- Date:

Insight - Although Covid concerns will feature in the first part of the year, we are generally optimistic about the outlook for global economic growth in 2022. With inflation rates set to fall back, the economic backdrop remains generally benign.

OVERVIEW

The transition to the post-Covid world economy has hit turbulence. Inflation rates have soared; recovery may turn to recession; and globalisation to autarky. Those concerns will not quickly fade.

A polycrisis

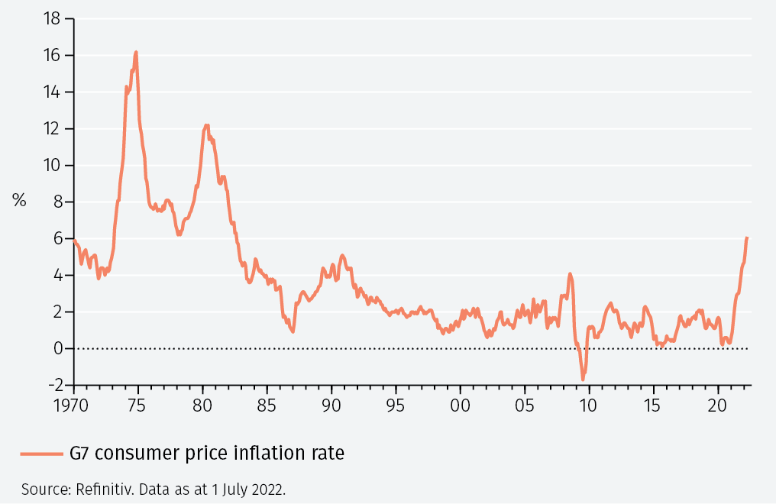

The major advanced economies are seeing the third spike in inflation since the 1970s (see Figure 1). Inflation rates close to, or above 10% are expected in the second half of the year. Central banks are fighting the trend with higher interest rates but that means the anticipated recovery in economies has been transformed into fear of recession. The deflationary forces of globalisation are in retreat. Self-sufficiency is the aim in areas from energy to food and semiconductors. Trust in many western political leaders, never high, has reached new lows. And the ability of ‘strongman’ leaders to guide economies is in question:1 China has extended its zero-Covid policy to 2027; Russia continues to fight its war in Ukraine; new strongmen in Latin America have quickly fallen out of favour. Questions are being raised about the credibility and, indeed, independence of central banks. In these turbulent conditions financial market valuations have been hit and diversification has been hard to find: safe as well as risky assets have suffered. In short, the world faces a ‘polycrisis’.2

Lessons from the 1970s and 1980s

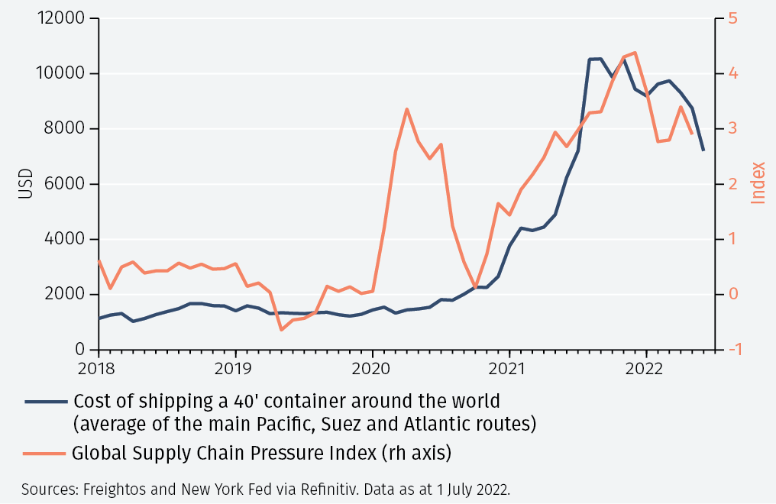

The darkest day is, as is often said, before the dawn. And, indeed, financial markets have regained some composure as we have moved into the second half of the year. Supply chain pressures and shipping costs have eased (see Figure 2).

