- Date:

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

US small-cap companies had a strong start to the second half of the year, with a rally of over 10.5% so far in July, after underperforming large-cap companies by almost 15% in the first half of 2024. The weaker-than-expected reading of the June Consumer Prices Index (CPI) index triggered a rotation from investors into parts of the market that had so-far lagged. We believe that while the asset class may look attractive, investors should remain selective in their small-cap exposure.

A change in sentiment

In June, US CPI headline and core inflation were lower than expected. The new evidence that inflation is returning towards the Fed target raised the probability that interest rates will be reduced in the remainder of 2024. According to futures contracts, a 0.25% reduction in the fed funds rate is fully priced in at the Federal Open Markets Committee (FOMC) September meeting.1

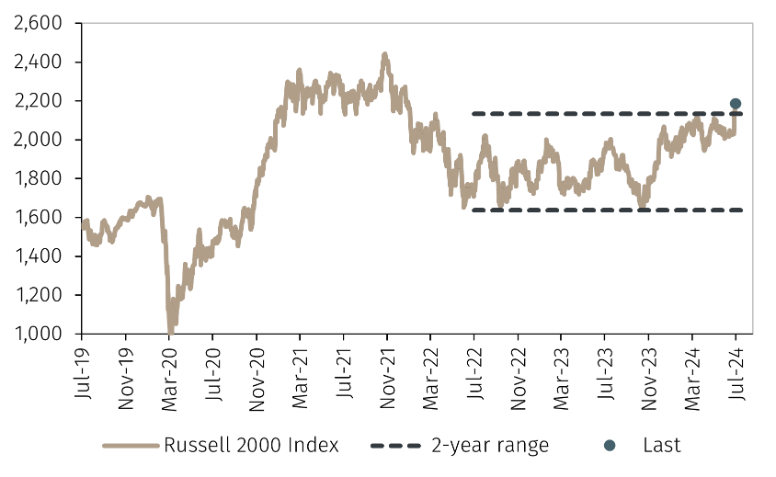

This led to a change in sentiment from investors who sold mega-cap technology stocks and turned to other parts of the market that had underperformed year-to-date (YTD), namely small-cap stocks. The Russell 2000 index, which tracks the performance of US smaller companies, had the largest percentage increase since November 2023, when the Fed’s pause on its interest rate hike cycle triggered a similar rally in the sector. From a technical point of view, the index broke the top of its 2-year range, with investors remaining confident this market can continue to trend higher (see Chart 1).

Source: LSEG Data & Analytics and EFGAM. Data as of 16 July 2024.

Key drivers: profitability, valuation, and cash flow generation

Small companies are more sensitive to interest rates, as they are more dependent on external financing for growth than large caps. Therefore, the potential for lower interest rates in the future would support the sector. However, this could become an issue for some firms if the easing of monetary policy, as a result of a deceleration in economic activity, negatively affects profitability. Investors should therefore tread with caution on how they approach their allocation to the sector as not all small companies are equal. Factors such as profitability, valuation and cash flow generation will be the key drivers to future returns for investors.

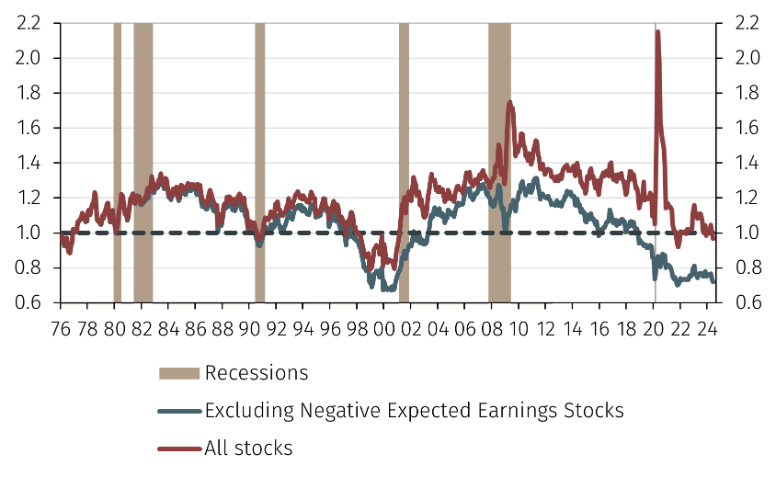

There are considerable differences among firms in the Russell 2000 index, with almost a quarter of them remaining unprofitable. These firms are unlikely to turn profitable as a result of one, or two, 25-basis-point rate cuts from the Fed this year. Therefore, it is important to be selective.

Source: Empirical Research Partners Analysis

By excluding firms with negative forward earnings, the forward Price-to-Earnings ratio of smaller companies relative to large-cap stocks looks attractive. In fact, valuations of profitable US small caps are at the lowest level since the year 2000 (see Chart 2). These are precisely the type of stocks that the New Capital US Small Cap Growth fund focuses on – highlighted by strong profit growth and relatively attractive valuations.

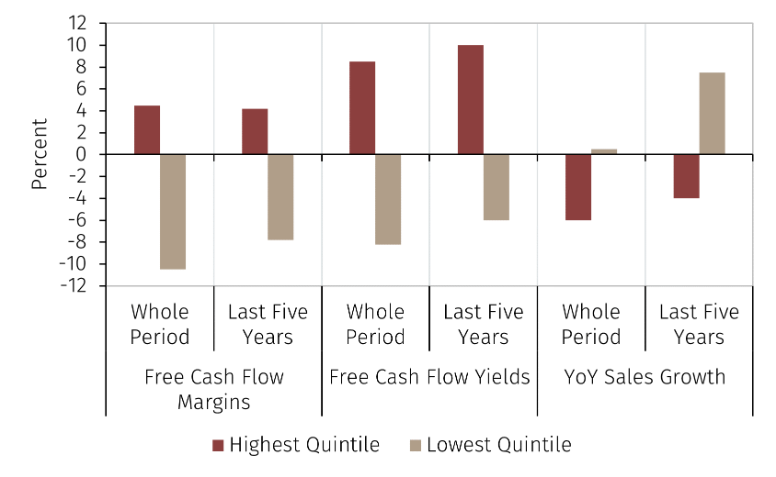

Additionally, it is important to distinguish between firms which can generate enough cash rather than focus just on its growth rate over time. The difference in returns between the highest and lowest quintiles of smaller companies based on free cash flow margins and free cash flow yields have been greater relative to those based solely on annual sales growth rates (see Chart 3).

Source: Empirical Research Partners Analysis

Investors should remain selective

Small cap companies have rallied in response to increased expectations of interest rate cuts before year end. However, signs of economic weakness in the US economy could become an issue for unprofitable firms. Investors should remain selective in this space, avoiding passive strategies in favour of actively managed ones. While sales and earnings growth is a pre-requisite for small cap performance, there is significant disparity between top and bottom performers. Additional focus should therefore be placed on firms’ profitability, valuation and cash flow generation in addition to sales growth rates.

1CME FedWatch tool, data from 16 July 2024.

New Capital US Small Cap Growth Fund

Learn moreImportant Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.