- Date:

- Author:

- Amanda Cotti

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

On 26 July the International Monetary Fund (IMF) released an update to its World Economic Outlook (WEO).1 Although the forecast for global growth was revised slightly higher for 2023, the global recovery is slowing amid widening divergences across economic sectors and regions. In this Macro Flash Note, Amanda Cotti summarises the changes.

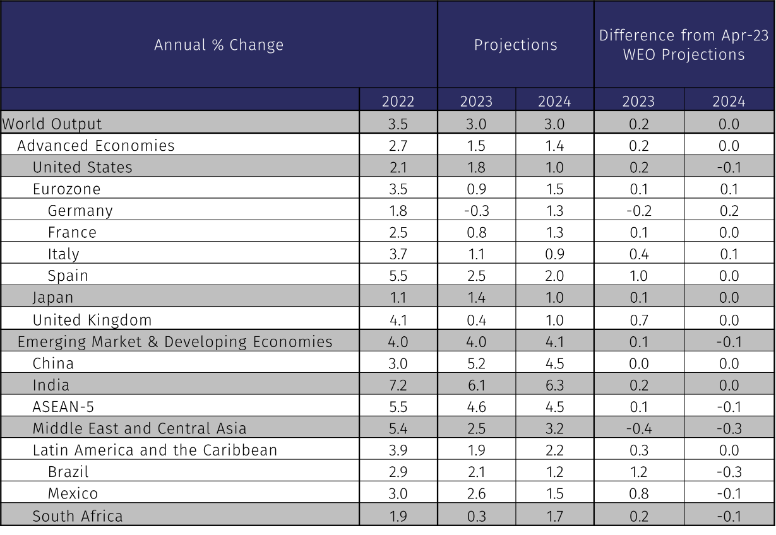

IMF outlook

The IMF revised up its global growth projection for 2023 by 0.2% compared to the previous estimate in April 2023. The new forecast for global growth is 3.0% for both 2023 and 2024. However, there are concerns about the growth slowdown in advanced economies, particularly the United States and the eurozone.

Source: IMF, World Economic Outlook Update, July 2023.

Economic growth in the United States is forecast to slow from 1.8% in 2023 to 1.0% in 2024. The upward revision to the US forecast in 2023 is due to strong consumption growth in Q1 2023, supported by a tight labour market that boosted real incomes and vehicle purchases. This positive trend is expected to be brief as consumers have largely used up their pandemic-related savings, and also due to the lagged impact of interest rate increases.

Growth in the eurozone is expected to decline from 3.5% in 2022 to 0.9% in 2023 before recovering to 1.5% in 2024. There have been notable changes in the growth composition for 2023, with the Italian forecast revised up by 0.4% and predicted growth in Spain raised by 1.0%, benefiting from strong performance of services and tourism. Conversely, growth in Germany was revised down by 0.2%, leading to a projected contraction of -0.3% due to weak manufacturing output and an economic downturn in Q1 2023.

In the UK, economic growth is predicted to decrease from 4.1% in 2022 to 0.4% in 2023, then recover to 1.0% in 2024. The 0.7% upward revision for 2023 is due to strong consumption and investment, fueled by lower energy prices, reduced post-Brexit uncertainty (after the Windsor Framework agreement), and a resilient financial sector after global banking stresses subsided in March.

Emerging markets and developing economies are projected to have stable growth at 4.0% in 2023 and 4.1% in 2024, with slight revisions of 0.1% for 2023 and -0.1% for 2024. However, this overall stability masks divergence, as approximately 61% of economies in this group are expected to grow faster and the rest, including low-income countries, will experience slower growth in 2023. The forecast for China is unchanged at 5.2% in 2023 and 4.5% in 2024, though investment has been negatively impacted by the real estate downturn. Growth in India is projected at 6.1% in 2023, with a revision of +0.2% due to stronger domestic investment.

The upward revisions for Latin America and the Caribbean for 2023 are due to stronger-than-expected growth in Brazil, which has been marked up by 1.2% since the April WEO. This growth improvement in Brazil is driven by a surge in agricultural production in Q1 2023, leading to positive spillovers to activity in the services sector. Additionally, growth in Mexico has been revised upward by 0.8% to 2.6%, with a delayed post-pandemic recovery in services and positive spillovers from resilient US demand.

Risks to the outlook

Risks are tilted toward the downside, including persistent inflation, financial market repricing, underperforming recovery in China, increasing debt distress, and geopolitical tensions. Tight labour markets and exchange rate depreciation could lead to higher inflation in some regions, while financial markets' misalignment with policymakers' tightening expectations may cause asset price falls and tighter financial conditions. A less favourable outlook for growth in China could affect trading partners, and high borrowing costs for emerging economies pose debt distress risks. Additionally, geopolitical tensions could hinder multilateral cooperation on global public goods provision.

In summary, the global economy displays short-term resilience, but the pace of recovery is falling. Advanced economies, including the US and eurozone, are grappling with growth concerns while emerging markets and developing economies demonstrate stable growth. Despite these positive signs, risks like inflation, financial market fluctuations, recovery in China, mounting debt distress, and geopolitical tensions warrant close monitoring. Taking a cautious approach will be essential to navigate these challenges.

1 See https://go.pardot.com/e/931253/look-update-july-2023-Overview/3f6v4/239594997?h=dB-vLkm9ZZ9Z4kEaVQk89xNBjMfye0xPxMFoBEktTos

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.