the attractive valuations of the sector and the structural factors supporting it, the US healthcare sector underperformed the overall US S&P 500 index in 2021. Even so, returns were substantially positive (15.7%) in the year to 1 December 2021; and there were some attractive returns in specific healthcare companies.

|

10Correct |

Global co-operation reinventedGlobal co-operation was indeed reinvented in 2021 and, in several key aspects, improved. Although tensions between the US and China and between the UK and the EU remained, measures to tackle climate change and to establish a common minimum corporation tax rate were notable milestones in the move to greater co-operation.

|

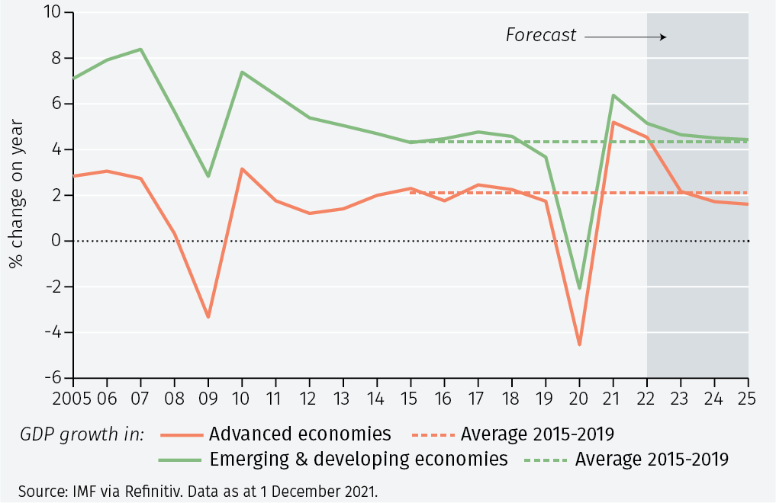

1. Global growth above trend

We expect global growth will stay strong in 2022, around 4.5%. Growth will be above the pre-Covid trend, but will fade into 2023.

We expect global economic growth to remain strong in 2022, at around 4.5% in the advanced economies and 5% in the developing and emerging economies (see Figure 1a). After a strong finish to 2021, however, and with renewed restrictions due to the Covid Omicron variant, 2022 is likely to start on a weak note.

Such a growth rate for the advanced economies will be more than twice the 2.1% seen in the five years prepandemic. It will be driven by continued progress with the fight against Covid – particularly an increase in vaccination rates in the countries that have lagged behind and the roll-out of new therapies, in particular a Covid pill – a rundown in accumulated savings, a rebuilding of inventories and an easing of supply chain bottlenecks. The advanced economies’ growth rate will then fade, in subsequent years, towards the potential long-run rate of around 1.5%-2%.

Growth in the emerging and developing countries will be only a little above its pre-Covid average in 2022. Most significantly, China’s growth will slow – although at around 5% it will still be strong by most standards.

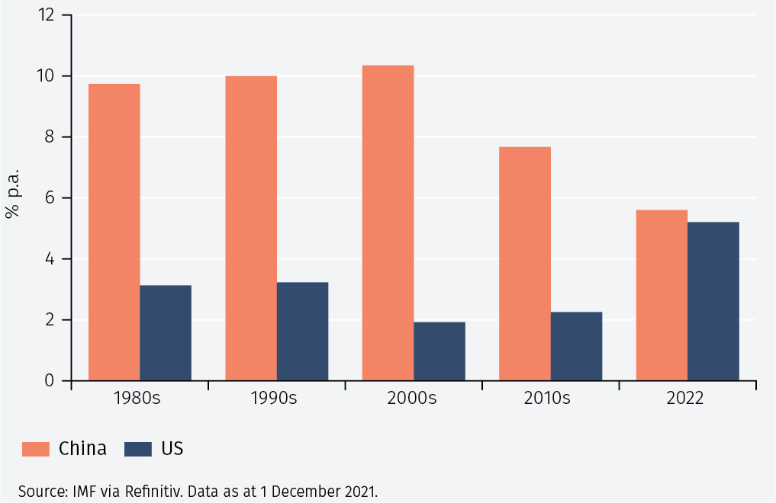

2022 may see, for the first time in decades, US growth come close to that in China (see Figure 1b). Given that President Biden has said that the US is in a contest with China about whether western free market economies or eastern autocracies work best, such a development would support the US. That would be especially the case if China succumbed to a full-blown credit and property market bust (which, after all, the US has experienced several times in its history). By the way, we think it won’t.

