- Date:

- Author:

- Joaquin Thul

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

Brazil has embarked on a series of policy changes, causing uncertainty to rise and equities to underperform in 2023. In this edition of Infocus Joaquin Thul looks at the recent Brazilian Central Bank’s (BCB) decisions, the factors that might drive a policy change later in the year and how Brazil’s foreign policy aims to lead global sustainability efforts and promote peace.

Since Lula Da Silva took office on 1 January, there has been a series of changes in Brazil’s economic and foreign policies. A left-wing government has been appointed following a divisive election in 2022. The new administration proposed a new fiscal rule, which is under review by the Brazilian Congress. The Ministry of Finance is working on a tax reform and aims to conduct an administrative reform. Concerns have been raised over the management of the fiscal budget by the new government which also questioned the independence of the BCB.

Additionally, Lula intends to re-position Brazil as a key player in the current geopolitical environment, signalling a change from the Bolsonaro administration. He aims to increase Brazil’s trade links with Asia and lead the BRICS group together with China, its main trading partner.1,2 The increased uncertainty over some of these proposed changes and the concerns arising from Brazil’s close ties with China help explain the poor performance of Brazilian equities in 2023 despite attractive valuations. The Bovespa index is down by almost 7% year-to-date (YTD) after being one of the best performers last year with gains of almost 5%.

Economic policy developments

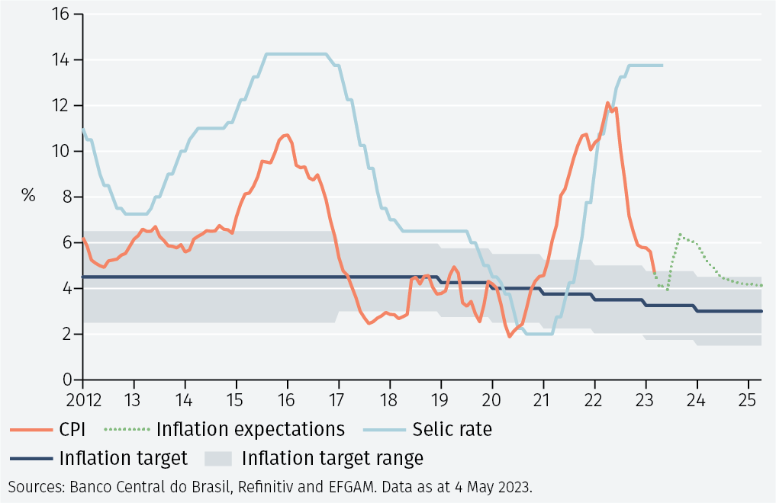

Despite initially questioning the BCB’s independence and need for lower interest rates, Lula has recently toned-down his criticism of BCB President Campos Neto.3 However, the appointment of Gabriel Galipolo, a senior official at the Ministry of Finance, as monetary policy director at the BCB has been seen as another attempt from the government to influence the central bank’s actions. On 3 May the BCB kept interest rates unchanged at 13.75% for the sixth consecutive meeting. The tightening of monetary policy since April 2021 saw the Selic rate increasing by 11.75 percentage points, and headline inflation declining from over 12% year-on-year in April 2022 to 4.65% in March 2023. There is speculation on when the BCB will start cutting rates to support the economy which, according to IMF projections, is expected to see its GDP grow by less than 1% in 2023. The decline in commodity prices, the deceleration of global economic activity and the contraction in domestic credit supply have lowered inflation and would support a rate cut in the coming months.

However, the BCB said that cutting interest rates will depend on inflation getting close to the 3.25% target and the anchoring of long-term inflation expectations. The first condition has already been met. Current headline inflation is now within the upper limit of the target range (see Figure 1). The second condition remains challenging. The de-anchoring of long-term inflation expectations is attributed to the risks of persistent global inflationary pressures and the uncertainty surrounding the new fiscal rule which will impact the trajectory of public debt and thus inflation expectations (green dotted line in Figure 1).

In March, Minister of Finance Fernando Haddad presented the new fiscal rule, and it is expected to be approved by Congress in mid-May. The new rule sets annual primary fiscal balance targets and limits real spending growth to 70% of real revenue growth. This limit could fall to 50% if the primary balance target is missed.4 Being now linked to revenue, as opposed to inflation under the previous rule, the new fiscal framework risks making public spending more pro-cyclical. However, the additional condition to meet the primary fiscal target is expected to limit the scope for the administration to be fiscally irresponsible.