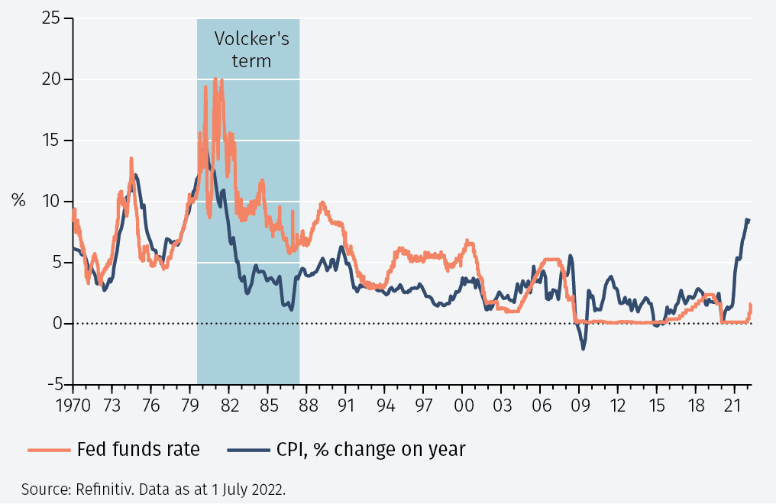

Oil and agricultural commodity prices have fallen back. Inventory shortages have, in some cases, quickly been transformed into excess stocks and liquidation sales. Even so, the potential for inflation becoming ingrained remains. The words used to describe the issues: ‘price cap’, ‘embargo’, ‘escrow account’ and ‘wage-price spiral’ comes straight from a 1970s Thesaurus. In the US, perhaps the key lesson from that period is that hesitant action on tightening monetary policy risks being ineffective in controlling inflation. In the US, inflation started to rise, under the influence of expansionary monetary and fiscal policies, from the late 1960s onwards. US interest rates, however, barely kept pace with inflation throughout the 1970s. Real rates were often negative. It was not until the monetary tightening of Fed Chairman Volcker that inflation was brought back under control (see Figure 3).3

Stagflation and a bear market

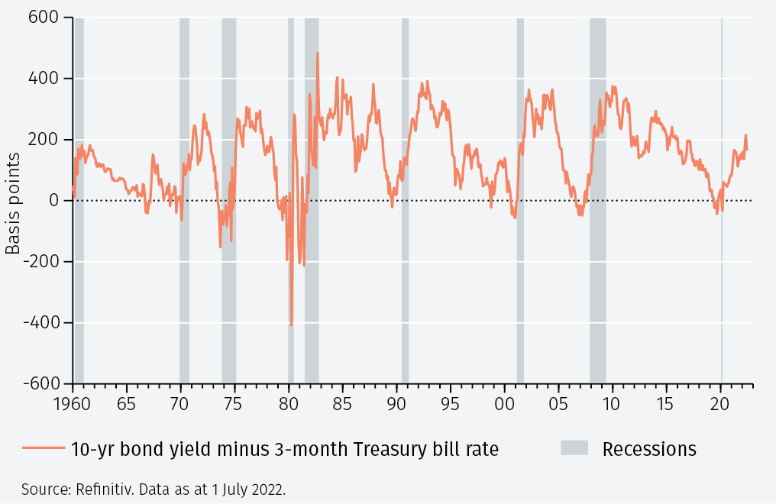

The US Fed does seem to be on a path to higher rates but there are two concerns stemming from that. First, that such action leads to an inversion of the yield curve which, in turn, presages recession (see Figure 4).

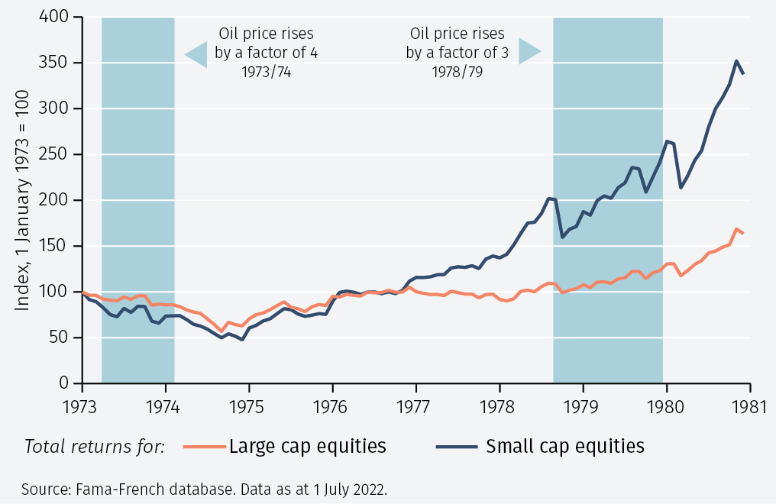

Hence, concern about recession (or slow growth) before inflation has been brought under control – stagflation – has surfaced. Second, higher interest rates and bond yields, by raising the discount rate used to value long-term assets, adversely affect the equity market. In the 1970s, with two oil shocks, large cap US equities essentially traded sideways as growing earnings were undermined by lower multiples. This period, however, saw the discovery of the ‘small cap phenomenon’. Such companies, typically more flexible and innovative, did well (see Figure 5).