Elsewhere in Asia, we look for a boost from opening up in the ASEAN economies – admittedly a somewhat uneasy grouping, given developments in Myanmar – and India looks set to grow strongly. Its vaccine rollout, after a slow start, has progressed very well and we find the restructuring of the economy – particularly the growth of the e-commerce sector – encouraging. Brazil looks set to be mired in political uncertainty ahead of the presidential election at the end of the year – which may see the re-election of former president Lula. And despite the benefit of high oil and gas prices, Russia’s growth looks likely to be sluggish.

2. Spending spree

As Covid concerns recede in 2022, consumers will be willing to spend more, particularly from their accumulated savings. Spending on leisure and healthcare will be two key areas.

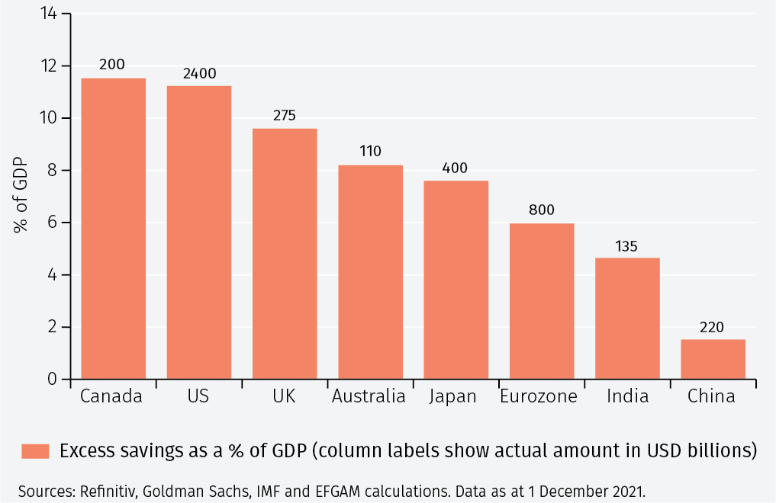

Pent up demand and accumulated savings will support a spending bounce back in 2022. How quickly that bounce occurs depends, of course, on the progress with reducing Covid (and, particularly, its omicron variant) but we do see consumer confidence being steadily rebuilt.

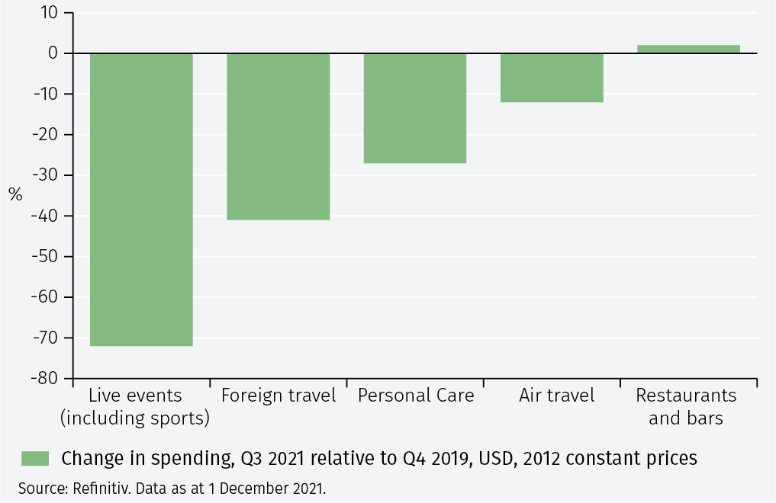

The US and the UK, two economies with large accumulated excess savings (see Figure 2a), look set to benefit the most. We see two major themes. First, spending on leisure activities will recover. In the US, spending in some categories – such as live events, foreign travel and personal care – is still well below pre-pandemic levels (see Figure 2b).

