- Date:

Insight - Although Covid concerns will feature in the first part of the year, we are generally optimistic about the outlook for global economic growth in 2022. With inflation rates set to fall back, the economic backdrop remains generally benign.

OVERVIEW

Although Covid concerns will feature in the first part of the year, we are generally optimistic about the outlook for global economic growth in 2022. With inflation rates set to fall back, the economic backdrop remains generally benign.

Global fourth wave

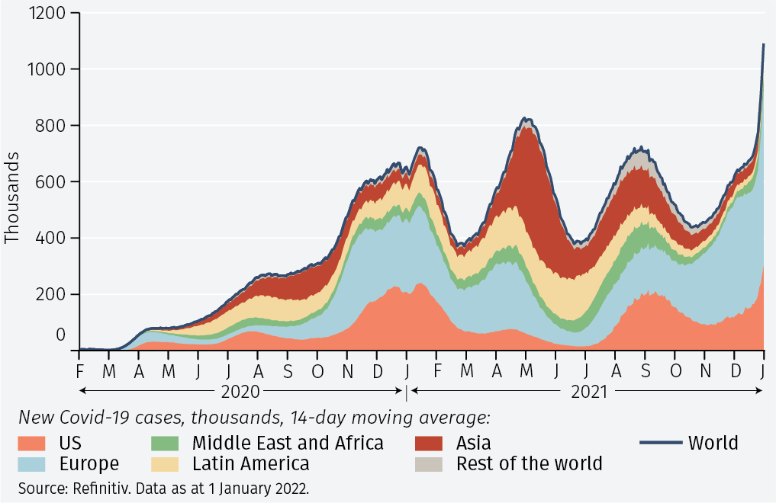

In early 2022 the predominant global concern is likely, once again, to be a surge in Covid cases – the fourth such wave (see Figure 1). Global economic growth was already hit towards the end of 2021 as the Omicron variant spread, some restrictions on movement were imposed and consumer sentiment was adversely affected. However, the impact varied widely from country to country. Europe was the hardest hit of the advanced economies. US economic growth, in contrast, seems to have remained relatively firm.1

To some extent the world economy has grown accustomed to dealing with Covid. Global economic growth slowed very sharply in the first wave from March 2020 onwards but has been more resilient in subsequent outbreaks. The potential for a recovery later in 2022 remains and we see overall GDP growth at around 4.5% for the advanced economies and slightly faster than that in the emerging economies.

