- Date:

- Author:

- GianLuigi Mandruzzato

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

The European Central Bank (ECB) has indicated that its tightening cycle is approaching its end. However, public statements by Governing Council members show that the debate is ongoing about how much higher rates must be raised to bring inflation back to the 2% objective. In this edition of Infocus, GianLuigi Mandruzzato looks at the factors that will feed into the ECB’s decisions.

The ECB is expected to raise interest rates again at its meeting on 15 June and leave the door open to further increases. However, recent statements from Governing Council members highlight a diversity of views about how much higher interest rates should rise. President Lagarde has indicated three key criteria for judging whether the stance of monetary policy is appropriate: the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission.

The inflation outlook

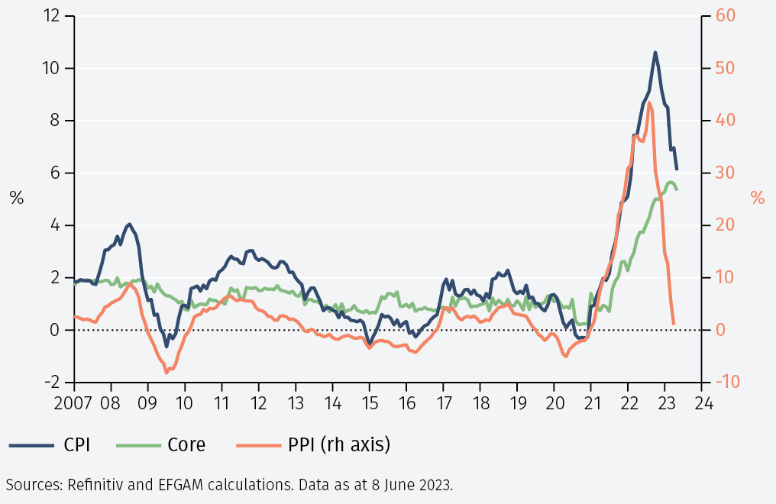

The inflation scenario has improved significantly in recent weeks. Eurozone consumer price (CPI) inflation fell to 6.1% year-on-year in May and core inflation also eased (see Figure 1). While current inflation remains elevated relative to the ECB’s 2% target, lower commodity prices – including energy, industrial metals, agricultural goods and fertilizers – suggest that inflation will fall further. These falls have led to a collapse in producer price (PPI) inflation (also shown in Figure 1). This is likely to be transmitted to lower CPI inflation in the coming months. In a sense, this will be a reversal of the surge in producer prices in 2021/2022. However, the transmission of downward shocks has historically been slower than upward shocks.

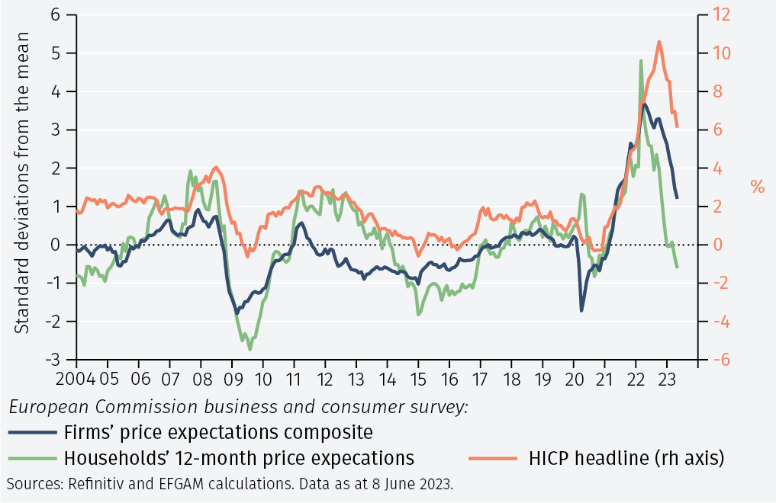

Also supporting the prospect of lower CPI inflation, corporate surveys show there is a lower tendency to increase prices compared to the end of 2022, although it remains relatively high among services firms. And consumers’ inflation expectations have dropped in recent months (see Figure 2).

Finally, it is noteworthy that the slowdown in GDP will also encourage inflation to return towards 2%. The economy went through a shallow technical recession in late 2022 and early 2023 and weakness in EU Commission and S&P Global PMI surveys suggests the soft patch could extend for a few more quarters.

Underlying inflation dynamics

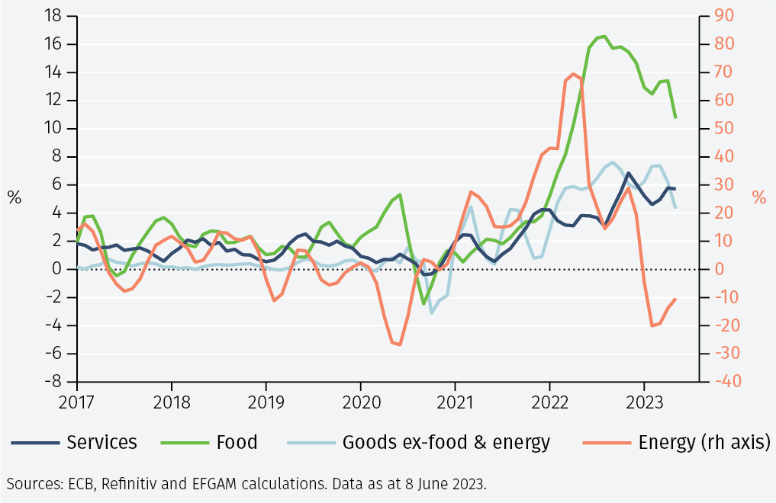

Underlying inflation has improved a little but remains too high, especially in the services sector. The annualised quarterly change in the prices of services remains just below 6% and does not show clear signs of moderation (see Figure 3).1 Although services prices increased by only 0.12% month-on-month in May, further clear signs of moderation are necessary before the ECB can conclude that services price inflation is returning towards 2%.