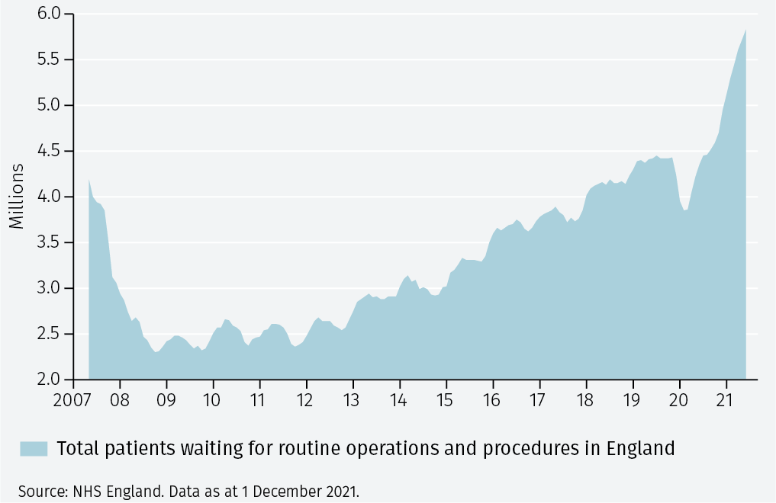

Second, we expect greater spending on healthcare. As resources in the healthcare system were diverted towards the Covid pandemic, a backlog of patients waiting for other medical procedures has built. In the UK, for example, 5.9 million people are waiting for treatment (see Figure 2c). We expect higher spending in this area both by the state and consumers themselves.

Supply shortages (such as of new and used cars) and a lack of skilled labour (for home renovations, for example) have tended to raise prices in many areas of consumer spending. We think this greater pricing power by companies will remain an important theme, especially in areas, such as the airline industry, where capacity has been reduced.

3. Emerging markets go digital

Emerging economies have typically lagged behind the advanced economies in the move towards digitalisation. On many fronts, we see them making substantial progress in 2022, raising interesting investment opportunities.

Digitalisation is set to become a more prominent trend in emerging and developing countries in 2022. The basic building blocks for greater digitalisation are already in place. 90% of people aged under 30 live in such economies;2 that age group is typically much more likely to adopt digital technologies, especially smartphone-based applications; and the required infrastructure, notably mobile phone networks, are either in place (as they are typically easier to install than fixed-line networks) or are being introduced. Smartphone penetration in developing economies is actually higher than in developed economies, according to one survey, although 4G connectivity is still lower.3

The services which we see as particularly interesting in this move to digitalisation are mobile banking, ride sharing and online retail sales. Around the world, there are interesting examples of companies in those sectors likely to come with IPOs (Initial Public Offerings) in 2022.

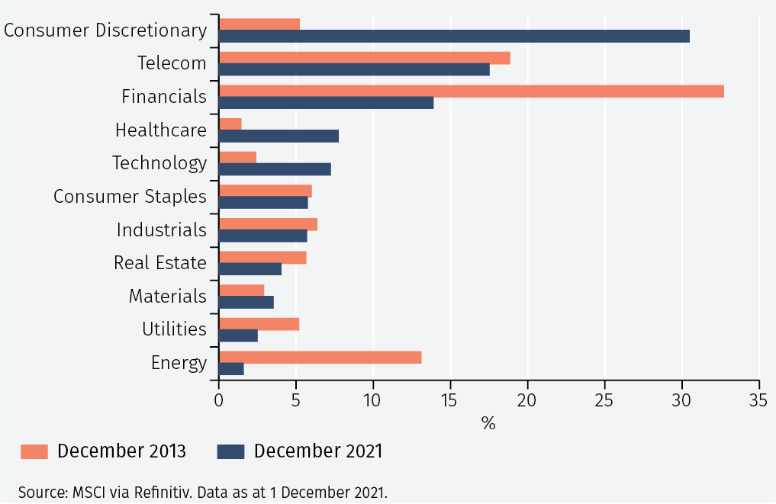

Of course, not all emerging economies are at the same stage of digital development. In Africa, the M-Pesa mobile payment network is already well established and e-commerce services are being added to that platform. Moreover, China is already a leader in many areas of digitalisation. As a result, we have seen the nature of the Chinese equity market change in recent years (see Figure 3). The consumer discretionary, technology and telecom sectors, where predominantly private sector companies are represented, often provide products and services similar to their better-known US counterparts. They are now three of the largest sectors. Their increased share has come as the relative importance of energy, utilities and industrial companies (often State-owned enterprises) has declined. These changes in China give an indication of the prospective changes in other emerging equity markets as digitalisation progresses; changes which will create much more interesting investment opportunities.

4. Inflation proves transitory; risks of a policy mistake

The hardest call for 2022 is whether inflation does prove transitory or not. We think, on balance, it will, with US inflation dropping back to 2-3%, but not until the second half of the year. There is a risk policymakers make a mistake.

