- Date:

Inview March 2021

Editorial

Welcome to the March edition of Inview: Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

The news at the end of 2020 that several successful vaccines against Covid-19 had been developed led to a sea change in market sentiment. Since then, it has gradually become clear that vaccinating large parts of the population across the globe is a massively demanding task. With vaccination campaigns progressing unevenly across countries, investors are increasingly wondering whether there is a risk that the expected recovery in 2021 will be weaker and less synchronised than initially thought. A related concern arises from the fact that the virus mutates, leading to new versions that may be more contagious or more dangerous. It is notable that the vaccination campaign in the UK, where one of the most contagious variants originated, is the most advanced among developed countries.

Another factor impacting markets the outlook for inflation. With the US engaging in massive fiscal stimulus and with global liquidity being plentiful after years of expansion following the global financial crisis in 2008-9, some market participants are increasingly wondering how big the risks to price stability are. Inflation rates fell sharply during the first four months of 2020 as a result of Covid. With these data points now dropping out of the calculations, inflation will be rising in many countries in early 2021, boosting concerns about inflation.

In turn, an unexpected, sharp rise in inflation would almost surely lead central banks to signal that they stand ready to tighten monetary policy, if that becomes necessary. Of course, Chairman Powell has repeatedly made clear that the Federal Reserve is nowhere near starting to think about tightening monetary policy. However, the markets have a long memory and recall all too well that the FOMC expected in March 2019 to continue to raise interest rates gradually, even though markets were pricing in, correctly, a change in direction in US monetary policy from late 2018 onwards.

The increased concern about inflation and the related rise in bond yields have contributed to a pause in the equity market rally. That is not at all surprising after the strong performance displayed immediately following the US presidential election. Moreover, February is historically a tough month for equity markets, historically showing the second weakest average returns of the year after October. However, the underlying factors supporting equity markets remain in place, as shown by the strong earnings reported by listed companies in the last quarter of 2020 and the solid guidance projected for 2021.

In our view, portfolio allocation should maintain a slight overweight in equities over fixed income, with a preference for value stocks and medium and small capitalisations. Within fixed income, government bond yields remain unattractive despite the recent rise, although long-dated inflation protected bonds offer a good hedge against both the risk of inflation and of increased volatility. Gold prices have fallen further in the last few weeks and offer another option for hedging portfolio returns if risk aversion were to rise again.

Global Asset Allocation: Summary

Equities

- We have considered moving towards an overweight in Europe, but momentum is not yet strong enough. US equities would be the obvious candidate to downgrade to finance that move. However, we will wait for any market pull back to add to European equities and potentially to increase our overall equity overweight.

- Some profits are being taken in smaller US companies following their recent strength relative to large caps. We are looking to add to value and large cap growth at this point, continuing to hold our US overweight for now.

- Japan is one of our preferred areas but there has been a clear leadership flip more recently to value companies. We would not necessarily chase this move, but it does warrant a more balanced profile going forward.

- Brazilian equities have been under pressure recently, following the ousting of the CEO of Petrobras by President Bolsonaro and this has created additional uncertainty. Latin American equities remain one of our underweight areas.

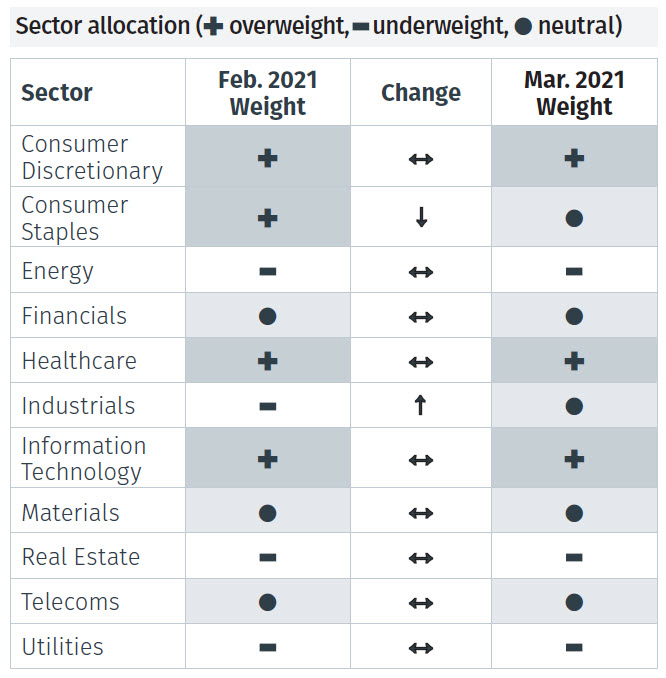

- This month we are upgrading industrials to a neutral position as the sector is now showing relative momentum. Meanwhile consumer staples are downgraded to neutral having lost their uptrend.

Fixed Income

- Fixed income positioning is underweight although we note that diversification is key, highlighting the need to be allocated across emerging markets, convertibles, investment grade, high yield, TIPS and mortgage backed securities.

