- Date:

Infocus - EFG Chief Economist Stefan Gerlach looks at the slowdown in the decline in the US unemployment rate and considers the difficulties facing the Fed which, by law, has to manage both employment and inflation.

In this issue of Infocus, EFG Chief Economist Stefan Gerlach looks at the slowdown in the decline in the US unemployment rate and considers the difficulties facing the Fed which, by law, has to manage both employment and inflation.

Tension has developed between observers of US monetary policy and the Fed. While market participants and the public have worried about the recent rapid rise of inflation, Chairman Powell has repeatedly emphasised that the US remains some distance away from maximum employment and that it is premature to discuss reducing the degree of monetary accommodation.

The state of the labour market matters much more for the Fed than other central banks because by law the Fed has dual objectives of price stability and maximum employment. While the latter term has not been defined, Chairman Powell has mentioned that the low unemployment rates of less than 4% observed before the Covid pandemic arguably constituted maximum employment. If so, with the unemployment rate more than 2% above that level, it appears that the US economy has still quite some way to run before maximum employment is reached.

While some commentators have been impatient for a sign that the Fed will soon start the long process of scaling back monetary policy, the Fed appears to believe that it is too early to do so.

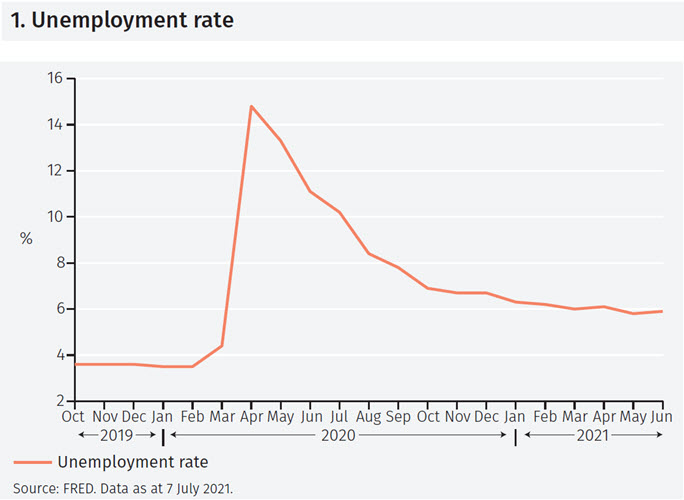

Figure 1 shows the evolution of the US unemployment rate since late 2019. The unemployment rate was 3.5% in February 2020 but started to rise precipitously in March as the pandemic took hold. It peaked at 14.8% in April, but then started to decline rapidly, falling by almost 8% to reach 6.9% in October. Since then, the rate of decline has slowed dramatically, and it took until May 2021 for the unemployment rate to fall below 6%. It was 5.9% in June.

With the Fed concerned about ensuring maximum employment, the failure of unemployment to fall further will have direct implications for US monetary policy.

Why has the unemployment rate stopped declining?

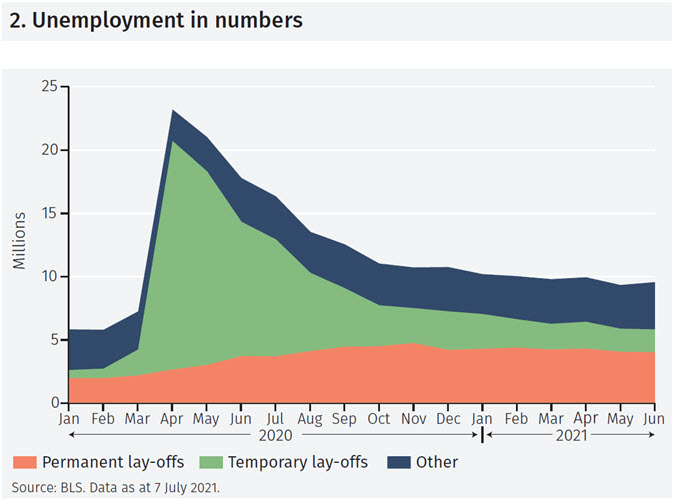

But why has the improvement in the labour market slowed so drastically? Figure 2 provides one explanation. After the pandemic started, the fraction of unemployed workers that were temporarily laid off rose rapidly from 13% to 78%. These workers remained in contact with their former employers with the understanding that they would be asked to return to their jobs as soon as the economy reopened.

As the economic recovery set in, these workers quickly returned to their jobs and the unemployment rate collapsed. By November, the proportion of workers on temporary layoff fell below 30% and started to decline slowly, falling below 20% only by May 2021.

With the group of temporarily laid-off workers contracting, the group of “other” workers – comprising new entrants to the labour market such as students, re-entrants such as those that gave up looking for a job when the pandemic started, and job leavers/quitters – grew in importance.

To continue reading, please use the button below to download the full article.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.