Conversely, the dynamics of energy, food and industrial goods prices have moderated in recent months and are likely to continue to do so, given lower commodity prices and the trend in US durable goods prices.

Monetary policy transmission

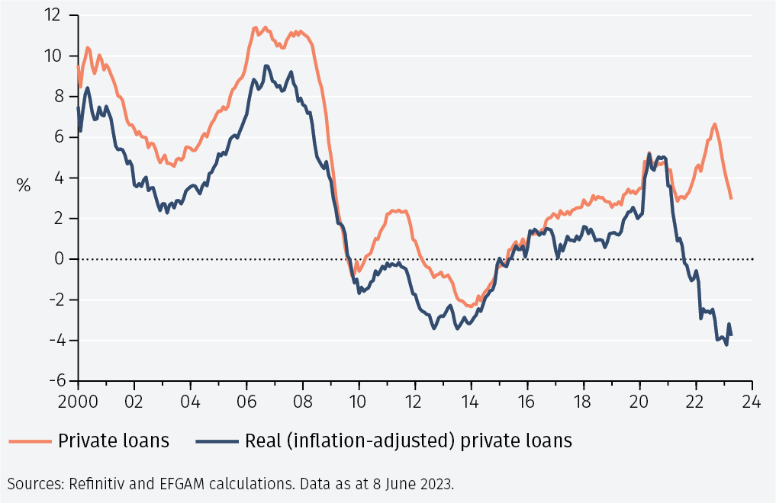

The third factor mentioned by President Lagarde was the transmission of monetary policy. She said on 1 June that “considerable tightening is still in the pipeline” even after the rapid and aggressive rate hikes totalling 3.75% implemented since July 2022. A reduction in the availability of credit is also evident, reflecting the tightening of conditions applied by commercial banks on lending to the private sector and the reaction by businesses and households to significantly reduce the demand for credit. Net credit flows have been virtually zero since September 2022 and the inflation-adjusted annual change in the stock of outstanding bank loans is already weaker than the low point reached during the eurozone debt crisis in 2011-13 (see Figure 4).

In an interview on 7 June, Executive Board member Isabel Schnabel, said that the impact of the ECB’s restrictive monetary policy “on inflation is expected to peak in 2024”. However, she noted that this process is uncertain and depends on private sector expectations. Furthermore, the cost of a policy that is not restrictive enough is higher than one that is too restrictive.

Interestingly, the responses of corporates and households to EU Commission and ECB surveys are consistent with a relatively quick return of inflation towards the ECB’s 2% target.

Conclusions

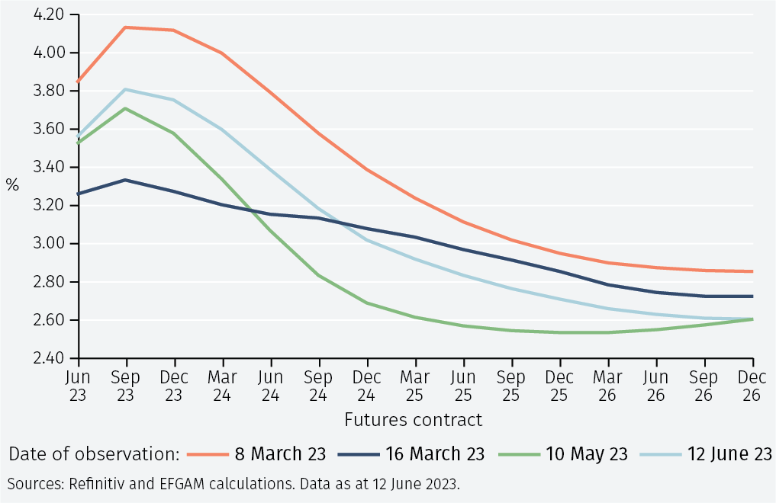

According to futures contracts, after the expected 0.25% increase at the June ECB meeting, investors fully anticipate another 0.25% interest rate increase during the summer and attach a probability of around 30% to another such increase by the end of 2023 (see Figure 5). If these projections are correct, the ECB’s overnight deposit rate would peak between 3.75% and 4%. In combination with the expected decline in inflation, short-term real rates are projected to turn positive before the end of 2023 and rise further in 2024.

Subsequently, markets are discounting a 0.25% reduction in interest rates as early as the first half of 2024, to be followed by further cuts bringing interest rates towards 2.50% in the course of 2025.

The main risk to these projections seems to be that interest rate cuts will start later, possibly towards the end of 2024 if not until 2025. This would reflect the preference of the ECB to maintain restrictive policy for longer to accelerate the return of inflation towards the 2% target and keep inflation expectations well anchored. Interest rates cuts would be delayed also if the end of the tightening cycle happened later than currently priced in by markets, perhaps because the ECB takes longer intervals between the remaining rate increases to assess how past monetary policy tightening is impacting the economy.

1 The seasonally adjusted HICP (Harmonised Index of Consumer Prices) indices published by the ECB are used for these calculations.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.