- Date:

Infocus - Although inflation is reaching levels not seen for many years, central banks in most advanced economies hesitate to raise interest rates.

The National Bank of Poland responded quickly to the Covid pandemic with interest rate cuts and ample liquidity provision to the banking sector. With inflation picking up rapidly and strong economic growth, it is now in tightening mode. In this issue of Infocus, EFG chief economist Stefan Gerlach looks at Polish monetary policy.

The National Bank of Poland (Narodowy Bank Polski, NBP) is one of the few central banks that has already started tightening monetary policy and is doing so rapidly. Since October, the NBP has raised interest rates four times by a cumulative 2.15% to 2.25%. Further increases in the near term appear likely.

These developments raise the issue of how monetary policy is conducted in Poland and how it may evolve in the coming months. In this context, it is useful to look at the NBP’s policy framework and review recent policy developments during the Covid pandemic and the start of the NBP’s tightening cycle.

The monetary policy set-up in Poland

The main objective of the NBP is to maintain price stability and, since 1999, inflation targeting has been used. From 2004, when Poland joined the European Union, the target has been for 2.5% annual inflation with a tolerance band of +/- 1 percentage point.

Policy is set by the Monetary Policy Council and the principal policy instrument, as in many countries with inflation targeting, is a short-term interest rate: the minimum yield on seven-day NBP money market bills.

A corridor system is used to control money market interest rates more closely. The ceiling is given by the Lombard rate and the floor is given by the NBP deposit rate. Thus, if money market rates rise sharply, banks can borrow from the NBP using government securities as collateral. And if money market rates fall too low, they can deposit funds overnight with the NBP. The NBP uses required reserve ratios to smooth the impact of fluctuations in banking sector liquidity on interbank interest rates.

While Poland is a member of the European Union and has undertaken to join the eurozone at some future date, the zloty exchange rate has been freely floating without restrictions since 2000, although the NBP may decide to intervene if necessary to achieve the inflation target.

However, when Poland decides to join the euro, it will have to maintain a stable zloty against the euro for at least two years according to the rules of ERM II. The NBP’s monetary policy will change fundamentally at that stage from targeting inflation to keeping the exchange rate broadly stable against

the euro.

Macroeconomic performance before Covid

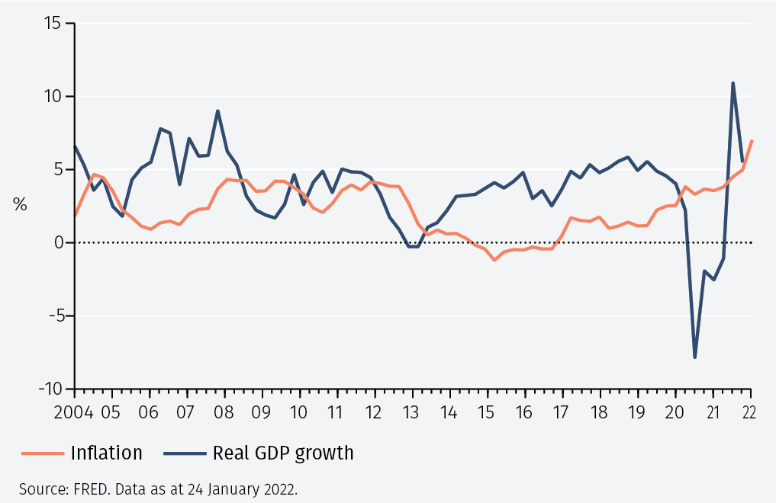

Poland’s macroeconomic performance in the 2004-2019 period was good, with real GDP growth averaging 4.1% and inflation averaging 2.1%. Of course, the high growth rate has much to do with Poland’s economic transition from socialism to a market economy that started following the appointment of Prime Minister Mazowiecki in 1989. With low wages, greater integration in the international trading system and accession to the EU in 2004, growth has been strong, not least due to sizeable fiscal transfers received from the EU.

Looking more closely at the economic conditions since 2004, it is notable that Poland was not severely affected by the Global Financial Crisis in 2008-9. However, real growth fell during the eurozone debt crisis in 2011 and real GDP growth over 4 quarters contracted from Q4 2012 - Q1 2013. Inflation fell sharply over this period and Poland experienced a two-year period of deflation starting in late 2014.

