- Date:

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

The ECB is expected to raise interest rates by 75bps when it meets this week, which would be the largest hike ever implemented. In this edition of Infocus, GianLuigi Mandruzzato looks at the risk of excessive monetary tightening by the bank.

In her speech at the Jackson Hole symposium, Isabel Schnabel, an influential member of the ECB’s Executive Board, stated the need to raise interest rates quickly even in the face of the looming recession. Three factors support this strategy:

1. Uncertainty about the persistence of inflation;

2. threats to central bank credibility;

3. potential costs of acting too late.

Schnabel concluded that because “high inflation has become the dominant concern of citizens […] central banks need to act forcefully [and] lean with determination against the risk of people starting to doubt the long-term stability of our […] currencies.”

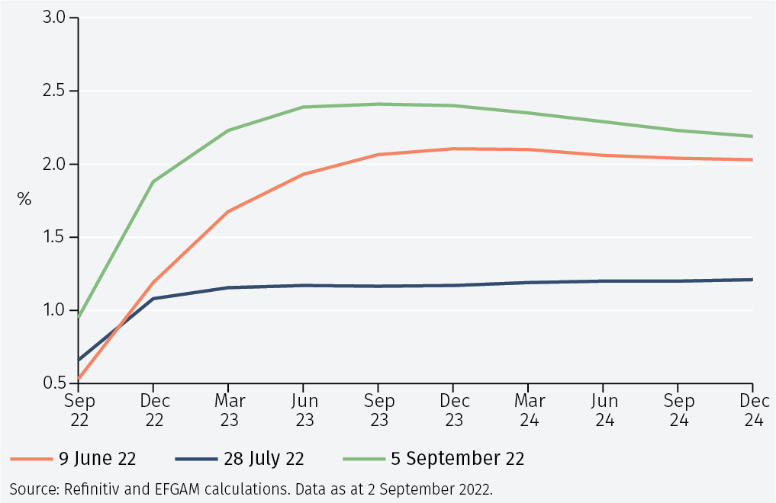

Markets raised the probability of a 0.75% interest rate increase at the 8 September ECB meeting to over 60%. Rates are expected to peak at 2.5%, about 1.25 percentage points higher than in July (see Figure 1) and the interest rate expected at the end of 2024 rose to 2% from 1.25% a month ago.

Schnabel’s remarks suggest the eurozone inflation outlook has worsened considerably of late. However, the data are less clear cut with several elements improving recently.

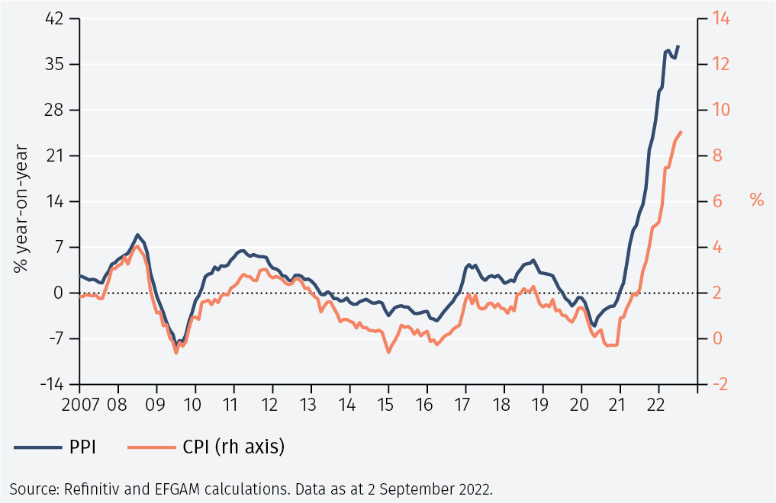

The main negative factor for eurozone inflation is the increase in natural gas prices and, because of that, electricity prices as a result of the war in Ukraine and sanctions imposed on Russia. Producer price inflation surged to 38% year-on-year in July and will rise further in August when the natural gas price set a new record. Inevitably, high producer prices fed into CPI inflation (see Figure 2).

Increases in energy and food prices over the past year have pushed CPI inflation to 9.1% year-on-year in August, contributing 4.8 percentage points to overall inflation. Core inflation was 4.3% year-on-year, far above the ECB’s 2% target, reflecting shocks that have little to do with eurozone demand. Beyond energy prices, these include high freight rates and reduced availability of durable goods due to a shortage of semiconductors.

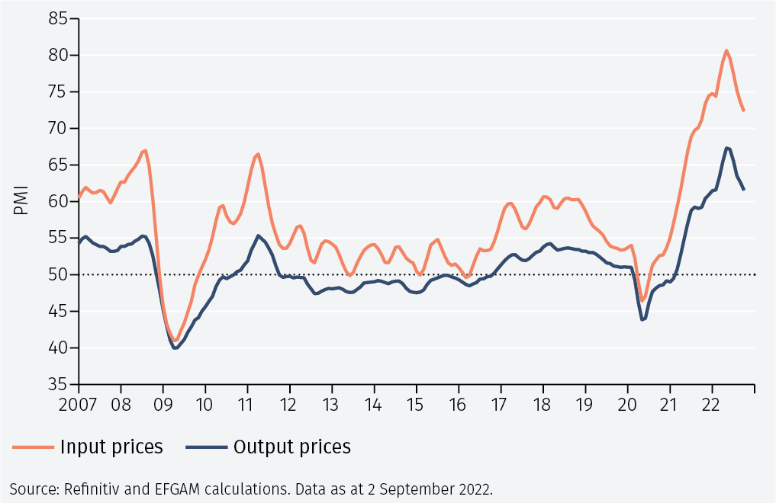

However, according to the PMI survey, price pressures are moderating (see Figure 3). In August, prices paid by eurozone firms for production inputs and prices charged to customers fell for a fifth and fourth consecutive month, respectively.