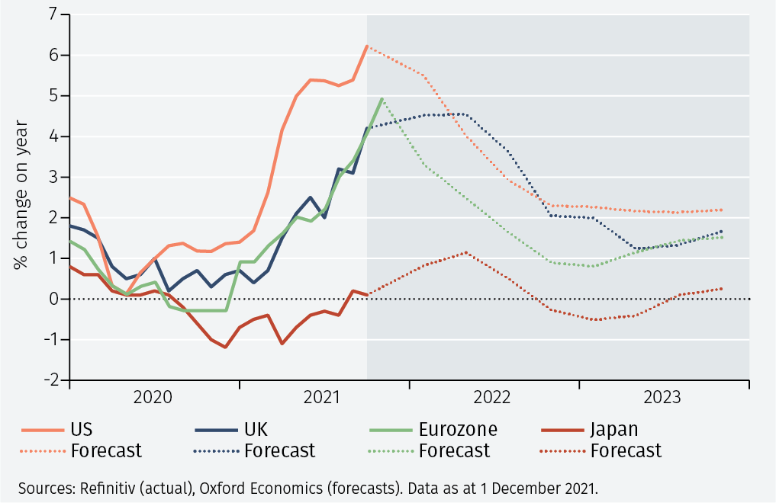

We think higher inflation in the US, UK and eurozone will prove transitory, falling back towards 2% in the second half of 2022 (see Figure 4a). Inflation in Japan will only briefly rise above 1%. That decline will be driven by base effects – a comparison with strong price increases in the corresponding months of 2021, easing supply chain issues and, potentially, weaker oil and commodity prices.

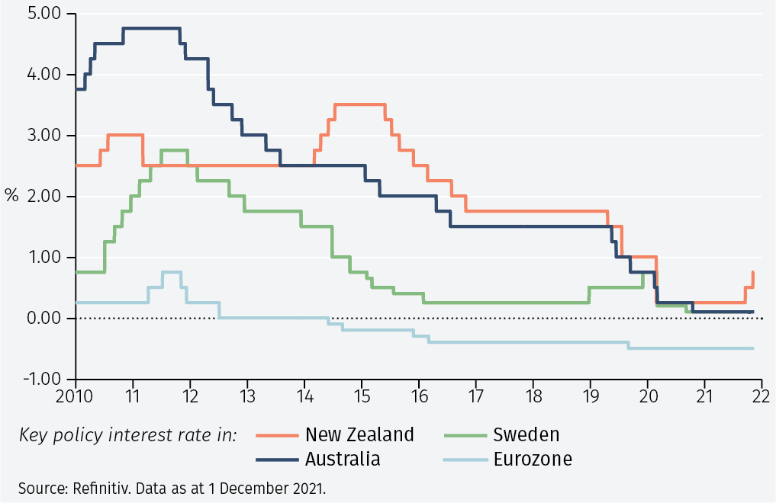

There is a risk, however, of central banks making a policy mistake. There are three ways in which this could happen. First, they may overestimate the role played by demand in the rise of inflation. Second, they may underestimate the sluggishness of inflation and argue that the fact that it stays high even though supply factors have moderated is evidence that tighter policy is necessary. Third, they may underestimate the collective amount of tightening they are doing. As a growing number of them tighten policy, the contraction of global aggregate demand may be greater than they anticipate. The latter is a particular concern in emerging markets, where tightening has been swift and marked, in response to the inflation threat. Since the global financial crisis, there have been several examples of central banks raising rates, only for these moves to be subsequently reversed (see Figure 4b).

The risk is that they make the same mistake again. Outlook

5. Savings and green infrastructure

For several years, real interest rates have been kept low by a savings glut. Now, there is an urgent need to deploy those savings to finance the green infrastructure. 2022 will be a year when that imperative is clearly recognised.

