- Date:

Inview - In this publication we consider

significant developments in the world’s markets,

and discuss our key convictions and themes for

the coming months.

Editorial

Welcome to the June edition of Inview: Monthly Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

Global equity markets have been rangebound for some time and the trend continued in May with a 1.25% drop in the MSCI World index, most of which came on the last trading day of the month. Even if some elements of concern regarding the economic situation seem to have diminished, the risks remain mainly to the downside for growth. Nonetheless, corporate earnings beat expectations, especially for technology companies, reinforcing confidence that markets can continue to rally.

For now, markets remain caught between two opposing forces. On one side of the debate, the loss of economic momentum in both developed and emerging countries is evident. Hopes that a strong recovery in China would support global growth have collided with the reality of a more modest reopening in the absence of significant economic policy stimulus. At the same time, tensions around the US debt ceiling and the repercussions of instability in the financial sector have made financial conditions more restrictive.

On the other side of the debate, it is increasingly clear that inflation is declining globally. This is partly thanks to the fall in the prices of raw materials. Furthermore, services prices are also starting to return to levels more consistent with central banks’ targets. The tightening of monetary policy also appears to be nearing completion in many parts of the world and this is supportive for markets.

At the same time, the earnings season has been better than expected, especially for technology companies. The brighter prospects for corporate profitability in 2023 are another favorable factor for the markets.

The implications for the asset allocation of a diversified portfolio are that, in our view, a moderate overweight in both equities and bonds remains appropriate. However, some adjustments in the allocation within asset classes are advisable. Within equities, uncertainty around the Chinese recovery and its spillover into Europe argue for a trimming of the overweight in Asian equities, a reduction to neutral of the exposure to European markets and a neutral position on emerging Europe and the Middle East. In contrast, attractive valuations and solid performance of Japan equities warrant an overweight position.

Among fixed income assets, increased bond yields and the nearing of the end of monetary policy tightening make longer-dated government bonds attractive, including local currency emerging market debt. Finally, to limit the riskiness of the portfolio, exposure to high yield bonds should be reduced in favour of investment grade corporate bonds.

Asset Allocation

Global Allocation

The global economic outlook continues to reflect a weakening of economic conditions. The deterioration in manufacturing activity over the recent months has been offset by strong performance of services. However, the negative slope in the US yield curve suggests the US economy is still expected to weaken in the coming months. Data on consumer prices revealed that headline inflation has rolled over. However, core inflation remains elevated, contributing to high levels of uncertainty in markets over future central bank actions. These mixed economic signals are normally associated with an inflection point in the cycle and therefore our asset allocation needs to reflect this.

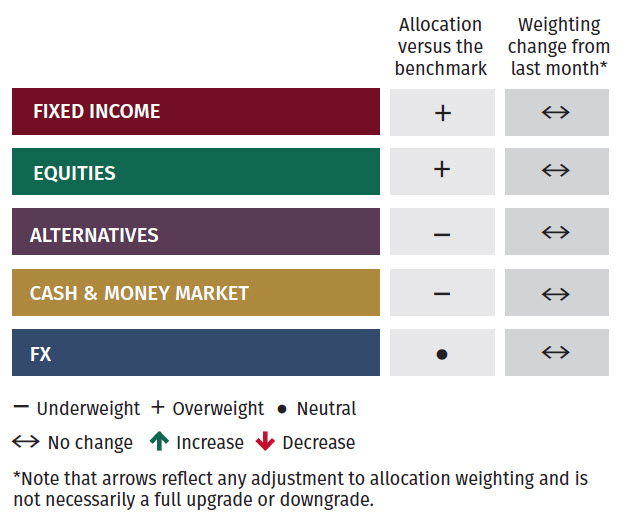

No changes were made to our broad asset allocation positioning, reflective of the overall uncertain environment. We maintain a slight overweight to equities but could look to reduce exposure once consensus on the asset class turns more bullish. Our small overweight to fixed income was also held.

Fixed Income

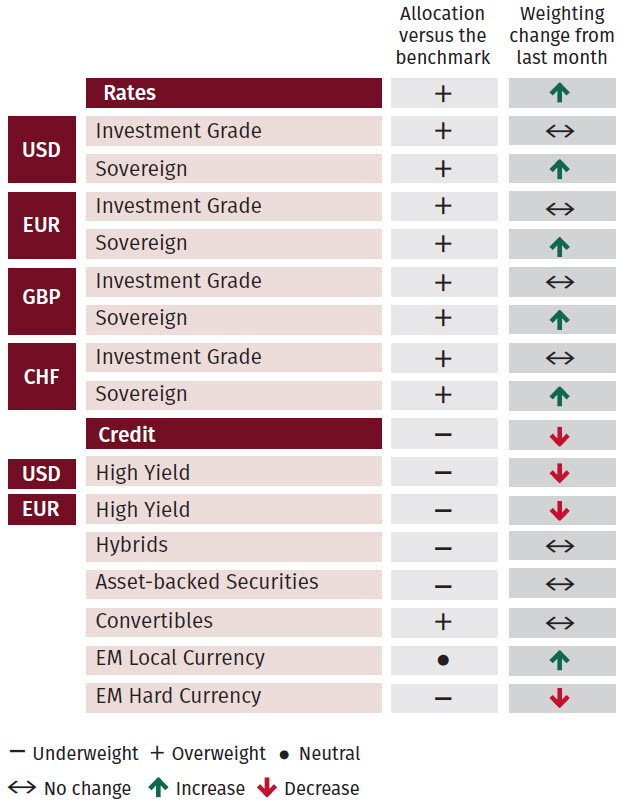

Within fixed income, markets currently anticipate the Federal Reserve will cut rates by the end of the year as inflation is expected to decelerate. Therefore, in the context of a decelerating economy, declining inflation, and tight spreads in both US and European credit, we are reducing our exposure to high yield. Additionally, in response to changes in rate expectations and the recent increase in yields, portfolio duration is being increased to levels around 5-7 years by adding to sovereign bond exposure across currencies. Investment grade spreads remain attractive and therefore we maintain our overweight position.