European households also do not seem worried about inflation. According to the EU Commission survey, households’ inflation expectations for the next twelve months are consistent with core inflation below 2% year-on-year (see Figure 4). This is significant as expectations moderated while inflation rose sharply, a development that brings to mind 2001 and 2008 when households correctly anticipated a quick fall in core inflation.

The decline in households’ expectations suggests that high inflation is seen as transitory. While it is unsurprising for workers to ask for compensation for the past inflationary shock, overall wage awards should remain close to the 3% year-onyear increase that, according to ECB estimates, is consistent with the 2% inflation objective (see Figure 5). The ECB will closely monitor ongoing wage negotiations, but the available evidence does not seem to require an aggressive reaction for the time being.

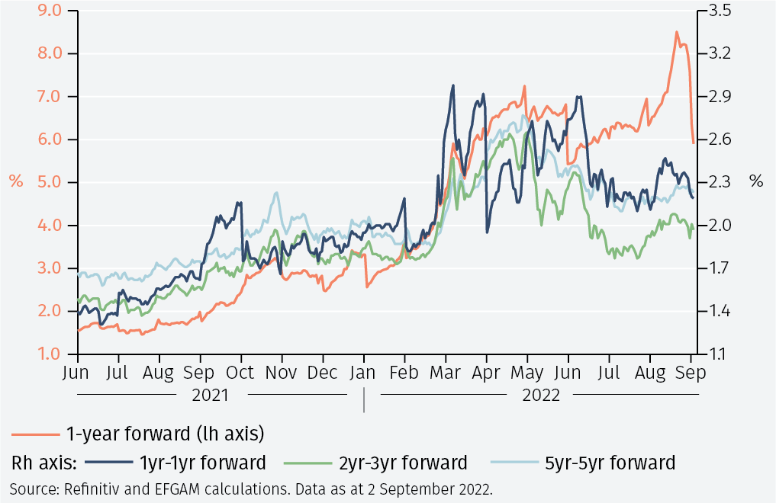

Furthermore, financial markets anticipate that inflation will return below the 2% objective (see Figure 6). The inflation swap rate for the three-year period starting in two years, when the ECB expected tightening will have taken full effect, is under 2%. Subtracting the risk premium, expected inflation is less than 2%. While this may show confidence in the ECB, it may also reflect concerns about an overly aggressive policy tightening.

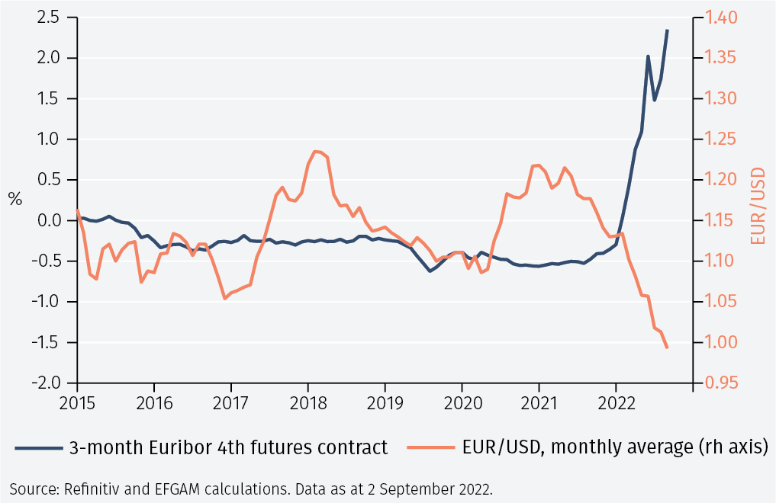

Finally, Schnabel anticipates that raising rates “forcefully” will stabilise the currency. Markets are not convinced and pushed the euro below parity against the US dollar despite increased rate expectations over the next twelve months (see Figure 7). Perhaps, markets are worried that aggressive policy tightening will undermine public debt sustainability in some eurozone countries.

In conclusion, the ECB is determined to raise rates aggressively, perhaps by 0.75% at the 8 September meeting. However, this new interventionist approach focuses more on current inflation than the medium-term outlook.

Despite record inflation in August, households and financial markets expect inflation will soon return to the ECB’s 2% objective. That and the looming recession reduce the risk that upcoming wage negotiations trigger a wage-price spiral.

Finally, the euro’s weakness – despite expected interest rate increases – likely reflects concerns about eurozone financial stability. A similar dynamic unfolded in 2011 following the surprising and premature ECB tightening, and the economy suffered the consequences of that decision for years. The ECB’s credibility would be better off with a gradual and forwardlooking approach to monetary policy normalisation rather than a frantic overreaction to exogenous shocks beyond its control.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.