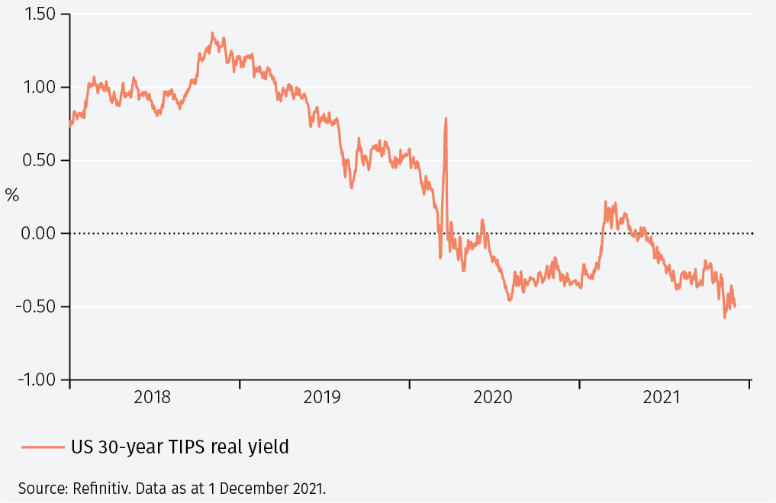

The real yield on US TIPS (Treasury Inflation-Protected Securities) fell to new lows, well into negative territory for 30-year bonds, in late 2021 (see Figure 5a). That is, the US government can lock in negative real borrowing costs for the next three decades. There are three main explanations of why this situation has arisen: substantial central bank purchases of government bonds, depressing their yield; secular stagnation – lower long-term trend growth driven by weak demand; and, reflecting high savings and low investment spending, a global savings glut.4

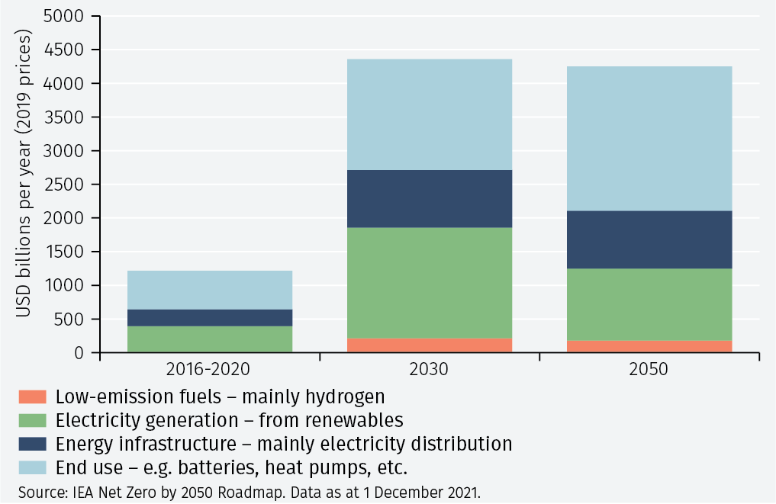

Now, the needs for the clean energy infrastructure to meet net zero carbon emissions by 2050 are massive (see Figure 5b). Running at USD 4 trillion per year for the next quarter century, USD 100 trillion will need to be spent in total.

Clearly, if there is a global savings glut depressing real yields, then mobilising these funds to invest in clean energy could achieve the desirable goals of limiting global warming to 1.5 degrees, while restoring real yields to a more appropriate level and generating a welcome boost to growth and employment.

But will that happen? Mobilising the excess savings is no easy task. ‘De-risking’ by many institutional investors, notably defined benefit pension schemes and insurance companies, has actually been encouraged by post-financial crisis regulatory changes. They are often more inclined towards the relative safety of fixed income assets than equities, leave alone long-term infrastructure projects. Sovereign wealth funds and central banks may have the resources to invest, but they too are typically conservative investors. Governments themselves could provide the financing, but many are concerned about their high debt levels, which have risen further as a result of Covid support measures. Nevertheless, the imperative to finance the green infrastructure will be much more widely recognised in 2022 and tangible progress will start.

6. Japan’s quarter-century convalescence

Japan’s economy continues its recovery and we think the equity market can make further progress in getting back to its 1989 peak.

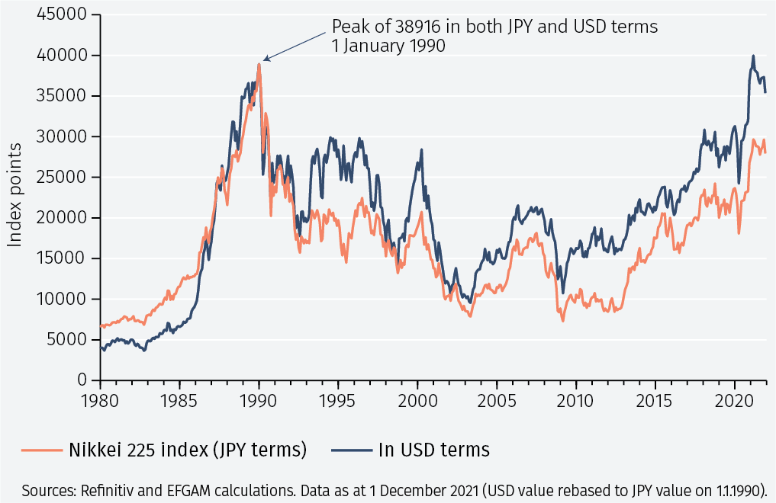

Japan’s broad stock market indices peaked at the end of December 1989 and then fell by more than 80% to a low point in late 2009 (see Figure 6a). The recovery since then has been steady and although the overall market is still around 20% below its peak in yen terms, it has regained its previous peak in US dollar terms.

