- Date:

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

Market commentators often have strong views about the outlook for interest rates. Many are now expecting the Fed to raise interest rates by half a percent at its next several meetings. But how certain should we be on the outlook for interest rates? In this issue of Infocus, EFG chief economist Stefan Gerlach looks at what can be learned from the prices of fed funds futures contracts.

Following heavy hints from members of the Federal Open Market Committee, financial market participants are pricing in a rapid tightening of US monetary policy. Thus, they expect the Fed to raise interest rates by 50 basis points both at its meeting on 15 June and its meeting on 27 July. Furthermore, many observers expect the Fed to continue raising interest rates during the autumn.

Fed policy is driven by two factors

But how much faith should we have in these predictions? It is easy to forget that on several occasions in the last 15 years the Fed has changed tack very sharply in response to changing news and data and cut interest rates by dramatic amounts.

For instance, while interest rates in the summer of 2007 stood at 5.25%, a year later they had been cut to 2%, and by early 2009 they were down to 0.25%. Plainly no market participant expected in July 2008 that the Fed would have cut interest rates by 525 basis points in 18 months’ time.

Similarly, following the onset of the Covid pandemic in the spring of 2020, the Fed cut interest rates by 100 basis points in one meeting. Again, this dramatic change in interest rates was fully unanticipated by financial market participants.

These episodes demonstrate that it may be useful to think of Federal Reserve interest rate policy as consisting of two components.

The first of these can be thought of as the normal evolution of monetary policy. This involves the Fed gradually changing interest rates in response to shifts in the outlook for inflation and the labour market. This part is generally well anticipated by financial market participants.

The second comprises very large and rapid changes in interest rates in response to entirely unanticipated events that have huge ramifications for economic conditions. In forming views about the outlook for US monetary policy, it is easy to forget about these shocks. Many market commentators appear to disregard them and therefore tend to underestimate the uncertainty of future interest rates.

The information in fed funds futures contracts

But how much uncertainty do investors attach to the outlook for interest rates? The Chicago Mercantile Exchange’s CME Fed Watch Tool, which uses the pricing of federal funds futures contracts to calculate the probabilities of various policy outcomes priced in by investors, can help in answering this question.

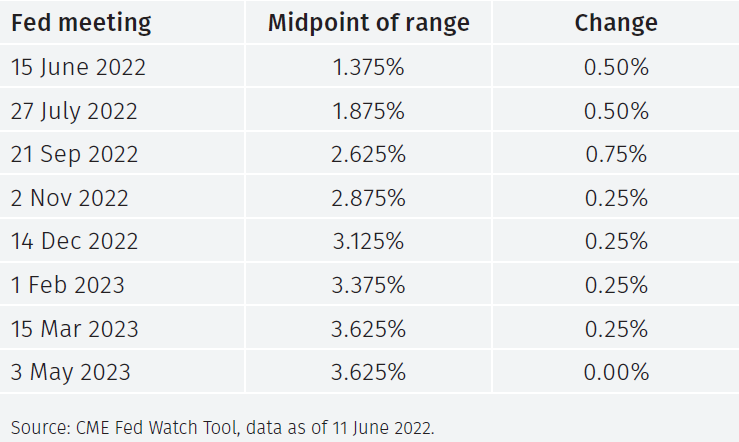

Using data from 11 June, the table below shows that financial market participants expect the Fed to raise the range for the federal funds rate by 50 basis points at each of its meetings in June and July, by 75 basis points in September, and by 25 basis points at its meetings in November, December, February 2023 and March 2023. Thus, cumulative large increases in US interest rates are expected over the coming year.

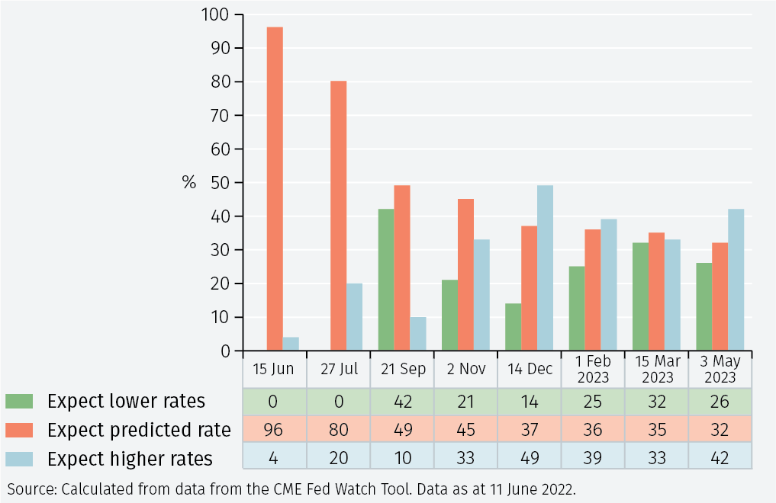

The CME’s Fed Watch tool can also be used to assess how sure financial market participants are about the outlook for interest rates. Below we look at expectations out to May 2023. The orange columns in Figure 2 show the probability attached to the most likely outcome, that is, the outcome that markets “price in.” The green columns show the probability attached to the Fed setting a lower interest rate and the blue columnsshow the likelihood attached to the Fed setting a higher interest rate than that priced in by markets.