The combination of stagflation and a weak equity market is certainly not one which provides a benign scenario for financial markets. The sell-off in crypto assets and the worldwide wobble in real estate is notable in this respect. The decline in the overall value of crypto assets (some USD 2trillion) is on a par with the decline in value of dotcom companies when that boom turned to bust in the early 2000s, and with the losses in the US subprime crisis.

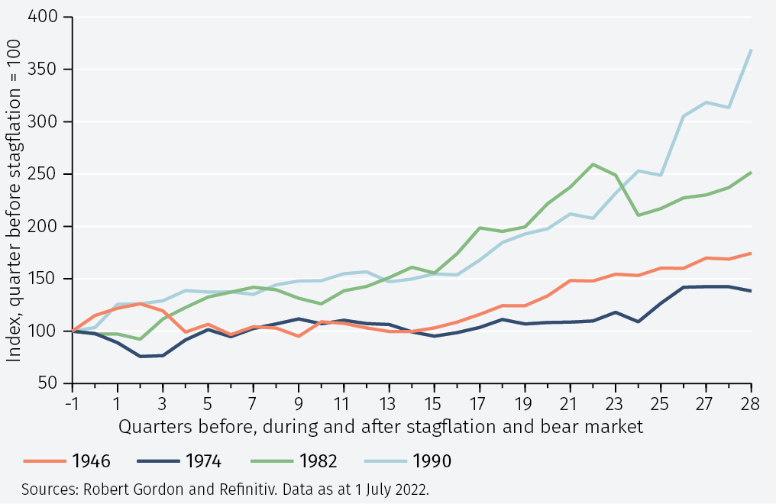

Periods of stagflation coupled with an equity bear market are, thankfully, rare. Four such periods can be identified since 1945 (see Figure 6). They have all been short – lasting just one or two quarters. And all four have seen strong equity market returns in the subsequent years. In three of those four periods – after 1946, 1982 and 1990 – inflation proved to be temporary. They produced the best returns. That historic experience suggests that central bank resistance to higher inflation is to be welcomed, not feared in financial markets.

Reassessing fundamental valuations

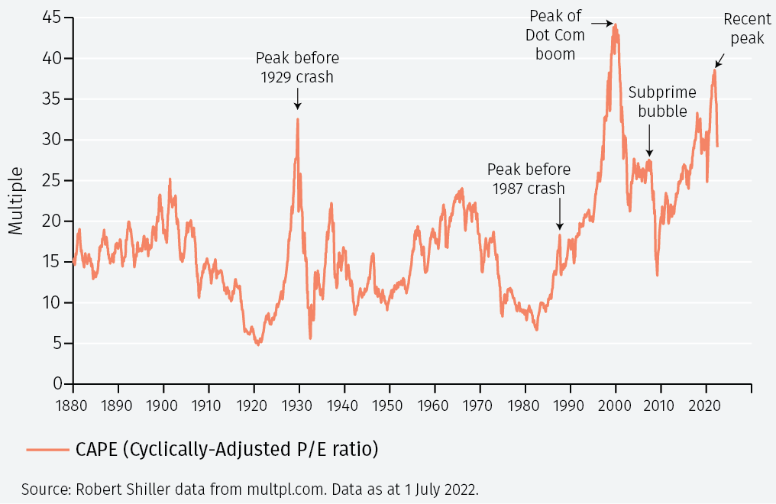

However, this rests alongside the concern that overall equity valuations are, on some measures, still too high. The cyclically-adjusted price/earnings ratio for the S&P 500 index is still at an elevated level (see Figure 7). Such a high valuation can be sustained if interest rates and bond yields are also held at low levels. And that, of course, depends on inflation returning to a lower level. This is not necessarily the sub-2% rate which was the persistent ‘problem’ of the pre-Covid era. A rate modestly above central banks’ target of 2% would, we think, be sufficient for financial markets to regain their poise. That will not be achieved in 2022. But it looks a more realistic prospect for next year.

To continue reading, please use the button below to download the full article.

Footnotes

1 The Federal Reserve Bank of Atlanta’s 4 January 2022 GDPNow forecast is for 7.4% annualised growth in Q4 2021. https://www.frbatlanta.org/cqer/research/gdpnow

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.