- Date:

Infocus - For some time, consumers around the world have been affected by shortages of goods, from basic necessities to microchips. At the same time, concerns about inflation have grown.

With US inflation much above the Fed’s 2% objective, it is of interest to ask what inflation rates are priced into the markets for nominal and inflation-indexed US Treasury securities. In this issue of Infocus, EFG chief economist Stefan Gerlach looks at breakeven inflation rates implied by the yields on these instruments.

With US CPI inflation running over 7% and with plenty of market commentators taking the view that it will remain much above the Fed’s 2% objective in coming years, it is interesting to consider what inflation rates financial markets are pricing in. One way to do so is to look at breakeven inflation rates, as captured by the spread between nominal and inflation-indexed US Treasury securities.

As a preliminary it should be emphasised that the market for inflation-indexed bonds is smaller and less liquid than the market for nominal bonds. This suggests that spreads between nominal and real yields do not solely depend on inflation expectations but also on supply and demand conditions in the two markets.

For instance, investors with very long-term obligations that depend critically on the price level may be keen to hold inflation-indexed bonds even at the cost of paying an ‘insurance premium’. That is, they may not want to take the risk of inflation being higher than they expect and would consequently prefer the protection of inflation-indexed bonds. They would therefore accept a real yield on inflationindexed bonds somewhat below the expected real yield on conventional bonds (their nominal yield minus the rate of inflation the investor expects during the lifetime of the bond). Consequently, the observed breakeven inflation rate will, on average, exceed the expected inflation rate.

However, the relative illiquidity of the inflation-indexed market may argue in the opposite direction: the breakeven inflation rate being lower than the expected inflation rate. The reason is that investors may require a higher real yield on inflationindexed bonds to hold them during episodes of financial stress, when they may worry about their ability to close positions quickly and cheaply. Observed breakeven inflation rates may therefore appear to decline if financial tensions erupt even if inflation expectations in truth are unchanged.

These risk and liquidity considerations are too important to be disregarded in managing a bond portfolio. However, they are unlikely to be so important as to mask the broad macroeconomic information embedded in breakeven rates, which is the focus here.

Breakeven inflation rates

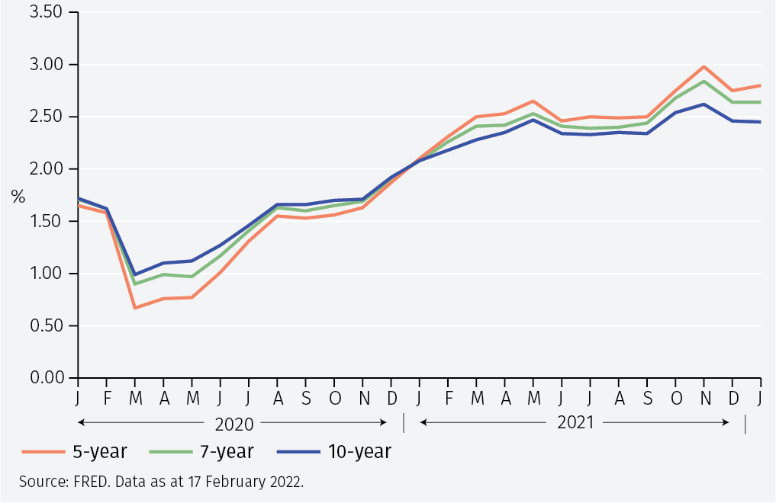

Figure 1 shows breakeven US inflation rates for 5-, 7- and 10-year maturities. These all fell abruptly as the covid pandemic started in early 2020 but have since gradually increased as inflation has risen. They peaked in November 2021 and stood at 2.8%, 2.6% and 2.4% in January 2022. These implied inflation rates are much below the 7.5% year-over-year CPI inflation raterecorded in January 2022.

The breakeven rate should reflect market participants’ inflation expectations. To see this, suppose that the nominal 5-year bond yield is 3% and the index linked 5-year yield is 1%, for a breakeven inflation rate over 5 years of 2% per annum. Suppose next that market expectations of inflation rise to 3%. In that case, the expected real return over the next 5 years on the nominal bond would be 0% versus the inflation-indexed return of 1%.

Demand would consequently shift from the nominal bond, pushing up its yield, toward the indexed bond, lowering its yield, until the spread between the two bonds equalled the expected inflation rate. While shifting inflation expectations may explain the bulk of the variation in breakeven rates, small discrepancies between expected inflation and breakeven inflation rates are possible because of the liquidity and risk effects mentioned above.

The term structure of breakeven rates

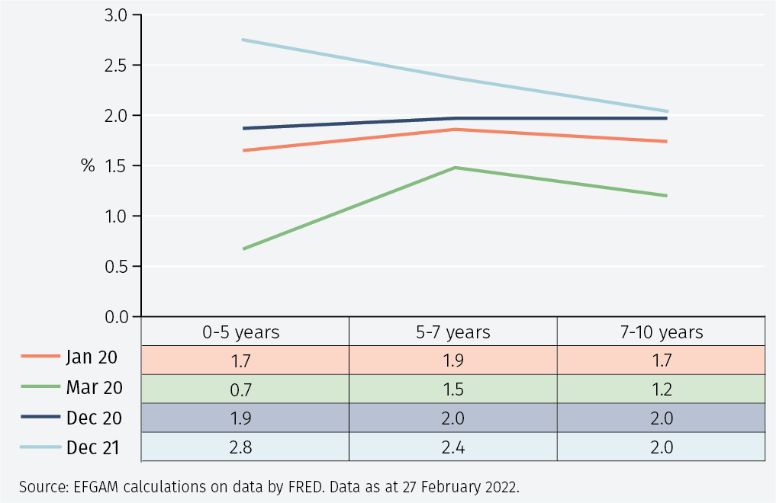

These breakeven rates can be used to compute a rough term structure for breakeven inflation.1 Figure 2 shows the same 5-year (or 0-5 years) breakeven inflation rate as in Figure 1, together with the implied 5-7 years and 7-10 years breakeven inflation rate.

Figure 2 shows that, while market participants in January 2022 expected inflation to average 2.8% over the next 5 years, for years 6 and 7 they expected it to average only 2.2% and, for years 8-10, they expected only 2.0% inflation.

The upshot of this analysis is that despite the recent high inflation rates, market participants expect inflation to fall markedly over the next 5 years and to be close to 2% during the 5-year period after that. Current high inflation rates are not expected to persist.

Inflation expectations during covid

The above analysis can be used to assess the movements in inflation expectations during the covid pandemic. Figure 3 shows that in January 2020, as the covid pandemic was starting, market expectations were for broadly constant inflation of just below 2% over the coming decade.

However, by March 2020 expectations had become much more pessimistic. The breakeven inflation rate over the next 5 years had fallen to 0.7% and longer-term inflation expectations had also fallen, but by less, from the beginning of the year.

By the end of 2020, inflation expectations had recovered to about 2% and thus slightly exceeded the levels of January. However, as inflation rose during 2021, inflation expectations ratcheted up, particularly in the 0-5 years horizon.

1 For instance, if the 5- and 7-year breakeven inflation rates are 2.8% and 2.6%, then prices are expected to increase by 5 × 2.8% = 14% over the next 5 years and by 7 × 2.6% = 18.2% over the next 7 years. Thus, the market is pricing in an average inflation rate of (18.2% - 14%)/2 = 2.1% in years 6 and 7.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.