- Date:

Inview - In this publication we consider

significant developments in the world’s markets,

and discuss our key convictions and themes for

the coming months.

Editorial

Welcome to the July edition of Inview: Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

Several factors have weighed on market sentiment in recent weeks. Since the number of hospitalisations and deaths from Covid appear to be on a downward trend, one is tempted to conclude that the Covid pandemic is behind us. If so, it will underpin market confidence. While fiscal and monetary policy makers are likely to scale back their emergency measures, this is not expected to be a major headwind for asset prices. However, it is now clear that the evolution of new variants of the virus shows that risks to the recovery remain. These new variants may be more contagious and there is a risk that the immune responses driven by vaccines and exposure to earlier versions of the virus could be less effective against new strains. Thus, it is too early to declare victory.

A second factor is shifting views about the outlook for US monetary policy. Investors have been concerned about the surge in US inflation, although it appears to be peaking and the Fed has, anyway, placed more emphasis on the failure of unemployment to decline. At around 6%, the unemployment rate is plainly some distance above the level the Fed may consider consistent with its legal objective of “maximum employment.” Two factors appear to be delaying the labour market recovery. While a large number of workers who were made unemployed remained in touch with their employers and were quickly reemployed as the economy reopened, there are now few such workers left. Hiring has thus become more difficult. Furthermore, many workers have been quitting, apparently viewing it as a good time to look for a better job. US interest rate expectations have therefore been scaled back in recent weeks and this has benefited bonds and other asset prices.

Since mid-May, equity markets have staged a strong rally resulting in many indexes closing the first half of the year at new historical highs. The recent return of investors’ appetite for growth stocks has helped close the performance gap with respect to value stocks. Interestingly, despite the fall in Treasury yields, the US dollar strengthened against all major currencies and, as is often the case when that happens, emerging market assets underperformed. Commodity prices have risen, driven by oil, but the peak annual change appears to have passed and this will help ease market concerns about inflation.

In the context of very accommodative fiscal and monetary policy, the momentum in global equities appears likely to last. Hence, a slight overweight to equities remains warranted within a diversified portfolio. In contrast, the recent fall in bond yields looks hardly sustainable as economies continue to recover from the pandemic and monetary policy will be cautiously normalised. Finally, industrial metals and gold, which have recently corrected, look attractive again also as a natural hedge against inflation.

Global Asset Allocation: Summary

Equities

- Within our neutral stance on European equities we still have a bias towards quality growth companies as they will continue to be the long-term winners. However, this has been painful in the short-term as European banks have continued to perform well.

- EMEA and Latin American equity markets continue to be our least favoured areas given the challenging growth outlook relative to other regions.

- Economic growth in China looks strong in the short term and in our view equity valuations look attractive relative to other regions.

- In the US, there has been a rotation into growth stocks in June, outperforming value for the first time since April. With bond yields plateauing and heading into second earnings season we feel that expectations for growth stock earnings are quite low, relative to higher expectations for value stocks.

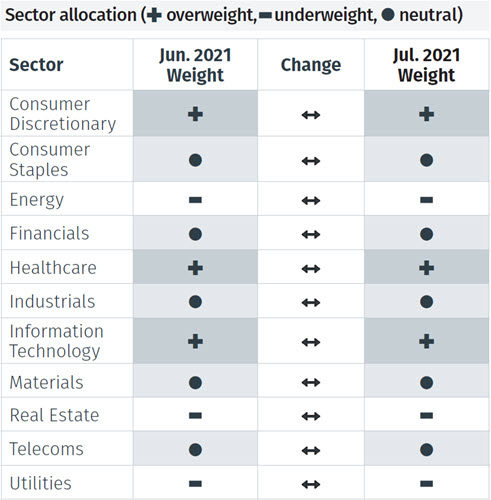

- There were no changes this month to our sector positioning, although it is notable that IT has lost relative momentum for the first time in a while. This is explained by the underperformance of large-cap tech companies. Alternatively, energy has gained relative momentum in June, although we remain cautious on the sector for the time being.

Fixed Income

- Although government bond spreads in developed markets have tightened against the US 10-year yield, in Europe spreads against the German 10-year bond have remained stable over the month. We are not overly concerned about inflation worries and remain underweight sovereign bonds.

- We have possibly been too cautious on high yield debt so far this year given very tight spreads and yields at all-time lows. Over the next 3-6 months good alpha opportunities might be created, so selectivity will be key.

- Convertible bonds continue to be our preferred area within fixed income, alongside preferred & hybrid debt, bouncing back from the dip in May.

Alternative Investments

- Last month we upgraded infrastructure to overweight as more countries develop their long-term infrastructure policies. While lower than initially touted, Joe Biden has struck an agreement with a bipartisan group of Senators on an infrastructure plan that should be a positive for the asset class.

