- Date:

Inview February 2021

Editorial

Welcome to the February edition of Inview: Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

The world economy is recovering from the pandemic but at variable speeds around the world dependent on the stringency of containment measures and vaccination programme progress. While most forecasters expect 2021 to be a year of economic recovery, recent news of more contagious variants of the virus, which show higher mortality and may require new vaccines, has raised downside risks. So has the slow progress made in vaccinating populations in many countries.

The IMF shares the view that growth will recover in 2021. In its January update to its growth projections, it forecast world GDP will grow by 5.5% in 2021 and by 4.2% in 2022, a slight upward adjustment from last October’s projections. These revisions mask large differences among countries, with the forecasts for the US and India being raised sharply in 2021 (but trimmed in 2022) while the growth forecasts for Italy, the UK, Spain and France were marked down in 2021 (but up in 2022).

Global markets started the year on solid footing, despite some volatility in the last trading sessions of January amidst social media driven short squeezes of some hedge funds. Equity prices are underpinned by the strong start to the fourth quarter reporting season: an above average share of companies beat analysts’ estimates and they did so by a larger margin than the historical norm. Although repeating the performance of 2020 will be difficult, in our view the chances are that the long equity market rally will continue.

In addition, markets seem to have appreciated the growing evidence that central banks are taking action in the climate change area. The ECB recently announced the establishment of a climate change centre to coordinate its activities in this area, and the Federal Reserve is establishing a Supervision Climate Committee with the same objective. With the major central banks moving ahead, many smaller central banks will undoubtedly follow.

Central banks recognise that they are not responsible for climate issues and lack policy tools, but increasingly feel that they can’t disregard public concerns. They can take action in several ways.

As regulators and supervisors, they can require firms to provide more and better information on their climate exposures, and they can require banks to climate stress test their portfolios. And as standard setters, they can promote rules for what constitutes green assets, and for how risks should be assessed and managed. The net effect of this will be to spur growth of green finance, offer new opportunities for investors, and more and cheaper funding for the transition to a low carbon economy.

In this context, the asset allocation of a diversified portfolio should in our view continue to prefer a slight overweight to equity markets over fixed income assets, with the US, Japan and emerging Asia offering the best opportunities in our view at the current juncture. Among fixed income assets,convertible bonds remain attractive as do hybrid and subordinated bonds. Finally, while the short-term outlook for gold has become more uncertain, the longer-term prospects remain attractive on account of persistent fiscal and monetary policy accommodation.

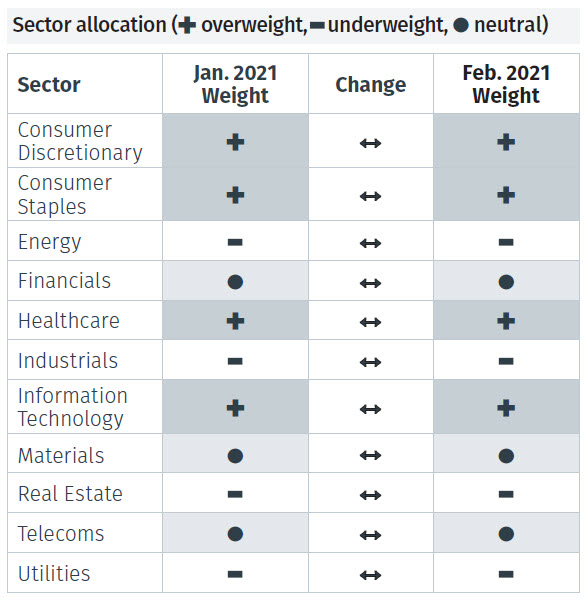

Global Asset Allocation: Summary

Equities

- January saw a very strong bounce for small-caps reflecting hopes of fresh fiscal stimulus from the Biden administration to help the economic recovery. We continue to have a preference for US small-caps as well as growth stocks and will monitor the rate at which US cities start to lift lockdowns.

- For European equities January started strong but momentum faded into the end of the month as lockdowns were re-enforced, something that will impact first quarter GDP. However, for now equity markets are looking through this soft-patch and so we hold a neutral position.

- We have been debating whether to change our UK equity positioning, with growing confidence around the vaccine roll out, but for now we hold a neutral position.

- The Asia Pacific ex-Japan region is still favoured tactically and strategically. We note that the recent India budget was a positive surprise and has spurred a decent reaction in the stocks.

- With no changes to trend and momentum signals, all sectors continue to show an uptrend. The challenge is to find sectors showing relative momentum at attractive valuations.

Fixed Income

- We remain neutral on emerging market debt however we are more optimistic on Asia while Latin American debt continues to look expensive in our view.

- Government bond yields have moved slightly higher over the months although they have still not moved high enough to warrant a re-evaluation of our underweight positioning.

