- Date:

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

The first round of Colombia’s Presidential election will be held on Sunday 29 May. The election could lead to the victory of Gustavo Petro as the country’s first leftist president or to the continuation of the current economic model under Federico Gutierrez. In this issue of Infocus, Joaquin Thul looks at Colombia’s economic context and the main proposals from the two leading candidates.

On Sunday 29 May, Colombia will hold presidential elections. These may lead to the triumph of Gustavo Petro, from Pacto Historico, as the country’s first leftist president or to the continuation of the current economic model if Federico Gutierrez, from the conservative coalition Equipo por Colombia, wins. In the last week, Rodolfo Hernandez, a right-wing businessman with no prior experience in politics, has also joined the race.

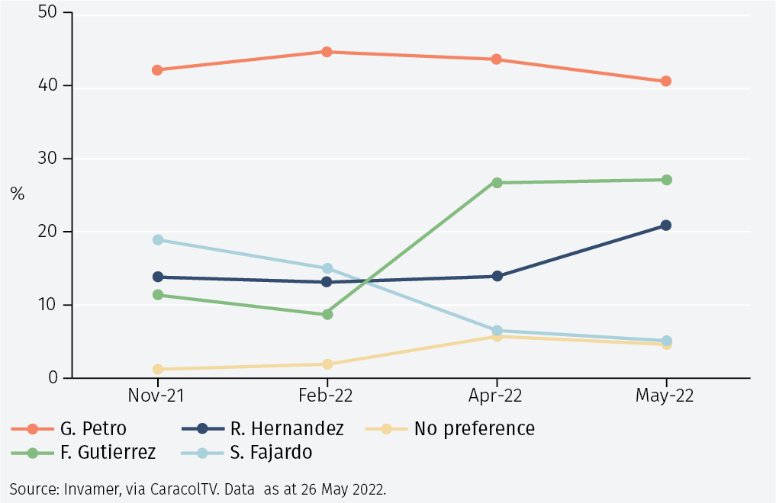

In Colombia, if no candidate receives more than 50% of the votes, the top two candidates go to a ballot. If required, the second round is scheduled for 19 June. Recent polls have shown that Petro and Gutierrez would receive 40% and 27% of votes respectively, closely followed by Hernandez with 21%, see Figure 1. This means it is unlikely that any candidate will win in the first round.

Last year both Chile and Peru elected left-wing leaders, increasing uncertainty in the region as both presidents, Boric and Castillo respectively, promised to deliver strong political change. However, months after the election not enough progress has been made on implementing new policies.

This year’s election has also been labelled as an election for change. Soaring inflation, the inability of previous governments to tackle deep social problems, poverty, unemployment and the repercussions of the Covid pandemic are prominent in voters’ minds and have led to a demand for political renovation.

The results from the Congressional elections last March added an extra layer of complexity. Congress is now highly fragmented. Petro’s Pacto Historico has the largest representation, but only 18% of votes in the Senate and 15% of the votes in the Lower House. In the event of a victory for Petro he will need the support from minority parties to govern. This resembles the situation in Peru where President Castillo has little support in Congress and faces strong opposition from other parties to pass legislation. In Colombia, both Petro and Gutierrez have experience in politics and despite their strong rhetoric, both would be less inclined to implement significant changes to an economy that is expected to grow strongly in 2022.

A positive economic context

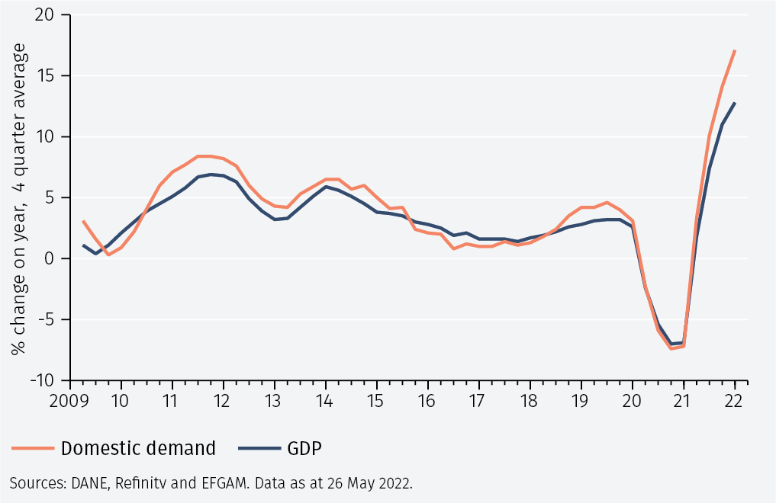

The economic backdrop in Colombia is positive. After a pick-up in GDP of 10.6% in 2021, the IMF expects Colombia to grow by 5.8% in 2022, the highest in the region and more than double the average of 2.3% GDP growth expected for South America. Growth in 2022Q1 was strong, at 4% quarter-on-quarter. This was attributed to solid domestic demand, see F igure 2. However, high inflation, which surpassed 9% year-on-year and the tightening in monetary policy carried out by Banrep, the Colombian central bank, will slow growth in the second half of this year.

The increase in commodity prices, particularly the rise in crude oil prices, has been positive for Colombia. The share of oil exports in total exports increased from 32% in previous quarters to 40% in March. With the price of oil expected to remain elevated, commodity exports will continue to strengthen.

The outlook for public finances has also improved. Colombia ended 2021 with a primary fiscal deficit of just under 4% of GDP, slightly below the 4.4% deficit in 2020 at the start of the Covid pandemic.1 In the second half of 2021 the current government passed a fiscal consolidation plan which included tax adjustments aimed at increasing fiscal revenue and changed the fiscal rule to include a limit to net debt of 71% of GDP and a provision to maintain a primary balance of at least 1.8% of GDP if the net debt limit is breached.2 The IMF expects Colombia’s primary deficit to reach 1.7% of GDP in 2022, which is slightly above the 1.2% average deficit registered on the five years prior to the pandemic.