- We retain a neutral stance on property. We are underweight on commercial and retail real estate but positive on logistics and residential, supported by record low interest rates, limited supply during the virus induced downturn and the fact that "nesting" habits will likely continue to remain in place.

Currencies

- The US dollar has strengthened against most developed currencies following the June FOMC meeting. This is reflected in traders’ commitments, which have become more bullish on the US dollar. In terms of valuation, the US dollar remains slightly overvalued in PPP terms against the EUR, JPY, GBP and CHF and we remain underweight for the time being.

- We are paying close attention to the Japanese yen and whether it will weaken further against the US dollar. Further weakening would favour value stocks in Japan.

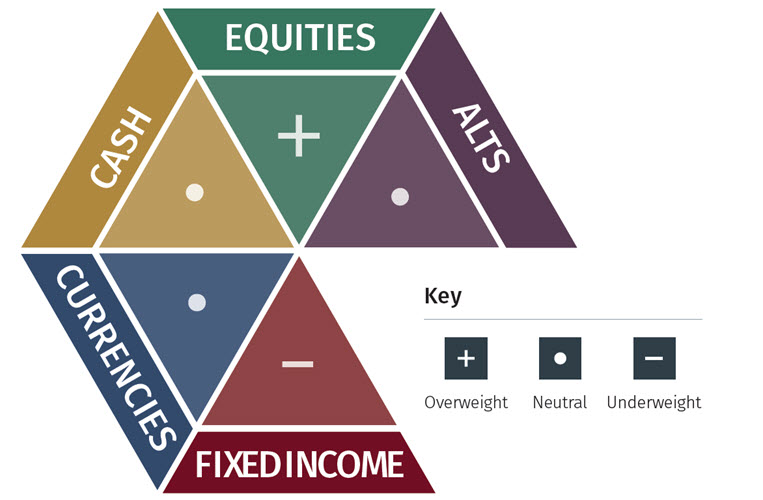

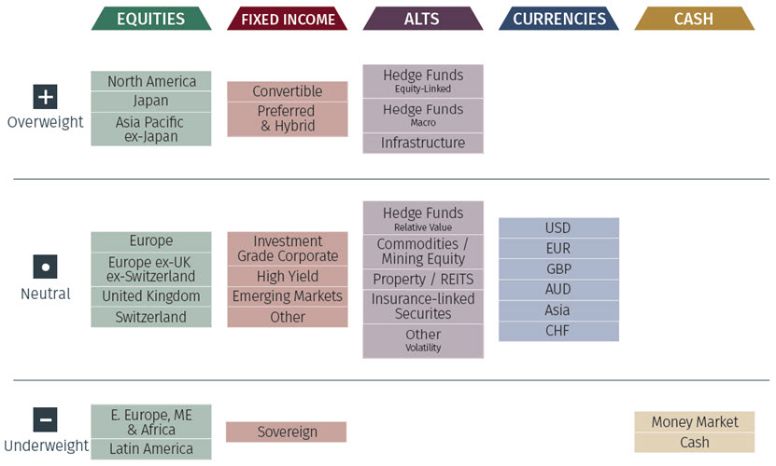

Global Asset Allocation: 12-Month Strategic Outlook

Based on a balanced mandate, the matrix below shows our long-term house view on investment strategy.

Overall Asset Allocation Views

Asset Class Breakdown

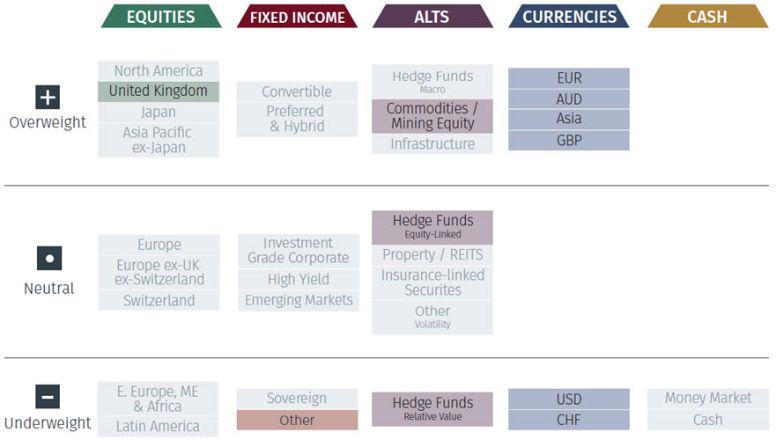

Global Asset Allocation: 3-Month Tactical Outlook

Based on a balanced mandate, the matrix below shows our short-term house view on investment strategy.

Note: The highlighted boxes indicate a difference from our 12-month strategic outlook.

Asset Class Breakdown

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.

ASSET ALLOCATION GRIDS

Please use the button below to download the full article to see asset allocation grids.