- Date:

Inview April 2021

Editorial

Welcome to the April edition of Inview: Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

Market concerns about inflation are growing. The drivers are the massive stimulus programme launched by the Biden administration coupled with expectations that the availability of more covid vaccines will allow for a quick normalisation of the economy.

The resultant shifts in US growth projections are striking. While forecasts made in the final quarter of 2020 were for growth of between 3-4% in 2021, the OECD, the IMF and the median FOMC member now expect US growth of around 6.5% in 2021. Growth forecasts for 2022 have also been raised, as have forecasts for growth of the world economy in 2021-22.

Unsurprisingly, expectations of stronger growth have been associated with sharp increases in oil and other commodity prices and upward revisions in inflation projections. Consequently, long bond yields and measures of breakeven inflation have risen. The depreciation of emerging market currencies against the US dollar is an additional driver of inflation in those economies. In the cases of Brazil, Russia and Turkey, the central banks have already started to raise interest rates to contain inflationary pressures.

Despite this sea change in sentiment and shifts in the outlook for inflation, the Federal Reserve continues to signal that interest rate increases are unlikely before 2024, implying that the tapering of bond purchases may not start before 2023. One reason for this seeming indifference to inflation risks is the change in the Federal Reserve’s policy framework announced last year.

The key feature of the new framework is the Federal Reserve’s intention to anchor inflation expectations at its 2% target by running an average inflation rate of 2%. Since inflation has averaged below 2% since the 2008 Global Financial Crisis, the price level is now some 8% below what it would have been if the target had been reached. In theory, this will allow the Federal Reserve to run inflation significantly above 2% for some years. In contrast to market participants, the Federal Reserve is unconcerned by the prospects for higher inflation.

Monetary policy accommodation will compound with fiscal expansion and faster vaccination in supporting the global recovery. However, differences in available fiscal space and speed of vaccine rollout mean the recovery will remain uneven across economies, with those most reliant on tourism most at risk.

The allocation of a diversified portfolio should maintain a slight overweight in equities, in our view. As we enter the Q1 earnings season we favour a tilt back to growth stocks as expectations are quite low relative to higher expectations for value stocks. However, longer term a more balanced profile is preferred given the expected strength of the economy over the course of the year. Exposure to the UK market looks attractive now that vaccinations are well advanced. Among fixed income assets, we believe convertible bonds offer the best risk/reward profile while tight spreads call for a neutral stance on corporate bonds despite the improved business cycle.

Global Asset Allocation: Summary

Equities

- We remain confident of the short-term prospects for US equities, preferring growth to value as we enter the first quarter earnings season.

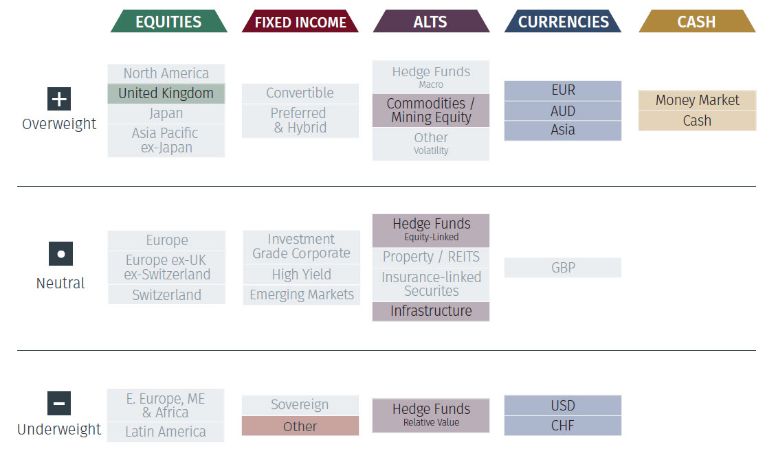

- We are upgrading UK equities from Neutral to Overweight on a tactical basis. This comes as a result of a pullback in sterling, the potential reopening trade resulting from a rapid roll out of Covid-19 vaccinations in the country and the expectation of an economic recovery in the second part of the year.

- We continue to favour Asia Pacific equities on a tactical and strategic basis. China has made a swift economic recovery but it should also be noted that Indian growth expectations are also robust and upwardly revised.

- The health crisis is far from being under control in most Latin American countries, limiting the economic rebound this year. Equity markets have already reflected some of the risks ahead and we are cautious on the region.