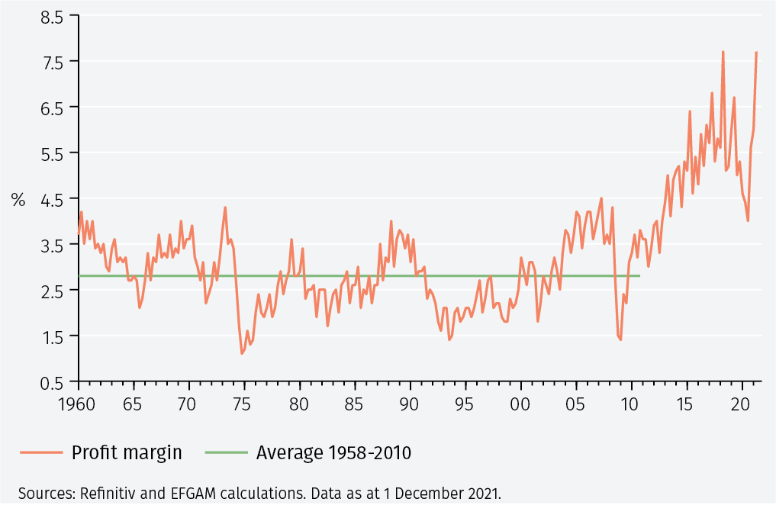

We think the market can make further progress in 2022. There are three main reasons. First, earnings growth should be strong. Profit margins are now well ahead of their historic average (see Figure 6b); export sales growth will be helped by a broader re-opening of the global economy, especially in other Asian economies; and domestic sales will be supported by a reopening to business travel and tourism.

Second, the Japanese yen is at a competitive level against the US dollar: JPY 114/USD on 1 December 2021, weaker than the JPY 110/USD rate at which Japanese companies are generally seen as competitive in international markets.

Third, most foreign investors have been net sellers of Japanese equities for a number of years. Net foreign sales amounted to JPY 25 trillion from 2015-20205 and are underweight exposure to the market. That started to change in 2021 and, we think, will continue.

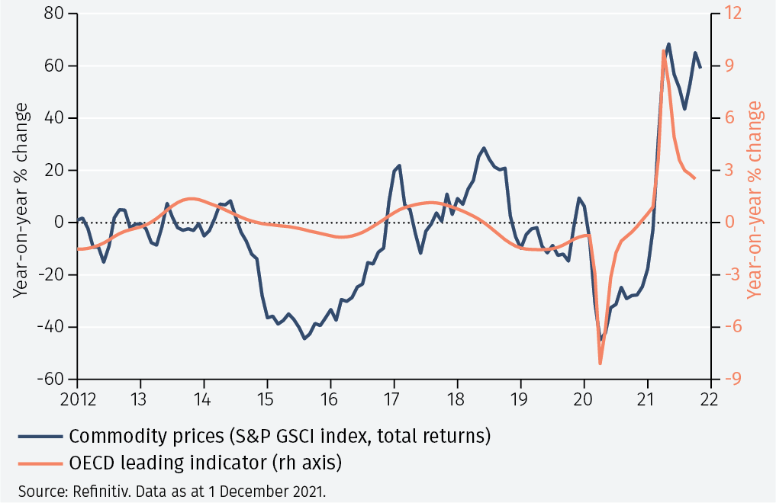

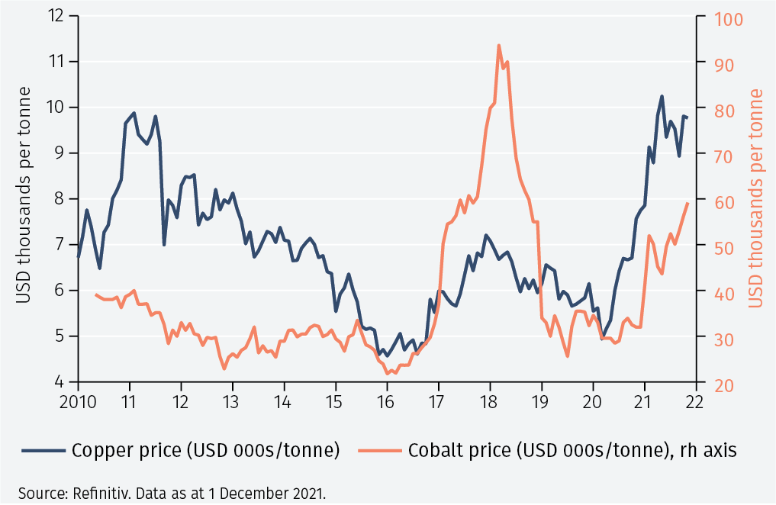

7. Commodities: spotting the winners

After a strong increase amidst supply shortages in 2021, we think commodity prices will ease back in 2022. Picking winners will be important: structurally, copper and cobalt remain favoured.

