- Date:

A Wave of Enthusiasm for GLP-1 Drugs

Over the past several months, investors have enthusiastically embraced the potential of new GLP-1 therapies, such as Novo-Nordisk’s Wegovy & Ozempic and Eli Lilly’s Mounjaro.

While these products are currently billed as best-in-class treatments for weight-loss and Type II diabetes, new clinical data has demonstrated their potential in preventing and/or treating many chronic conditions – such as sleep apnea, kidney disease, cardiovascular conditions, orthopedic pain, and addiction disorders.

The ongoing GLP-1 fervor has triggered unprecedented underperformance for the Medical Device sector, and by association, Biotechnology as well. The near-term concern is that patients could theoretically cancel an upcoming surgery or medication, and alternatively, treat their underlying condition with an injectable GLP-1 drug (e.g., maybe I can avoid knee surgery if I lose 50 pounds). Longer-term, investors are also fearful that the prevalence of many chronic conditions could decline with the launch of these “wonder drugs”.

Current research indicates that GLP-1 drugs have had no near-term impact on surgery volumes. Longer term, while we acknowledge the potential for slower growth in weight-related end markets, adoption rates of GLP-1 therapies would need to double current consensus expectations to trigger a material decline in these populations.

Signs of a Bubble

Over the past several months, investors have flocked to GLP-1 stocks at the expense of nearly every other sub-sector of healthcare. We believe expectations here are lofty, with names such as Eli Lilly having traded at 16x 2024 consensus sales and 49x 2024 consensus earnings.

While we understand that rampant GLP-1 adoption is a theoretical long-term threat (potential cure) for many chronic conditions – we believe the hypothesized impact to the healthcare industry is overblown. A couple of points to counter the current narrative:

1. Based on our industry work, reimbursement authorities cannot support overnight access to these costly drugs (at an estimated cost of $1,000 per patient per month). As such, near-term eligibility restrictions are likely to restrain the ramp in GLP-1 treatments.

2. Additionally, many Americans have a natural aversion to injectable medications. Because these self-administered medications involve long needles to the stomach, we believe adoption rates will be measured.

3. Most important, GLP-1 drugs trigger appetite suppression through mechanisms of nausea, vomiting, and diarrhea – long-term side effects that many would consider intolerable. With more than 50% of GLP-1 patients dropping off the drug within 12 months (and regaining weight), this represents a significant headwind for impacting long-term medical outcomes.

Impact on Performance

The Medical Device sector has been decimated by the current GLP-1 narrative – with the S&P Healthcare Equipment Index down more than 20% in 3Q23 and another 9% in the first half of October. Biotechnology stocks have experienced a similar impact – with the S&P Biotechnology Index off more than 12% in 3Q23 and another 4% in the first half of October.

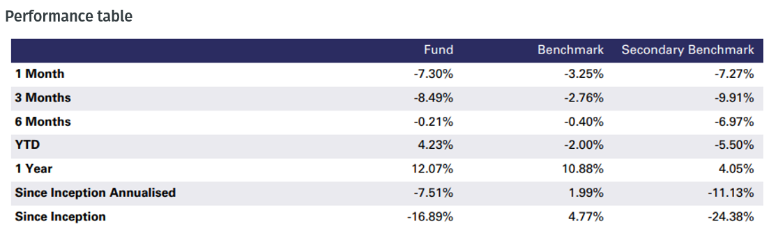

With more than two-thirds of the New Capital Healthcare Disruptors Fund allocated to Medical Devices and Biotechnology, the current environment has been challenging to say the least. Fund performance was down 8% in 3Q23 and another 5% in the first half of October. Full year performance is now flat YTD but outpacing the MSCI Healthcare Index by 250bps and our secondary benchmark (Solactive) by more than 850bps. The Secondary benchmark is designed to compare the performance of the fund with small and mid-cap companies, whereas the MSCI Health index tilts towards large-cap names.

Past performance is not necessarily a guide to the future. The value of your investments and the income from them may fall as well as rise as a result of market as well as currency fluctuations and you may not get back the full amount invested. Fund performance is net of fees and representative of the USD I Acc Share Class and shows a maximum of five previous calendar years and current year to date (computed on a NAV to NAV basis). Where share class inception begins prior to the five previous years the chart has been rebased to 100. Where the Fund has fewer than five full years of performance, returns are shown from the inception date. Benchmark: MSCI World Health Care Net Total Return USD Index, Secondary Benchmark: Solactive Developed Markets Healthcare Mid & Small Cap Index NTR. Source: EFG Asset Management, Bloomberg. As at 30 September 2023.

We believe the recent pullback is reminiscent of the bariatric surgery bubble of the early 2000s, as the procedure held the promise of 30% weight loss and a theoretical cure for Type II diabetes. And while the Medical Device and Biotechnology sector sold off in a similar fashion, many of these stocks experienced significant rallies as the procedure ultimately failed to quash the prevalence of weight-related disorders.