Stepping up foreign policy efforts

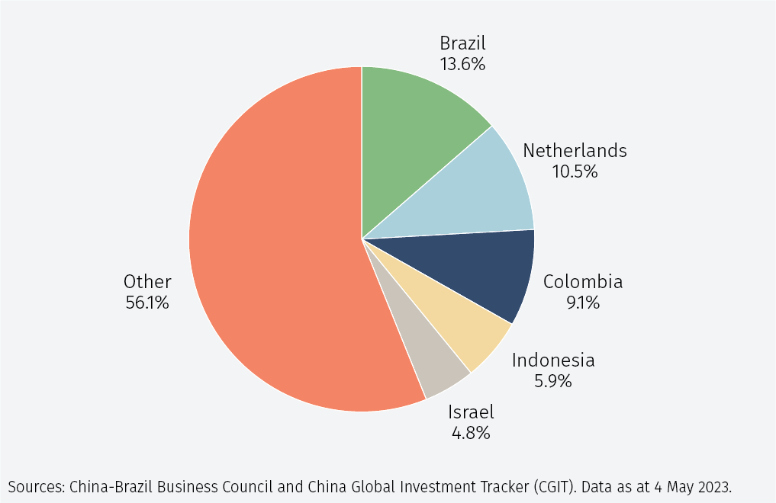

Lula has renovated Brazil’s foreign policy relations with key trading partners since January. In the first four months of 2023 he met US President Joe Biden to discuss common initiatives on climate change, visited China to work on trade and joint investment projects, travelled to Europe to restart discussions over a free-trade agreement between Mercosur and the European Union, and received Russia’s Foreign Minister Sergei Lavrov to discuss a potential resolution to the Russia-Ukraine conflict. Russia is Brazil’s main supplier of fertilizers, a key input for its agricultural industry. Lula’s visit to Xi Jinping in April was important to support investment and trade between the two countries. Brazil represented the main destination for Chinese investments in 2021, accounting for almost 14% of China’s investment abroad (see Figure 2). Moreover, Chinese investments in Brazil increased to USD 5.9 billion in 2021, the highest value since 2017, matching the amount invested by China in the rest of South America combined.5

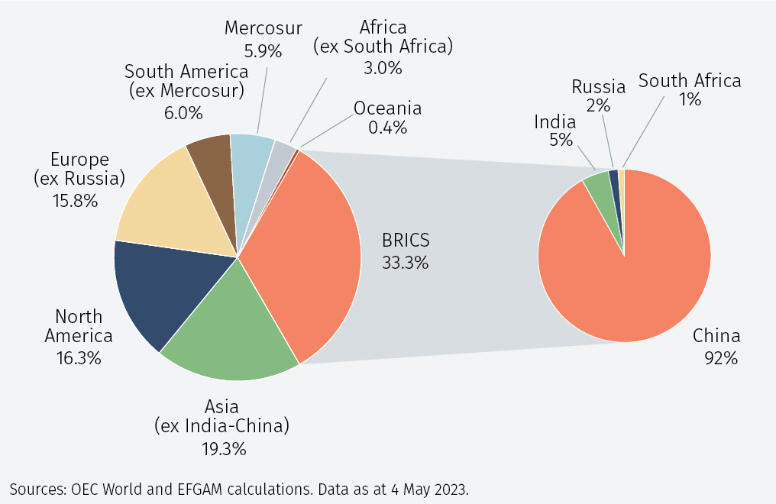

Investors were also concerned over two events during Lula’s visit to China. First, he attended the appointment of Brazilian former President Dilma Rousseff as head of the New Development Bank (NDB), formerly known as the BRICS Development Bank.6 During that event, Lula suggested that Brazil and China should stop using the US dollar for trade between them and called for the BRICS countries to find an alternative currency to be used for commerce among the group. Trade with the BRICS represents a third of Brazil’s exports, with China being the top destination (see Figure 3).

Additionally, Lula condemned the invasion of Ukrainian territory but was critical of Western countries’ response to the war. He stated that US and Europe should stop “encouraging” the conflict and start talking about peace. In line with Brazil’s historically neutral stance on previous global conflicts, Lula used the meeting with Xi to discuss the creation of a so-called “peace club” of countries to negotiate a solution to the conflict.

Conclusion

The change of government in Brazil has brought a series of changes in economic and foreign policies. The uncertainty this has generated has contributed to the poor performance of domestic equities in 2023. However, the direction of economic policy is unlikely to change under Lula and that will give investors more clarity in the coming months. The independence of the BCB will be respected given its recent success at reducing inflation. Long term inflation expectations have increased above the BCB target but should decline as uncertainty fades. It would be reasonable to expect the BCB to start cutting rates in the second half of 2023.

On the foreign policy front, Brazil’s ties with China have increased in the last few years, with a surge in Chinese investment in Brazil, particularly in the oil and gas exploration sector, but also in green infrastructure projects. Conversely, China is Brazil’s top trading partner, with agricultural exports to China representing almost one third of total exports.

Brazil seeks to position itself as a key player in the current geopolitical map. Efforts to negotiate a peaceful solution to the Russia-Ukraine conflict are commendable, although unlikely to succeed in the short term. Finally, it would be reasonable to expect joint efforts with China to increase trade within the BRICS in other currencies than the US dollar. However, this is also likely to take time given the strong position of the US dollar as global reserve currency.

1 BRICS is the group of Brazil, Russia, India, China and South Africa.

2 China accounts for one-third of Brazil’s total exports.

3 The BCB was granted independence by Congress in 2021.

4 Official projections anticipate a primary balance deficit of 0.5% of GDP for 2023, 0% in 2024 and a fiscal surplus of 0.5% and 1.0% of GDP in 2025 and 2026, respectively.

5 Chinese Investment in Brazil. 2021 a year of recovery. 31 August 2022 https://www.cebc.org.br/2022/08/31/estudo-inedito-investimentos-chineses-no-brasil-2021/

6 A supranational institution with headquarters in Shanghai, founded in 2015 to support infrastructure and sustainable development projects in emerging economies.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.