The chart shows that investors are very certain about the outcome in June and July, viewing them as “done deals.” But from September onwards there is growing uncertainty about what rate the Fed will set. For instance, the probability that theFed will have raised interest rates by less than 175 basis points by September is 42%, and the probability that it will raise interest rates by more than 175 basis points is 10%.

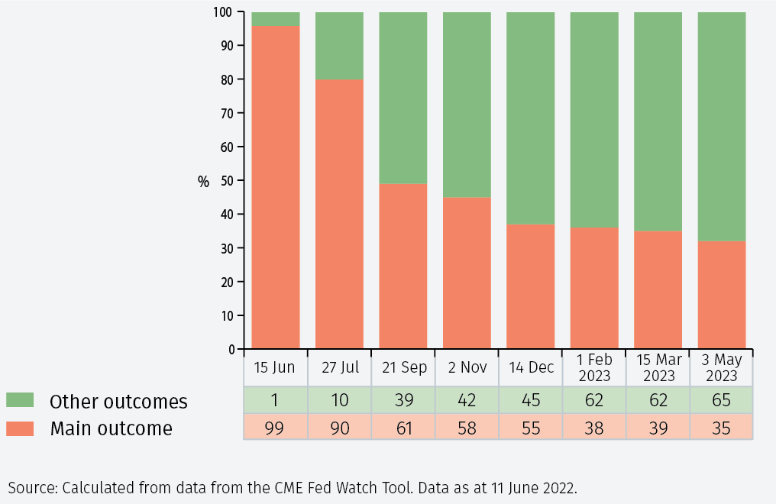

To understand better how much uncertainty market participants perceive, Figure 3 shows the probability attached to the Fed setting the interest rate priced in by the market and the probability of it setting another interest rate.

While market participants feel certain about the outcome at the June and July meetings this is not the case further in the future. For the September, November and December meetings they view the interest rates priced in as only marginally more likely to be right than wrong. And for the meetings in February, March and May 2023, they think they are much more likely to be wrong than right.

Probabilities

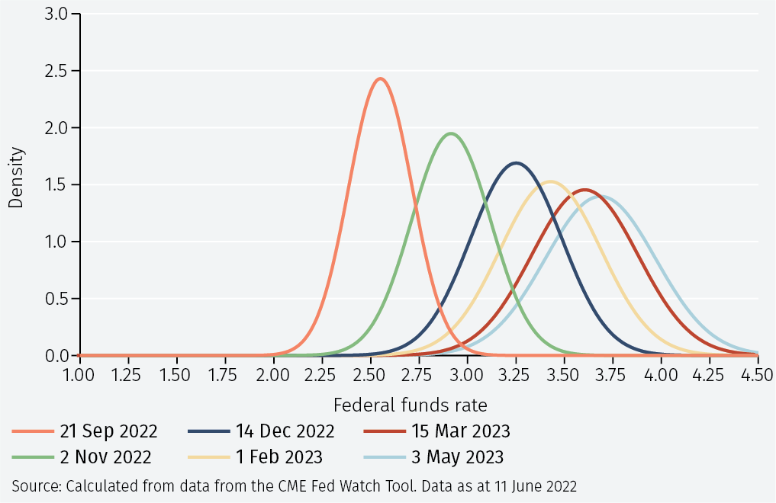

Another way to illustrate the uncertainty is to compute the probability distribution for the federal funds rate at the different Fed meetings as perceived by market participants. The estimated probability distributions, which disregard the June and July meetings for which market participants have very firm views, shown in Figure 4 are instructive.

They show that investors view interest rates anywhere between 2.25% and 2.75% are plausible for the September meeting, as are interest rates between 2.5% and 3.25% for the November meeting. For the December meeting, interest rates between 2.75% to 3.75% are likely. For the May 2023 meetings, they view interest rates between 3% and 4.25% as possible. These are very wide ranges.

Conclusions

The main conclusion from this analysis is that there is marked uncertainty about what interest rates the Fed will set over the coming year, except for the next two meetings. Indeed, investors think that the interest rate scenario priced in for the autumn is almost as likely to be wrong as right and that the interest rate scenarios priced in for the spring of 2023 are twice as likely to be wrong as right. While these results pertain to the Fed, similar uncertainty is likely to apply to the outlook for interest rates for other central banks.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.