Savings and spending

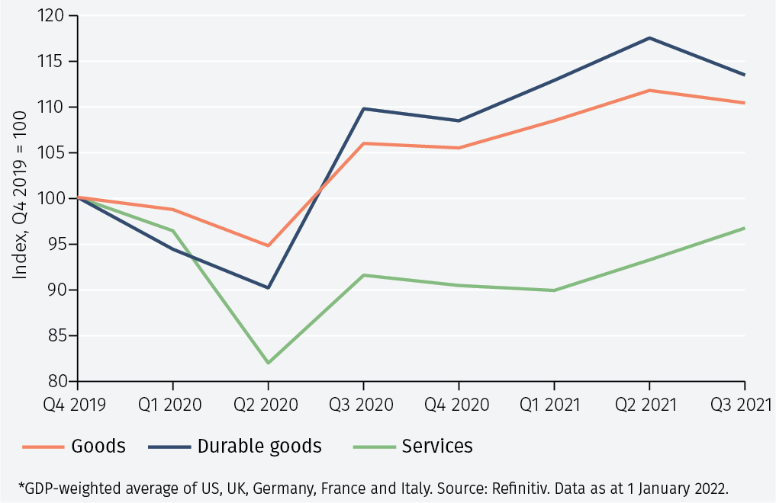

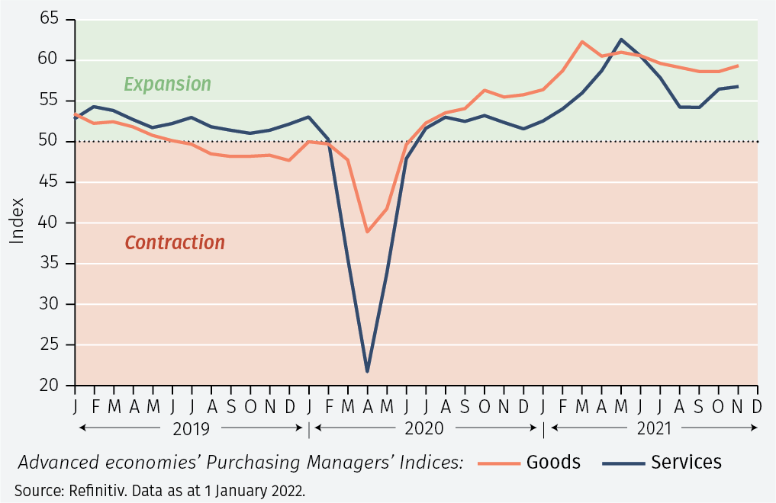

That assessment is based on three expected developments. First, we see a recovery in consumer spending on services such as entertainment, travel and live events. Across the main advanced economies, the latest data (to the third quarter of 2021) show such spending still below its pre-pandemic level (see Figure 2). Consumers have the ability to spend, given the household savings that have been accumulated during the pandemic and the increase in wealth due to asset price increases. In the US, for example, the net worth of households was USD 144.7 trillion at the end of the third quarter of 2021, almost 25% higher than immediately before the pandemic. The extent to which this translates into higher spending depends, of course, on consumer confidence and the willingness to spend. Survey data from purchasing managers showed some improvement in the services sector before the spread of Omicron (see Figure 3) suggesting that such spending was already starting to recover. It remains to be seen how resilient this proves to be, but we are optimistic. Consumers and many businesses have, to a considerable extent, learned to live with Covid; we expect an increase in vaccination rates in countries that have lagged behind; the roll-out of new therapies, in particular a Covid pill, are likely in 2022.

Second, we expect an easing of supply chain pressures, allowing pent-up demand for some goods to be satisfied and inventories to be rebuilt. The car and consumer electronics industries are two areas where such pressures have been most intense.

Third, the need for green infrastructure spending is substantial. To meet the objective of net zero carbon emissions by 2050, such spending is estimated at USD 4 trillion per year for the next quarter century, USD 100 trillion in total. The fact that government bond yields, in both nominal and real terms, remain so low suggests that there is still a global savings glut which can be deployed to meet these infrastructure spending needs.

Low government bond yields and secular stagnation

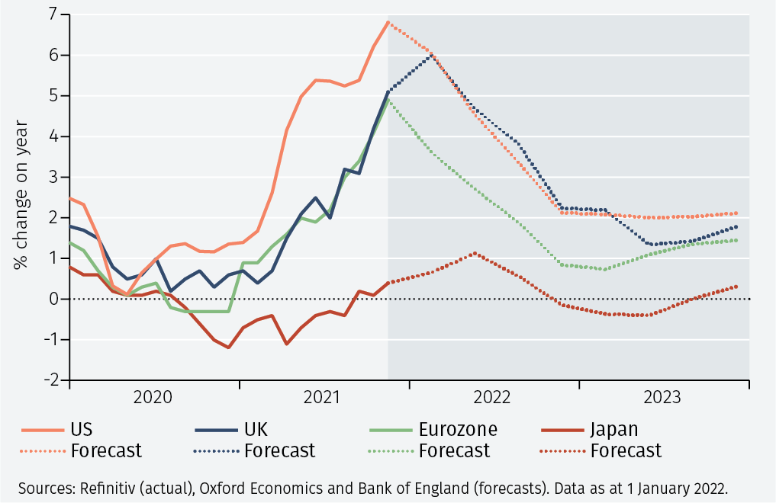

Bond yields also indicate to us that inflation rates are not expected to remain high. Peak inflation rates are set to be reported in the first quarter, with rates then falling back towards 2% (see Figure 4).