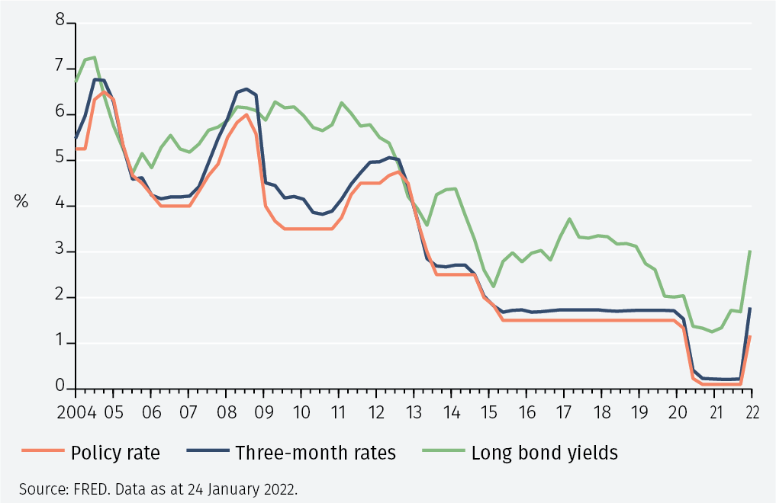

Throughout this period, interest rates in Poland fell gradually. The steady decline of interest rates in the eurozone surely played a role. But Poland had also experienced exceptionally high inflation in the 1990s, and inflation expectations appear to have declined only gradually as the NBP’s credibility grew (see Figure 1). Over time, policy rates fell from 5.25% in early 2004 to 0.10% during Covid (see Figure 2).

NBP policy during the Covid pandemic

The NBP responded quickly at the start of the Covid pandemic. In three meetings in March, April and May 2020, the Monetary Policy Council cut the policy rate by 140 bps to 10 bps and instituted an asset purchase programme (APP) and a programme allowing banks to fund new loans to enterprises.

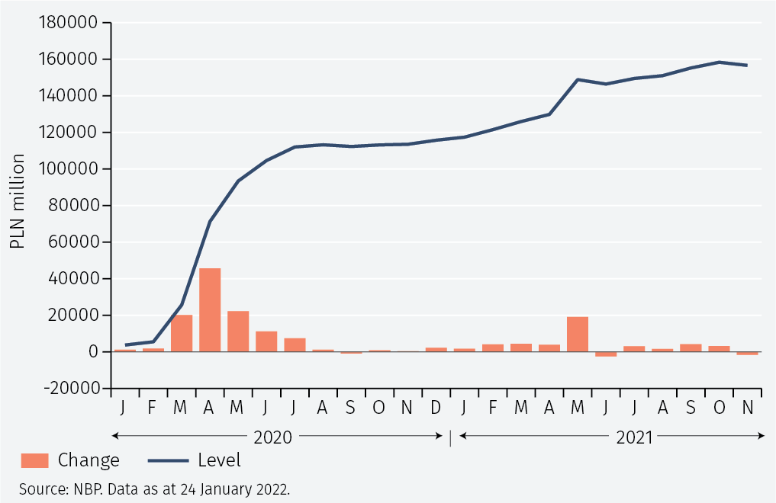

The APP was introduced during the severe market tensions in Spring, when Poland experienced rising bond yields and large and unexpected outflows from foreign investors.1 Purchases were substantial and initially covered Treasury securities but subsequently focused on government-guaranteed bonds issued by the Polish Development Fund and the development bank BGK. As evidenced by the evolution of the NBP’s balance sheet, purchases peaked in the second quarter of 2020 and subsequently slowed significantly (see Figure 3). Overall, the presence of the NBP in the bond market had a calming effect with long bond yields declining despite the surge in crisis-related government borrowing. Purchases picked up temporarily in May 2021.

In the 14 policy meetings following the interest rate cuts in 2020, the NBP kept interest rate unchanged at 0.10% and kept the various liquidity providing programs on the books even though they had ceased to be of critical importance. (Appendix 1 summarises the NBP’s policy meetings that led to interest rate changes from 2020-22.)

A turn to tighter monetary policy

In response to economic activity recovering, labour markets strengthening and with inflation at 5.8% year-on-year, in October 2021 the NBP decided to raise interest rates by 40 bps to 0.50%. Further increases in inflation and stronger economic activity led to additional interest rate increases in November, December and January 2022, when rates reached 2.25%. After the last monetary policy meeting, the NBP signalled that further rate increases will likely be necessary to meet the inflation target.