We see general softness in commodity prices in 2022, driven by weaker global economic growth (see Figure 7a).

Weaker demand in China, which accounts for half of the consumption of most industrial commodities, will be an important driver.6 But 2022 is set to be a year in which the overall trend in commodity prices may be less important than spotting individual winners. Structural factors – especially the transition to clean energy – favour strength in commodities such as copper and cobalt, given their use in electric vehicles and the new energy infrastructure. An electric vehicle uses up to 3½ times as much copper as an internal combustion-engine car.7 The trend future decline in the use of fossil fuels argues for weakness in oil and coal prices. But limitations on oil exploration and development may crimp supply before demand is substantially reduced, especially if the transition to EVs is slower than many expect. Expect the path of the oil price to be rocky again.

So, weaker commodity prices – but with copper and cobalt holding up better than oil and coal – is our call.

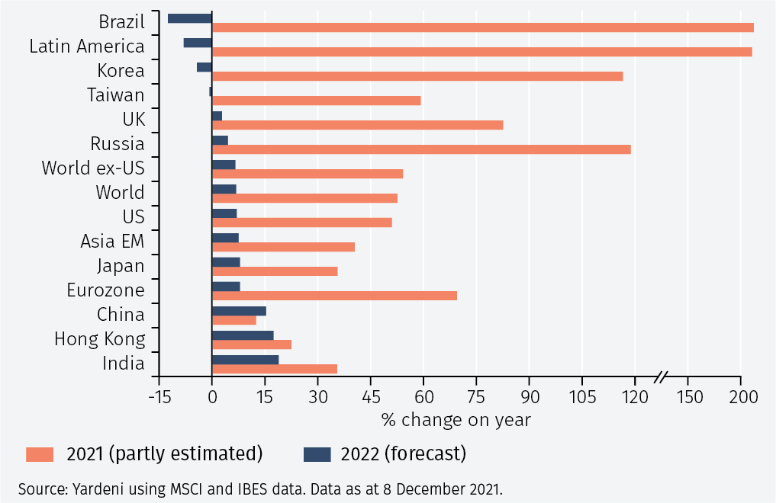

8. Tougher time for earnings

2022 will be a more normal environment for corporate earnings, after the sharp swings in the last two years. The biggest positive surprises will, we think, be in Asia. But the US market still remains the one to beat.

After a terrible year for global corporate earnings in 2020 but a spectacularly good year in 2021 (see Figure 8a) corporate earnings growth is set to return to a more normal pace in 2022. However, after a strong fourth quarter of 2021 and with renewed concerns about the Covid Omicron variant, the first quarter of the year may see some weakness in earnings.

In the US, we see earnings growth running at around a ‘typical’ rate of 5-10%. Cost pressures weigh on earnings, but companies have, in aggregate, generally been good at maintaining and even improving profit margins. That should continue in 2022.

Re-opening of key Asian markets should help earnings in those economies, especially for companies where sales have been restrained by semiconductor shortages and for those that have been closed down for some time, notably in the travel and tourism sector.

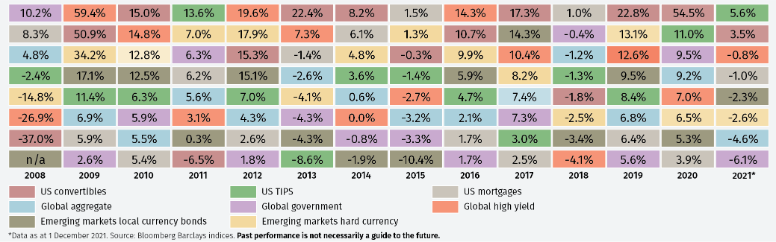

9. Fixed income opportunities remain

Upward pressures on government bond yields will depress total returns. Emerging market bonds are our choice in a tough environment.