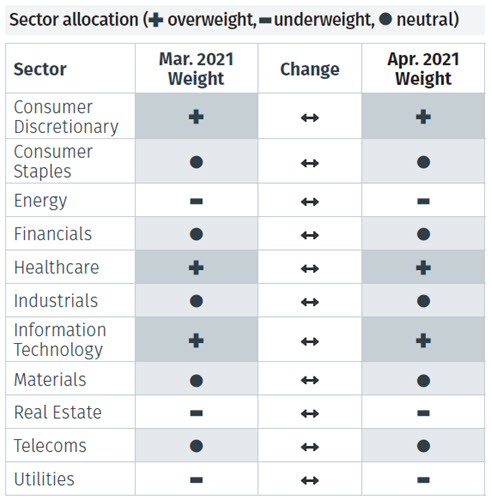

- Our Trend and Momentum model signals Consumer Staples is showing an uptrend again, having been downgraded to neutral the previous month. Meanwhile the Energy sector is signalling relative momentum over the last month. No sector changes have been made.

Fixed Income

- High yield spreads are at record lows but at the same time the economy is picking up. The higher coupons justify a continued neutral rating in this environment. Over the next few months good alpha opportunities may arise and so selectivity is key.

- Investment grade bonds have seen spreads narrow meaningfully over recent months helped by central bank support. We retain a neutral weight following last month’s downgrade.

- EM debt looks attractive in both hard and local currency given relatively high coupons although selectivity is required due to varying balances between macro conditions, covid and spreads.

- Preferred and convertible bonds are our tactical overweight positions due to their cyclical sensitivity.

Alternative Investments

- Following last month’s tactical upgrade of infrastructure to neutral no changes were made to our alternatives positioning.

- Within hedge funds we are more positive on Macro strategies that should offer a good hedge to risk-on positions, while we are more cautious in the relative value space as risk remains elevated.

Currencies

- The US dollar has strengthened in line with higher rates at the long end of the US dollar curve. The trend has now turned more neutral and we wait for a pullback in dollar-euro rates before reassessing.

- Besides the US dollar our other tactical currency underweight is the Swiss franc which we are watching to see if it will weaken further as volatility abates.

- Last month we downgraded the UK pound to tactically neutral as we felt the short-term benefits around the economic recovery had been priced in. We will continue to monitor the data as lockdown restrictions ease.

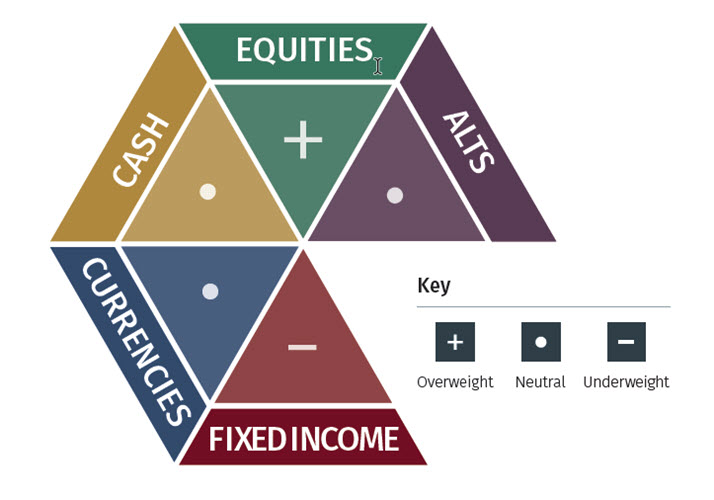

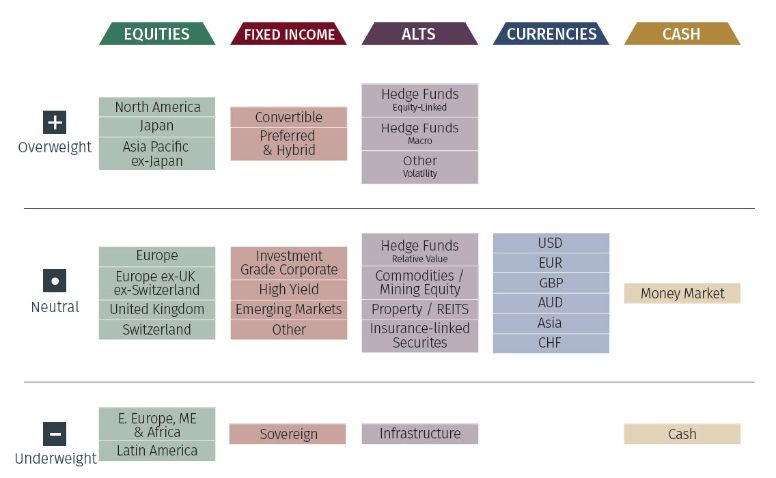

Global Asset Allocation: 12-Month Strategic Outlook

Based on a balanced mandate, the matrix below shows our long-term house view on investment strategy.

Overall Asset Allocation Views

Asset Class Breadown

Global Asset Allocation: 3-Month Tactical Outlook

Based on a balanced mandate, the matrix below shows our short-term house view on investment strategy.

Note: The highlighted boxes indicate a difference from our 12-month strategic outlook.

Asset Class Breakdown

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.

ASSET ALLOCATION GRIDS

Please use the button below to download the full article to see asset allocation grids.