We Remain Constructive on Healthcare Disruptors

We believe the recent sell-off could represent an opportunity for us to establish or add to positions in the fund. Despite an attractive insular growth outlook, valuation multiples in both Medical Devices and Biotechnology have dropped more than one standard deviation below their long-term averages. For our fund specifically, the forward sales multiple has declined more than 38% since the start of the year.

While we have a few names that have been directly impacted by the recent GLP-1 fervor (e.g., Dexcom, Intuitive Surgical and Shockwave Medical), the bulk of our portfolio is focused on next-generation diagnostics and breakthrough treatments that are unaffected by the potential fluctuations of the “waistlines” in the developed world.

New Capital Healthcare Disruptors Fund

Learn moreMARKETING COMMUNICATION

For professional clients, qualified investors and accredited investors only. The value of investments and the income derived from them can fall as well as rise, your capital is at risk. Note: Past performance is not a guide to the future. Returns may increase or decrease as a result of currency fluctuations.

Performance contribution is gross of fees, all other performance shown is net of fees and expenses. Please refer to the Prospectus for further information on this Fund and prior to any subscription. All data sourced New Capital, EFGAM, Bloomberg, as at title date, unless otherwise stated.

Issued in the UK by EFG Asset Management (UK) Limited which is authorised and regulated by the Financial Conduct Authority (FCA Registration No. 536771). Registered No: 7389736. Registered address: Park House, 116 Park Street, London W1K 6AP. Telephone: +44 (0)20 7491 9111.

This document is a marketing communication and does not constitute an offer to sell, solicit or buy any investment product or service, and is not intended to be a final representation of the terms and conditions of any product or service. The investments mentioned in this document may not be suitable for all recipients and you should seek professional advice if you are in doubt. Clients should obtain legal/taxation advice suitable to their particular circumstances. This document may not be reproduced or disclosed (in whole or in part) to any other person without our prior written permission. Although information in this document has been obtained from sources believed to be reliable, EFGAM does not represent or warrant its accuracy, and such information may be incomplete or condensed. All estimates and opinions in this document constitute our judgment as of the date of the document and may be subject to change without notice.

EFGAM will not be responsible for the consequences of reliance upon any opinion or statement contained herein, and expressly disclaims any liability, including incidental or consequential damages, arising from any errors or omissions. Performance results shown are net of applicable fees and expenses.

Any information quoted relating to the New Capital UCITS Fund plc is merely a brief summary of key aspects of the Fund. More complete information on the fund can be found in the prospectus, the simplified prospectus or key investor information document, and the most recent audited annual report and the most recent semi-annual report.

These documents constitute the sole binding basis for the purchase of fund units. Copies of these documents are available free of charge in the United Kingdom at EFG Asset Management (UK) Limited ("EFGAM"), Park House, 116 Park Street, London W1 K 6AP, United Kingdom. Copies of these documents are available free of charge in Germany at the offices of the German information agent, HSBC Trinka us & Burkhardt AG, Konigsallee 21/23, 40212 Dusseldorf, Germany. Copies of these documents are available free of charge in France from the French centralizing agent, Societe Generale, 29, boulevard Haussmann - 75009 Paris, France. Copies of these documents are available free of charge from the Swiss Representative: CACEIS (Switzerland) SA, Route de Signy 35, CH-1260 Nyon, Switzerland. Paying Agent: EFG Bank SA. 24 Quai du Seujet, CH-1211, Geneva 2, Switzerland.

Copies of these documents are available free of charge in Luxembourg at the offices of the Luxembourg paying agent, HSBC Securities Services (Luxembourg) S.A., 16 boulevard d'Avranches, L-1160 Luxembourg, R.C.S. Luxembourg, B28531. Copies of these documents are available in the local languages as per the above and from www.newcapitalfunds.com. A summary of investor rights is available at: https://www.efgam.com/newcapitalfunds/Summary-Investor-Rights.html.

Country of origin of the collective investment scheme: Ireland

Investment products may be subject to investment risks, involving but not limited to, currency exchange and market risks, fluctuations in value, liquidity risk and, where applicable, possible loss of principal invested.

In the European Union, this Document is issued by KBA Investments Limited ("KBA"). KBA Investments Limited is licensed in terms of the Investment Services Act (Cap 370) as an Investment Firm and is regulated by the Malta Financial Services Authority (Authorisation ID KIL2-IF-16174). In the European Union, this Document is available to Professional Investors only (as defined under Annex II to Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU).

KBA Investments Limited Licensed in terms of the Investment Services Act ( Cap 370) as an Investment Firm and is regulated by the Malta Financial Services Authority (Authorisation ID KIL2-IF-16174). KBA Investments Limited is a sub-distributor in certain countries in the European Union for EFG Asset Management (UK) Limited. For the full list of EU countries, please visit the https://www.mfsa.mt/financial-services-register/. Registered Office: Trident Park, Notabile Gardens, No 2 - Level 3, Zone 2, Central Business District, Birkirkara, Malta. Registered in Malta No. C97015.