In contrast with the US, in Europe and the UK interest rates are not expected to roll-over until early 2024, which should contribute to the weakening trend of the US dollar in the second half of the year. Finally, given the outlook for US rates and improving fundamentals of emerging market (EM) currencies, we are increasing exposure to EM local currency debt. Meanwhile we are slightly reducing EM hard currency debt.

Equities

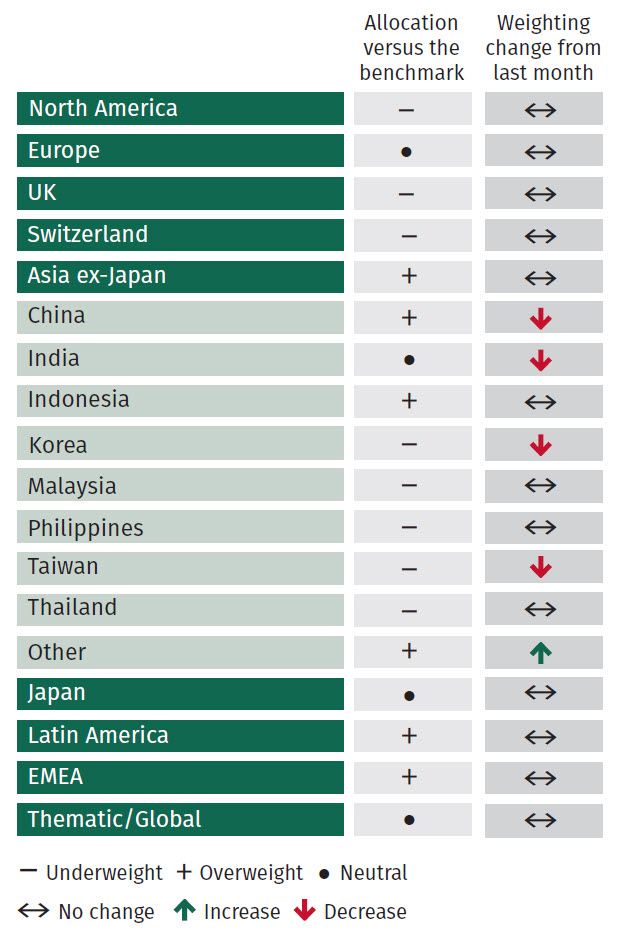

Within our equity exposure, we are upgrading UK equities to a neutral position versus the benchmark, reflecting an improvement in technical factors and more attractive valuations. We are also taking profits in Europe, downgrading our positioning to neutral relative to the benchmark. However, given the increase in the weight of European stocks in the MSCI AC World index in 2023, our absolute exposure to the region is increased relative to last month. Our allocation to Japanese equities was also increased to reflect our overweight conviction.

To make way for these increases we are reducing our allocations to Asia ex-Japan and EMEA. Within Asia ex-Japan the year-to-date performance of Chinese equities has been disappointing, despite earnings upgrades, improved economic data and attractive valuations. We are reducing our allocation to Asia ex-Japan but maintaining a relative overweight. The reduction in EMEA positioning reflects the tougher conditions in South Africa and Turkey.

Alternatives

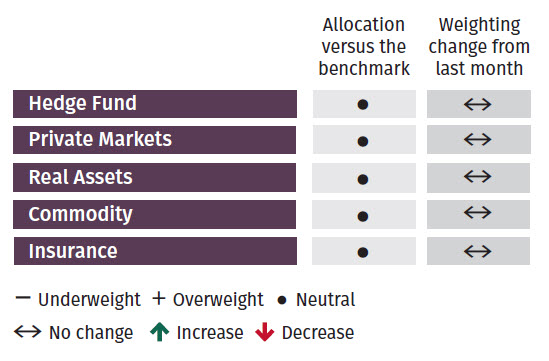

No changes were made to our alternatives exposure this month. We remain cautious on the real estate sector owing to liquidity concerns. Commodity positioning is neutral with our focus being on gold exposure. While oil markets had a small pick-up after the OPEC decision to cut production the impact has been more muted than what was initially expected by markets.

Within hedge funds, heightened volatility stemming from uncertainty in inflation and rates should be supportive for equity market neutral managers. Similarly, commodity trading advisor strategies are preferred in the context of more market volatility.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document. The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.

Independent Asset Managers: in case this document is provided to Independent Asset Managers (“IAMs“), it is strictly forbidden to be reproduced, disclosed or distributed (in whole or in part) by IAMs and made available to their clients and/or third parties. By receiving this document IAMs confirm that they will need to make their own decisions/judgements about how to proceed and it is the responsibility of IAMs to ensure that the information provided is in line with their own clients’ circumstances with regard to any investment, legal, regulatory, tax or other consequences. No liability is accepted by EFG for any damages, losses or costs (whether direct, indirect or consequential) that may arise from any use of this document by the IAMs, their clients or any third parties.