- Date:

- Author:

- GianLuigi Mandruzzato

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

The moderation in European electricity prices will spill over to Switzerland in 2025. As a result, Swiss inflation risks being lower than the SNB expects. In this Macro Flash Note, Senior Economist GianLuigi Mandruzzato looks at the implications for the Swiss National Bank (SNB) monetary policy and the Swiss franc.

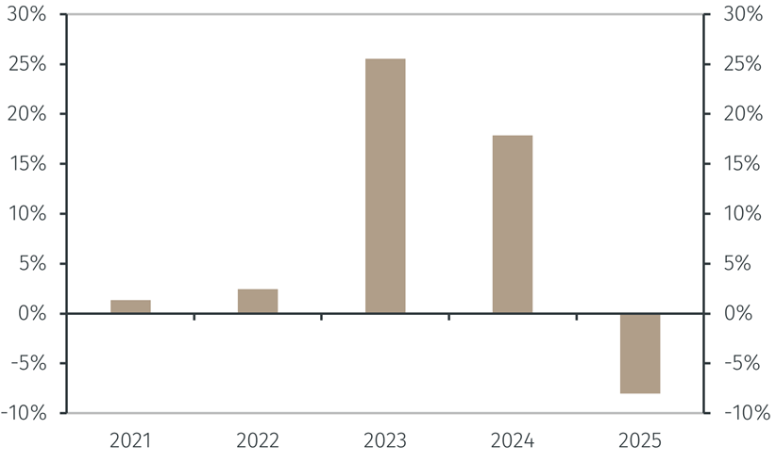

After the sharp increases of the past two years, electricity prices for Swiss households and businesses will fall in January 2025. On March 20, Swissgrid, the electricity grid operator, announced that next year the costs borne by an average household for general ancillary services, for power losses, and for energy reserves will fall by about 40% compared to 2024. This corresponds to a drop of around 4% in the overall price per kilowatt hour of electricity paid by Swiss households.

In July, more positive news on future electricity prices were released. According to a survey by the Association of Swiss Electricity Companies conducted among 83 of its members, the hourly price per kilowatt is seen falling by around 8%, which would reduce the overall price paid by households by another 4%.1

The price of electricity will likely fall significantly in 2025, although it will remain more than 35% higher than in 2022. The savings for the average Swiss household are estimated to be around CHF 110 for the full year, corresponding to a drop of around 8% from 2024.

Source: LSEG Data & Analytics and EFGAM calculations. Data as at 18 July 2024.

Lower electricity prices will lead to a further moderation in inflationary pressures in Switzerland. In early 2025, the annual CPI inflation rate will benefit from a favourable comparison with the 17.8% increase in the price of electricity recorded in 2024. Although electricity represents only 1.85% of the Swiss CPI basket, if its price falls as expected headline CPI inflation will decrease by half a percentage point next January compared to the rate in December and will most likely drop below 1% in annual terms.

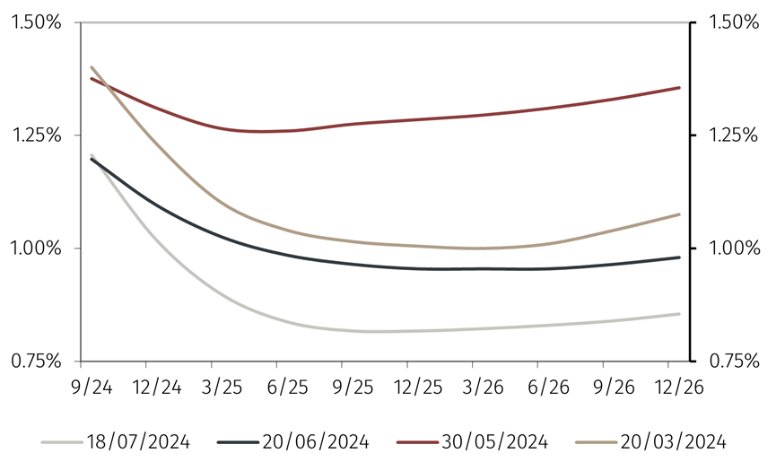

While large, the decline in headline inflation will represent a price level shock. As such, it should not have lasting effects on the underlying inflation dynamics. However, the decline in electricity prices will also dampen the dynamics of producer prices (PPI), where electricity accounts for about 2.5%, of the basket. This effect will be felt more gradually and will further reduce inflationary pressures in Switzerland through 2025 and beyond. This points to the risk that Swiss inflation will undershoot the latest SNB’s projections. Perhaps, this is one reason why the prices of futures contracts discount with a high probability that the SNB will cut the policy rate to 0.75% before the end of next year.

Source: LSEG Data & Analytics and EFGAM calculations. Data as at 18 July 2024.

Interestingly, the Swiss franc has recently strengthened despite the downshift in expectations of future SNB policy rates. This perhaps reflects the fact that lower inflation in tradeable goods prices, which can be proxied by the PPI, supports a nominal exchange rate appreciation in the longer-run. At the current exchange rates, the Swiss franc appears about 10% undervalued against an equal-weighted basket comprised of the US dollar and the euro based on the Purchase Power Parity. The prospect of lower PPI inflation than its trading partners will lend further support to the Swiss franc exchange rate.

1 Swiss electricity supplies must communicate final prices for 2025 to the Federal Electricity Commission (ElCom) by the end of August, and ElCom will publish the new prices for 2025 in early September.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.