- We have seen a recent sell off in government bonds although we are not concerned by inflation worries, noting that much of the increase in commodity prices is transitory (i.e. base effects). The yield curve steepening is a sign of reflation and we continue to be underweight.

- While our high yield debt positioning may have been too cautious over the last three-months given very tight spreads and US yields at all time lows, in the low rate environment we maintain a neutral position.

- In emerging market debt coupons are attractive both in hard and local currency bonds relative to zero rates, with selectivity being key.

Alternative Investments

- We are growing more constructive on infrastructure, tactically upgrading it to neutral to provide an interesting alternative to fixed income as the global recovery picks up.

- Hedge funds should also be considered as a good alternative to fixed income allocation as a diversifier of alpha.

- We remain cautious on oil and see recent price spikes from cold weather in the US and vaccine optimism as an over-valuation relative to fundamentals.

Currencies

- Having previously tactically upgraded the UK pound to overweight, this month we are taking it back to neutral. This is because we believe the short-term benefits around the economic recovery have been priced in. We will continue to monitor currency moves as more data comes through.

- Our PPP-based exchange rate models show a convergence of the US dollar to an equilibrium with the pound and the euro.

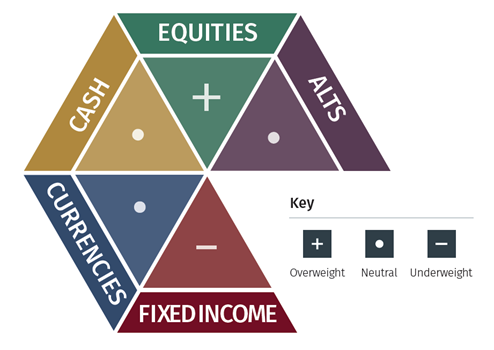

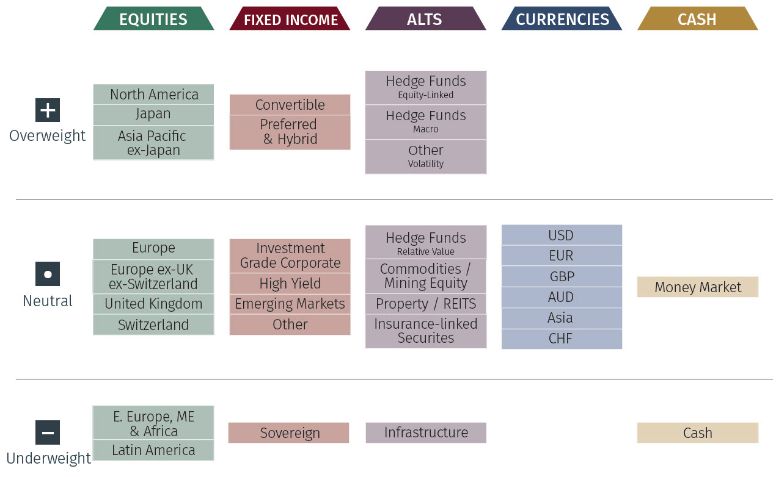

Global Asset Allocation: 12-Month Strategic Outlook

Based on a balanced mandate, the matrix below shows our long-term house view on investment strategy.

Overall Asset Allocation Views

Asset Class Breadown

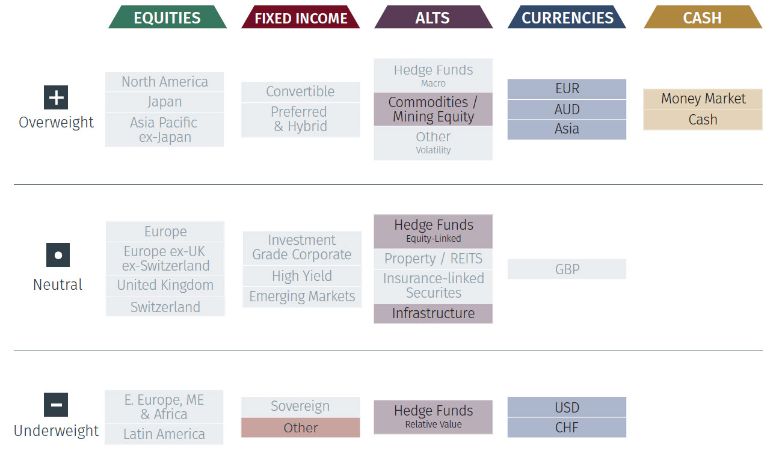

Global Asset Allocation: 3-Month Tactical Outlook

Based on a balanced mandate, the matrix below shows our short-term house view on investment strategy.

Note: The highlighted boxes indicate a difference from our 12-month strategic outlook.

Asset Class Breakdown

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.

ASSET ALLOCATION GRIDS

Please use the button below to download the full article to see asset allocation grids.