This raises the question of what the neutral level of the real interest rate is in Poland, that is, when inflation is at the 2.5% target and the business cycle is “in neutral”.

One way to estimate this quantity is to look at the average real interest over some period. For instance, between 2005 and 2019, it averaged 1.3%. However, the average inflation rate was 1.9% in that period, that is, below the inflation target. This suggests that interest rates were too high for inflation to rise to the target, implying that the neutral real interest rate is somewhere below 1.3%.

Appendix 2 discusses another method to assess the neutral real interest rate which suggests an estimate of 1.1%. If so, in the longer run as inflation returns and stabilises at the 2.5% target, the policy rate can be expected settle around 3.6%, that is, at least 125 bps above the current level. That suggests that the NBP will engage in several more interest rate increases.

With inflation around 8% in December, the question arises whether rates will rise gradually towards the estimated steady-state level or if they will rise temporarily above that level. That depends on why inflation has risen so sharply.

One view is that inflation has risen solely because of higher energy prices and temporary cost increases related to bottlenecks. Under this view, inflation will return to its steady state level on its own, with no need for the NBP to tighten monetary policy. Thus, interest rates can be expected to gradually approach the 3.6% level.

Another view is that inflation has risen also because of domestic wage and price pressures. In this case, the inflation rate will not return to its steady state level unless these pressures are reversed. This calls for a temporary period of restrictive monetary policy. Thus, in this case interest rates are likely to be raised over the steady state level of 3.6% for some period before being reduced to that level.

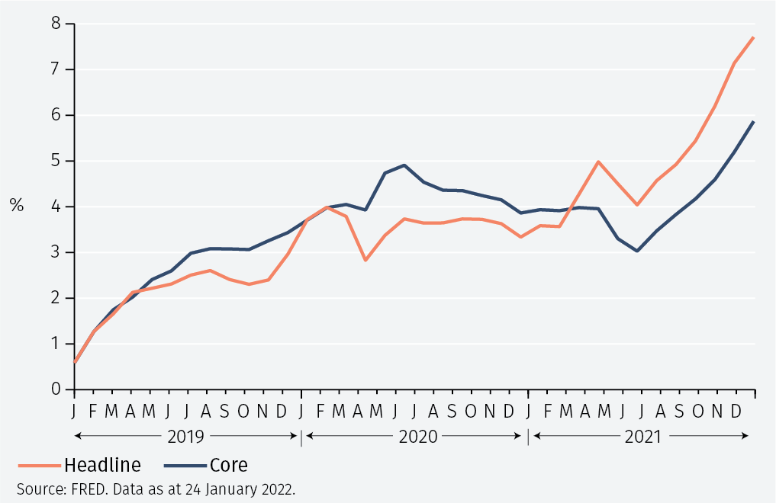

Figure 4 below shows headline and core (ex-energy) HICP inflation for Poland. Both measures were weak in early 2019 but have since risen gradually and in December 2021 were far above the 2.5% target. This indicates that the high inflation rate in Poland does not only reflect sharp increases in energy prices but also the economic recovery. This argument suggests that the NBP will increase interest rates above its steady level of 3.6% for a period of time to bring inflation down to target.

Conclusions

Monetary policy in Poland has been conducted successfully with a standard inflation targeting framework for almost twenty years ago. This has led to an average inflation rate since 2005 of 2.2%, which is close to the 2.5% target and well within the permissible fluctuation band 1.5 – 3.5%.

However, in early 2020 inflation rose just above the 3.5% upper limit of the fluctuation band, and in March 2021 it started to rise continuously, reaching 7.7% in December 2021. In response, the NBP started to raise interest rate from 0.1% in October to 2.25% in early January 2022.

It is difficult to know for sure at what level interest rates will stabilise. One estimate of the neutral real interest rate is 1.1%, suggesting that with a 2.5% inflation target interest rates will reach a long run level of around 3.6%. This suggests that recent interest rate increases will continue. Given that both headline and core inflation are far above the 2.5% target it seems likely that interest rates will first be pushed up above that long run level and that they will be reduced subsequently as inflation falls back toward the target.

1 See the IMF’s 2020 article 4 consultation with Poland for a discussion: https://tinyurl.com/53y7xbuz

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.