- Date:

- Author:

- Daniel Murray

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

Talk of a US recession has subsided over the past couple of months as confidence has grown that a soft landing will be achieved. However, it may be premature to make this call. In this Macro Flash Note, Daniel Murray reviews the evidence and highlights some of the things to look out for in the months ahead.

There is no official definition of recession, something that makes it problematic to identify one. For some, two consecutive quarters of negative GDP growth constitutes a recession but that definition is not universally accepted and does not by itself encapsulate sufficient granularity to distinguish between a regular slowdown in growth and something more painful. In the US, the National Bureau of Economic Research (NBER) has become the official arbiter of when a recession has taken place, although they typically only make the call several months after the start of the recession. Nonetheless, it is useful to look at the criteria the NBER considers when making its judgement call.

The NBER does not explicitly reveal a quantitative methodology nor a finite list of indicators it looks at. However, it does identify five data series that it looks at in making its judgement. These are:

1. Real manufacturing and trade sales

2. Industrial production

3. Real personal income less transfers

4. Average of payroll and household employment

5. Monthly GDP

Source: NBER, Census Bureau, Macro Advisors, Bureau of Economic Analysis, EFG calculations. Data as at end October 2023.

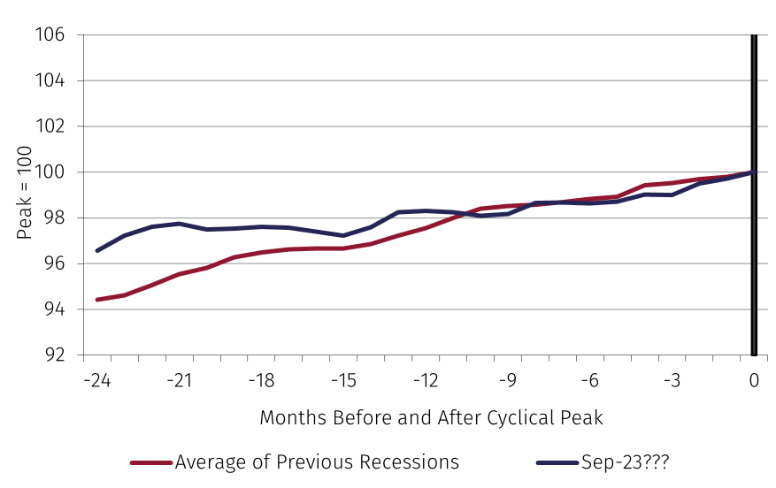

Chart 1 plots the average of these five indicators and also the historical average across all recessions since April 1960. The horizontal axis shows the number of months prior to the one in which the recession was called. For the current cycle, the latest data point in the chart is September 2023; -12 on the horizontal axis therefore corresponds to September 2022. All series are indexed so that the value is 100 in the month in which the recession began. The chart shows that current experience is very similar to the average experience of the previous nine recessions, especially over the prior 12 months. This does not imply that a recession is about to start but it does indicate that we should not rule out the possibility of one starting over the next few months - even though there are no obvious signs of recession at present.