Last month the IMF also approved a two-year arrangement of USD 9.8 billion for Colombia under the Flexible Credit Line (FCL) facility.3 This agreement will improve market confidence and, together with the country’s international reserve position of approximately USD 60 billion, will provide some insurance against external downside risks.

Tightening conditions and softening demand

Growth in 2022Q1 was mostly driven by strong domestic demand which contributed to a recovery in the services sector, while agriculture production was weak. However, rising inflation and a tightening of financial conditions by the central bank are expected to reduce household consumption and decelerate demand in the coming quarters.

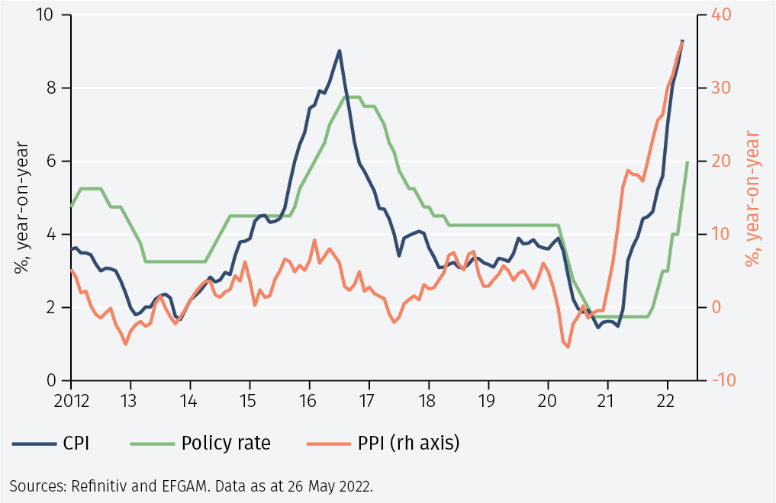

Headline CPI inflation in April reached 9.2% year-on-year, the highest level since 2000, while core CPI inflation hit 5.5% over the same period. These are above the target range of 2%-4% set by Banrep. The central bank recently raised interest rates by 100bps to 6%, emphasising the risks of a de-anchoring of inflation expectations.

Banrep has increased rates by 300bps so far in 2022 and 425bps since the rate hiking cycle began in October 2021. With inflation still to peak, the central bank will likely continue tightening monetary policy in the coming months. Some board members have suggested raising the interest rate by 150bps at their meeting in late June. Therefore, the expected tightening of financial conditions by the central bank will weigh on growth in the second half of the year.

Uncertainty on policies While the economic backdrop is relatively upbeat, there is uncertainty arising from the different policy proposals of the two frontrunner candidates.

Regarding energy policy, Gutierrez intends to continue most of the policies implemented by recent governments and promote projects to explore the production of blue hydrogen in Colombia to reduce dependency on fossil fuels. Petro also aims to promote renewable energy sources and he intends to not renew existing contracts for oil exploration in Colombia. This has sparked fears among investors and doubts from centrist voters who view this approach as too radical.

Both candidates agree on the need for a pensions reform, an improvement of the tax system and a modernization of the healthcare system. However, they differ on their approach to fiscal spending. Petro wants to promote tax reform to implement a more progressive tax system. In contrast, Gutierrez wants to promote fiscal austerity and more efficiency in public spending. He aims to reduce gross debt to 60% of GDP from 65%, aiming to recover the country’s investment grade status which was lost in July 2021.

The uncertainty generated by the election seems not to have affected domestic asset prices. Equities had a strong start to the year, with the MSCI Colombia index up 5.7% year-to-date, in line with returns in Brazil and Peru. Colombian 10-year government bond yields currently trade at 11.5%. However, in contrast to Brazil and Mexico where parts of the yield curve have inverted, the domestic yield curve remains steep, highlighting a healthier economic scenario (see F igure 5). The Colombian peso has not reacted to the uncertainty over the elections. It has depreciated by 2.4% against the US dollar so far in 2022, which is in line with the average depreciation of Latin American currencies this year.

Conclusion

We do not expect an outright winner to emerge from the first round of the Presidential elections on Sunday 29 May, with a second round needed in June. The choice for Colombians is between: Gutierrez, a more market-friendly candidate who would favour a continuation of the existing economic model; Petro, a left-wing candidate with an ambitious agenda for radical change; and Hernandez, a right-wing businessman who has captured the conservative vote. Regardless of the winner, the ability to govern will be constrained by the fragmented Congress and the resulting need to seek alliances to pass legislation. The new President will inherit an economy in a solid position despite the rising cost of living and, as in many other emerging markets, a slowing of economic activity.

Risks to growth are tilted to the downside. Uncertainty over the continuity of current economic policies remains high and the ability of the central bank to control inflation and anchor expectations will be tested. Additionally, the new administration will face challenges to consolidate fiscal accounts and reduce debt while maintaining social spending for lower income households. Overall, we maintain a positive view on Colombia which would benefit from a continuation in orthodox economic policies to contain inflation and promote growth.

1 IMF World Economic Outlook, April 2022

2 The fiscal rule in Colombia was put in place in 2011 and sets yearly spending ceilings to reduce the procyclicality of fiscal policy associated with the revenue generated from commodity exports. The rule was suspended in 2020 and most of 2021 to give the government more fiscal space to meet needs arising from the Covid pandemic.

3 The FCL was established in 2009 and allows countries with strong fundamentals, institutional policy framework and solid track records to draw on the credit line at any time. The advantage of drawings under the FCL is that they are not phased or tied to conditionality, as other IMF programs.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.