Very long-term government bond yields, such as the US Treasury 30-year yield, which cannot be explained by inflation trends over just a year or two, have trended lower over a number of years (see Figure 5). This can be taken not just as an indication of a global savings glut but also of secular deflationary forces. If that is the correct interpretation then after the recovery in 2021 and 2022, global growth can be expected to revert to its pre-pandemic relatively slow rate (2% or less for the main advanced economies).

Globalisation and the emerging economies

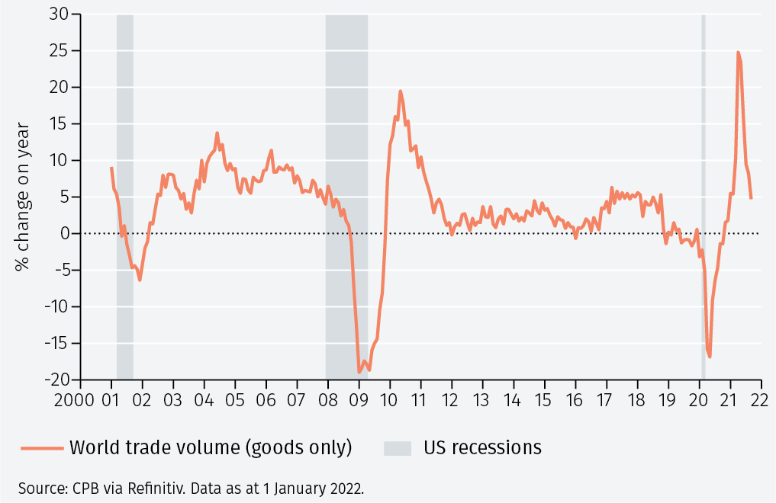

Two other big longer-term questions about the global economy are also pertinent. First, whether globalisation is under threat, especially as a result of the trend to reshore production. Our view is that there are limits to the extent this can take place, particularly because of a lack of skilled labour in those countries seeking to reshore (see Special Focus, page 11) and the complex nature of global supply chains. Global trade in goods is likely, we think, to continue to grow at a rate similar to that seen in the period 2012-2019 (see Figure 6), with potential for faster growth in services.

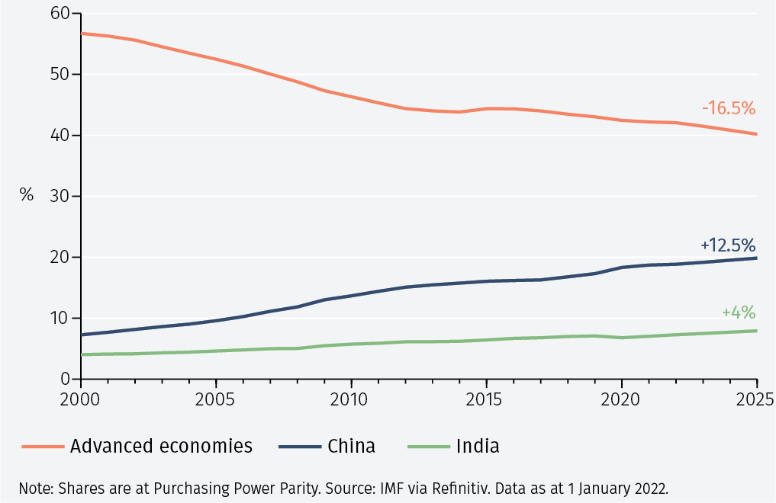

Second, whether the importance of the emerging economies in driving global growth will continue. In practice, only two emerging economies – India and China – have accounted for all the decline in the advanced economies’ share of global GDP since 2000 (see Figure 7). We are optimistic that other emerging economies, propelled by the adoption of digital technologies, can now catch up.

To continue reading, please use the button below to download the full article.

Footnotes

1 The Federal Reserve Bank of Atlanta’s 4 January 2022 GDPNow forecast is for 7.4% annualised growth in Q4 2021. https://www.frbatlanta.org/cqer/research/gdpnow

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.