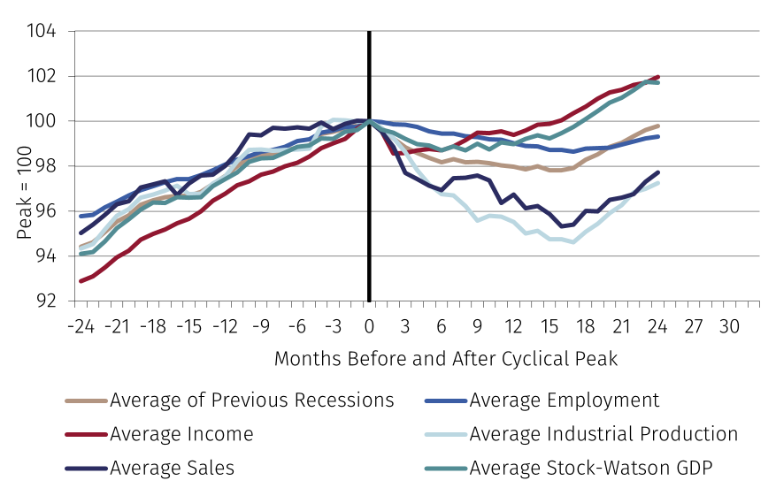

A separate issue relates to the question of the typical behaviour of these indicators once the recession has started. This is illustrated in Chart 2, which highlights three interesting points. First, it shows how recessions typically begin without warning, but once a recession has started the indicators deteriorate rapidly. It is not that the pace of growth gently slows before gradually turning negative, but rather that prior to the cyclical peak all indicators appear to be growing comfortably before suddenly experiencing a downturn. Secondly, the chart shows how the variables are highly correlated: they all deteriorate at a similar time. Thirdly, there is variation across the indicators in terms of the depth and length of the peak-to-trough drawdown.

Source: NBER, Census Bureau, Macro Advisors, Bureau of Economic Analysis, EFG calculations. Data as at end October 2023.

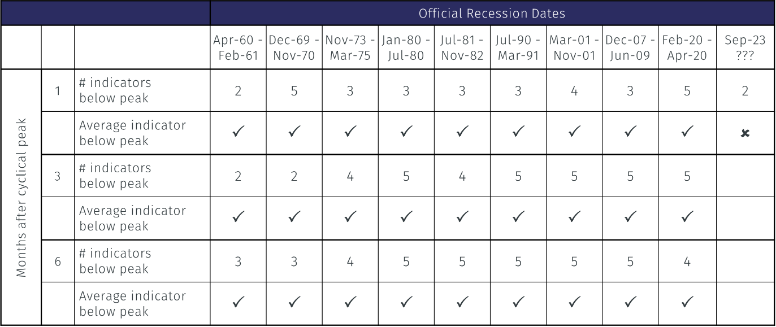

All recessions have their own nuances and peculiarities so it is possible that some subtleties are hidden in the averages. To explore the data in more detail, analysis of the behaviour of the individual indicators in prior recessions was performed. Each indicator was assessed 1, 3 and 6 months after the cyclical peak. The data is summarised in Table 1.

Source: NBER, Census Bureau, Macro Advisors, Bureau of Economic Analysis, EFG calculations. Data as at end October 2023.

The analysis shows that not all of the five indicators need to be in contraction for the NBER to call a recession. However, typically at least three are declining one month after the peak in the cycle. Furthermore, over all time periods the average of the indicators has been in contraction in all nine prior recessions. The far-right hand column of the table shows that the peak is highly unlikely to have been in September.

The main conclusions from this analysis are as follows:

- Economic conditions change very quickly and with little warning. One month the data can look robust, the next in decline. This means that we should not be complacent about the US economy in the current cycle.

- Typically, several important indicators turn at the same time.

- Whilst not a hard rule, if the average of the NBER’s five indicators is in decline that is a strong signal that the economy is in recession.

In terms of the implications for markets, it does not matter whether the NBER calls a recession or not. It is simply a label and the NBER might wait a year or more after the event before saying that the economy peaked in a particular month. Markets are discounting mechanisms and will typically anticipate economic slowdowns ahead of time, long before the NBER has made its official pronouncement.

However, economic slowdowns – recessions or otherwise - are nonetheless important events for markets since they are almost always accompanied by challenges to the corporate sector: declining profits and rising defaults. At the same time, any meaningful contraction in activity normally results in an easing of monetary policy.

It is therefore incumbent on investors to monitor the data closely for any signals that we are close to the tipping point. At the moment that does not seem to be the case but it is quite possible that the situation will change over the next few months. While there is limited evidence of a widespread economic slowdown in the US at present, the economy is looking similar to previous situations immediately prior to the start of a recession.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.