- Date:

- Author:

- GianLuigi Mandruzzato

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

In this Macro Flash Note, GianLuigi Mandruzzato looks at the result of the last ECB meeting and the implications for the path of monetary policy.

The ECB raised interest rates by 0.5% in March, as anticipated despite recent developments in the international banking sector. However, it acknowledged that recent events increase uncertainty regarding the economic outlook. It therefore refrained from giving precise indications about the outlook for policy.

President Lagarde stated that henceforth monetary policy will be decided based on new information, focusing on three elements:

- The assessment of the inflation outlook based on economic and financial data.

- The dynamics of underlying inflation, that is, excluding energy and food prices.

- The intensity of the transmission of past interest rate increases.

Despite the lack of precise guidance, the observation that inflation is expected to “stay too high for too long” indicates that the ECB maintains a tightening bias. During the press conference, President Lagarde also clarified that if new data supported the ECB’s base case scenario despite the greater uncertainty that has emerged in recent days, the Governing Council knows it has “more ground to cover" in raising rates to a level that is adequate to bring inflation back to the 2% target.

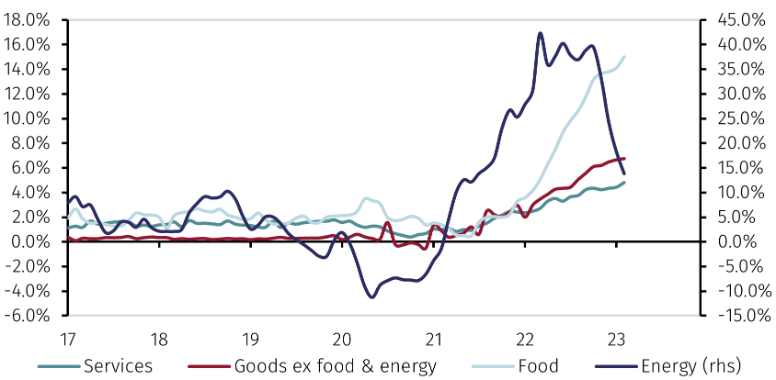

In light of the latest high inflation data, this is not surprising and likely keeps the option of further interest rate increases at the heart of the ECB’s internal debate (see Chart 1). At the same time, barring a rapid resolution of financial sector tensions, the pace of increases is likely to be more moderate in the coming months than at the beginning of the year.

Source: Refinitiv and EFGAM calculations. Data as at 17 March 2023.

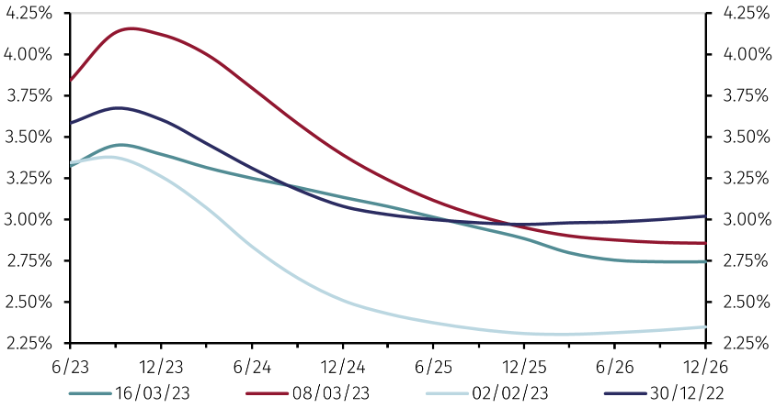

Market expectations embedded in short-term rate futures contracts price in no more than two further rate increases of 0.25% and suggest that rates will peak during the third quarter of 2023 (see Chart 2). President Lagarde’s comments and the high probability that inflation will be much higher than 2% for some more time make this scenario perhaps too optimistic. It would not be surprising if, in the coming weeks, market expectations of eurozone interest rates are revised upwards, while remaining lower than the peak seen before tensions emerged in the financial sector.

Source: Refinitiv and EFGAM calculations. Data as at 17 March 2023.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.