- Date:

- Author:

- Stefan Gerlach

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

Financial variables are more uncertain than many investors recognise. That message is worth recalling at the present juncture where both short-term and long-term interest rates are seen as close to their peaks. While many commentators may expect both to decline slowly, history suggests that they may move by large amounts in either direction in the coming months. In this Macro Flash Note, Chief Economist Stefan Gerlach looks at historical data for three-month and 10-year Treasury yields to show just how difficult they are to predict.

In thinking about asset allocations, investors try to ascertain what, in their opinion, is the most plausible outcome for stock prices, bond yields, and exchange rates. In doing so they often disregard the fact that financial variables are highly uncertain. While it is important to have a view of what one considers the most likely evolution of market prices, investors should also be aware that in practice the future often plays out in unpredictable and unexpected ways.

Source: FRED. Data as at 06 October 2023.

As an illustration, consider the evolution of three-month and 10-year Treasury yields since the early 1960s shown in the graph above. While these yields often move little from month to month, on occasion there are huge changes triggered by dramatic shifts in the economic environment. In thinking about the future, it is essential to recognise that further such shifts may occur.

For instance, the surge in yields in the late 1970s, caused by the oil shock and subsequent rapid inflation, came entirely unexpectedly to many investors, as did the period of rapid interest rate declines in the early 1980s. And who would have forecast that short term interest rates would fall so sharply after the collapse of the dot-com bubble in 2001?

Similarly, the sharp decline in short interest rates to almost zero following the collapse of Lehman Brothers in the autumn of 2008 will have been predicted by very few - if any - market participants a few months earlier. Nor will the reduction of short-term interest rates to almost zero in the immediate aftermath of the outbreak of the Covid pandemic. And few investors will have expected the rapid tightening of monetary policy by the Federal Reserve and several other central banks - and the associated surge in bond yields - in the last 18 to 24 months.

Before characterizing the degree of uncertainty in these two interest rates, note that the graph shows that calm and turbulent periods often alternate. Investment professionals will form judgements on whether the near future is likely to be tranquil or volatile and what part of the historical record is most relevant now. The statistical analysis below will disregard such information and is therefore likely to overstate the degree of uncertainty.

Next, we estimate a simple statistical model that captures the historical volatility of the two interest rates.1 We then use the model to forecast these two interest rates for the period from October 2023 until December 2025. Furthermore, we add information about the degree of precision of these forecasts by showing so-called fan charts.

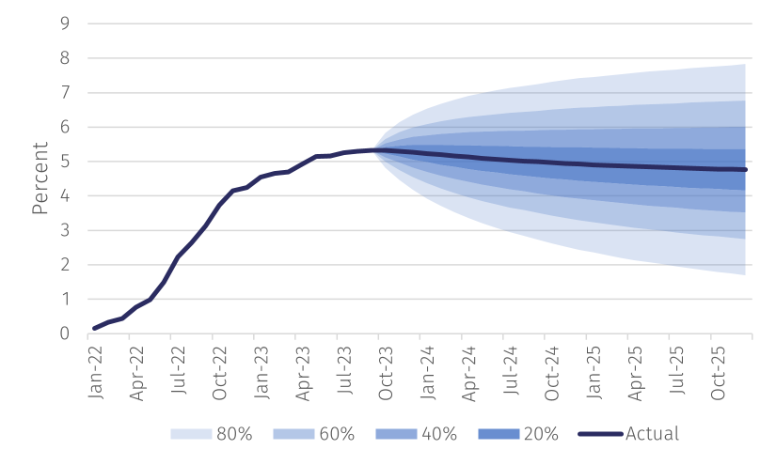

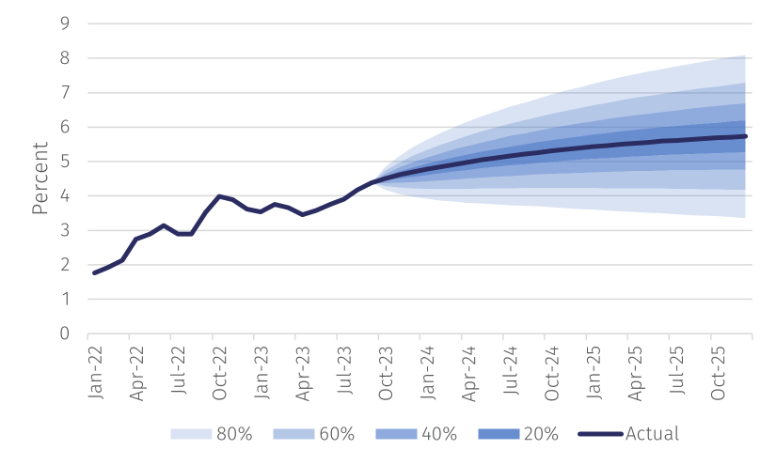

The graphs below show the results for three-month and ten-year interest rates. The most lightly coloured area in these charts, or “fans”, shows the range in which the actual value is likely to fall with 80% probability. The somewhat darker area shows the narrower range in which the actual value is likely to fall with 60% probability, and so on.

Source: EFG calculations on data from FRED. Data as at 06 October 2023.

Source: EFG calculations on data from FRED. Data as at 06 October 2023.

These fans are very broad. With a probability of 80% three-month interest rates will be someone between a little below 2% and almost 8% at the end of 2025. Ten-year yields are likely to be somewhere between a little more than 3% and about 8%. And the likelihood that they will be outside of these ranges is 20%, which is not so low that it can be ignored.

The extreme degree of forecast uncertainty is not because the forecasting model is poor but because interest rates are very uncertain. Much of this uncertainty is due to occasional episodes that lead to dramatic changes in interest rates. Each episode, such as the Global Financial Crisis in 2008 or the Covid-19 pandemic in 2020, is unique, and investors whose expectations are proven wrong may be tempted to conclude that they just had bad luck. But these episodes are recurrent and the lesson to be drawn is that the future is highly uncertain. In summary, what the future will hold for investors is difficult to predict.

1 A VAR(2) model estimated on monthly data from March 1962 to September 2023 is used.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.