Generally, the background for most major developed fixed income markets in 2022 will be a tough one. The starting level of yields is low in nominal terms and negative in real terms. That, of course, has been said about the year-ahead outlook for some time. This year, it does seem likely that continued upward pressure on inflation coupled with reasonably robust economic growth and the demands for clean energy infrastructure spending will push up benchmark government bond yields.

In this tricky environment, we see an interesting opportunity in emerging market bonds, both in hard currencies and local currencies. Local currency yields are high and in many markets, often pushed up by aggressive domestic monetary policy tightening. As the effect of this works through in dampening domestic inflationary pressures, we think attractive local currency returns can be made. There is the potential for this to be augmented by currency appreciation.

In China, high yield spreads are considerably above the corresponding level in the US market (see Figure 9b). This reflects concerns about the property sector, in particular. We think these have been exaggerated and consequently represent an opportunity.

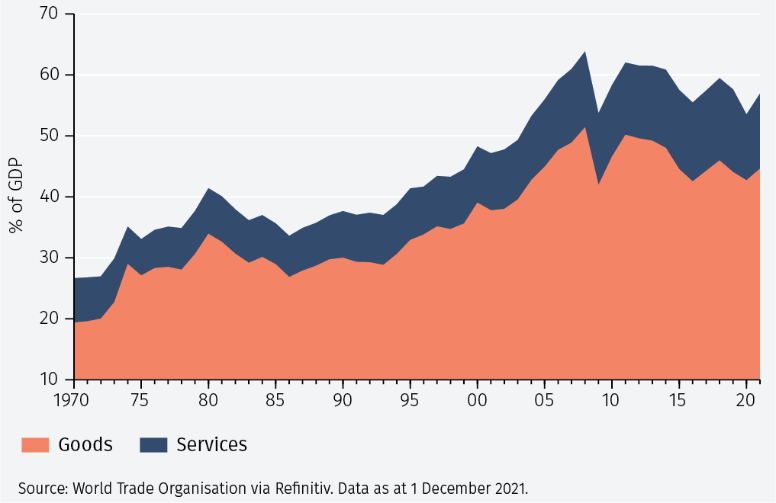

10. Globalisation, reshoring and new trade patterns

Globalisation will continue but various factors limit the scope for reshoring.

Patterns of global trade are changing and 2022 will be an important year. In particular, there are clear pressures for reshoring of production. The drive for that, in the US, under President Trump, was bringing back jobs lost to overseas producers. Under President Biden, the emphasis is on making supply chains – particularly in electronics and pharmaceuticals – more resilient. There is also an environmental aspect - domestic production may well have a lower carbon footprint than production overseas. And with freight costs remaining high and shipping schedules less certain, smooth global flows can no longer be relied on.

However, several factors limit the scope for such reshoring.

One key constraint is a lack of labour. From a longer-term perspective, US population growth is slowing, due to a lower birth rate and lower immigration. Shorter-term, labour force participation (those working or actively seeking work) has failed to recover to its pre-Covid level. The ‘Great Resignation’ (workers voluntarily quitting their jobs) has seen as many as 1.5 million of those aged 55+ bring forward their retirements; child-care responsibilities, long-term Covid-related sickness, work-related stress and concerns about the persistence of the virus have dissuaded others. 8

Another factor limiting the scope for reshoring is the complexity of global production. Covid vaccine production can require more than two hundred individual components, which are often manufactured in different countries.9 For many electronic items thousands of components are needed. We no longer live in a world where consumer electronics are invented in Californian garages.

One solution is automation and reconfiguration of manufacturing processes, incorporating artificial intelligence (AI) to make them as efficient and error-free as possible.

While this will help physical goods production, services trade is growing in importance. For some time, administrative functions for many companies have been carried out overseas: anything from technical support in the Philippines to software development in Uruguay and airline ticketing in India. Such services trade is probably under-recorded: according to one estimate, it could be twice that indicated by the data shown in Figure 10. 10

So, although the nature of globalisation is changing, the scope for reshoring is limited. We will continue to live in a globally interconnected world.

Footnotes

1 Savings above the average 2019 savings rate.

2 Source: Nomura; UNCTAD. 1 December 2021.

3 Source: Deloitte. https://tinyurl.com/32xcakbm. 1 December 2021.

4 The explanation given by Larry Summers, for example. See https://tinyurl.com/vx74z429

5 Source: Evercore ISI; 1 December 2021.

6 https://tinyurl.com/3hvpu4x4

7 Source: WoodMackenzie. https://tinyurl.com/yk3brkfh

8 Niall Ferguson, Bloomberg. https://tinyurl.com/29nn28jc

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.