- High yield corporate bonds have been helped by equity gains and the prospect of faster than expected economic growth but we hold a neutral positioning while spreads are still tight.

Alternative Investments

- For commodities as a whole we are strategically neutral but we differentiate our exposure. Industrial metals are preferred, particularly copper on a longer-term perspective. We are neutral on gold but poised to add to exposure should momentum improve. There is still caution around energy investments, with oil supply still too high.

- Infrastructure continues to be one of the areas within alternatives we are most cautious on, holding an underweight position until economic recovery picks up whereby it could prove an interesting alternative to fixed income plays.

Currencies

- Our one allocation change this month was a tactical upgrade of the pound to an overweight position. The pound has rallied as the Brexit dust settles and there is restored confidence of an economic recovery given the vaccine roll out.

- The renminbi is one of our favourite currencies, given the improving Chinese economy, a high carry on local rates and the likelihood that China will be the first to tighten policy. We are positive on Asian currencies as whole on a short term basis.

- Trader commitments show the market remains short in the US dollar and long in euros, consistent with the consensus view on dollar weakness during the second half of 2020. Dollar weakness could persist so we remain cautious.

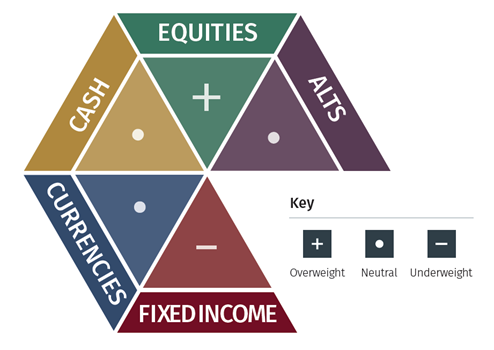

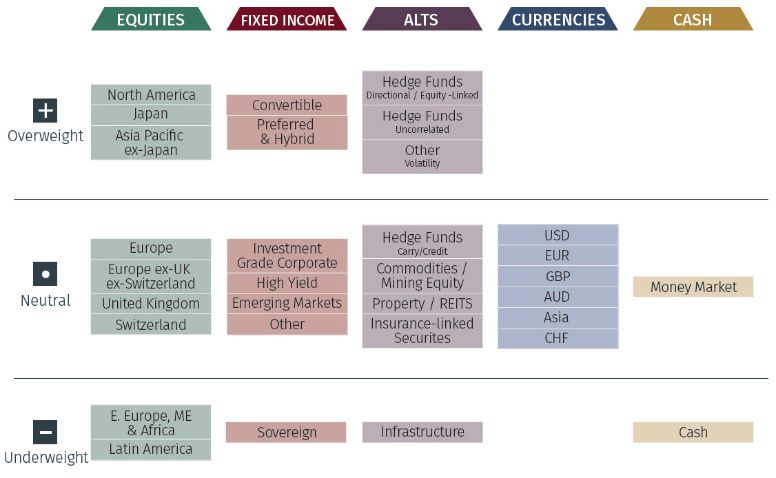

Global Asset Allocation: 12-Month Strategic Outlook

Based on a balanced mandate, the matrix below shows our long-term house view on investment strategy.

Overall Asset Allocation Views

Asset Class Breadown

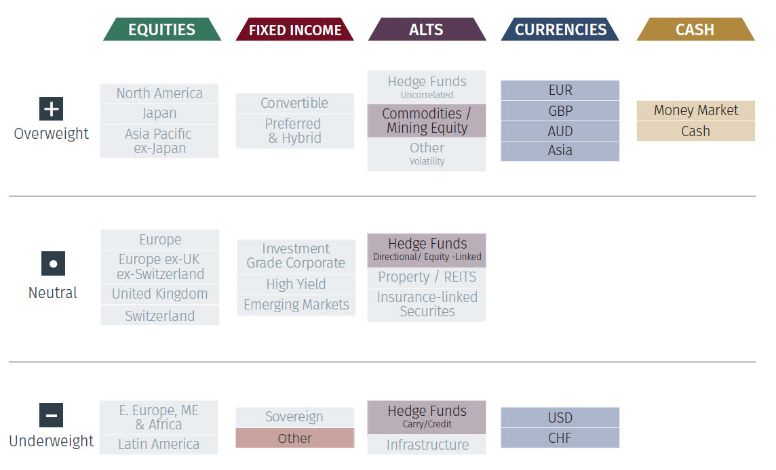

Global Asset Allocation: 3-Month Tactical Outlook

Based on a balanced mandate, the matrix below shows our short-term house view on investment strategy.

Note: The highlighted boxes indicate a difference from our 12-month strategic outlook.

Asset Class Breakdown

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.

ASSET ALLOCATION GRIDS

Please use the button below to download the full article to see asset allocation grids.