- Date:

Global house view & investment perspectives

Editorial

Welcome to the November edition of Inview: Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

A major influence has been the US elections and the perceived implications for the economy. President Trump’s failure to win re-election is a good sign in that it makes US policy more predictable. It is also likely to lead to smoother diplomatic relations with the US’ international partners, which will help reduce risk premia, particularly for European and emerging market assets. It reduces the risk of trade disagreements between the US and Europe and increases the likelihood the dispute settlement system of the WTO will be restored, lowering trade tensions. While disputes about Chinese trade practices will remain, the US should refrain from unilateral actions and instead seek alliances with its partners.

Since the Senate will most likely remain with a Republican majority, Biden will not be able to introduce sweeping changes to economic policy. While it is probable that the US will engage in a fiscal expansion to mitigate the effects of Covid, this is likely to be smaller than if the Democrats had won a majority in the Senate. Similarly, while the new administration may seek to raise taxes, it is unlikely that they will be able to completely undo President Trump’s 2017 tax cuts.

Furthermore, Biden is likely to reappoint Fed Chairman Powell when his term ends in 2022, promoting continuity and predictability of US monetary policy.

A second major development has been the announcement that a Covid vaccine will most likely be ready for use before the end of the year. While it will take several months before enough doses are available for a broad public vaccination campaign, it suggests that the Covid pandemic will be brought under control in much of the world in 2021. Meanwhile, the focus will remain on controlling the virus, if necessary, by further imposing strict lockdowns as have been announced by several European countries recently.

A third factor has been the approaching deadline for a Brexit deal. The talks have remained difficult although clarity about the outcome of the US presidential election may help achieve progress. While a deal is more likely than not, it is clear that the trade regime between the EU and UK will change fundamentally on January 1st. For example, services may well not be part of any deal and the service sector is an important component of the UK economy. The UK economy will therefore feel the repercussions more than continental Europe.

The “Goldilocks” political outcome of the US elections and progress on a Covid vaccine warrant an overweight in risky assets. Over the medium term, it is conceivable to expect the performance gap of the last few years to narrow between non-US and US markets, with the markets of Asia and Europe likely to be preferred. In the context of low yields and policy reflation in developed markets, emerging market bonds in hard currency look attractive, as do convertible bonds and hybrids. Gold is also poised to benefit from the extended policy accommodation and the prospect of a weaker US dollar.

Global Asset Allocation: Summary

Equities

- We remain marginally overweight to equities. With cash levels also elevated, election related volatility could provide opportunities to deploy some cash before year-end.

- Despite the Republicans retaining control of the Senate, we expect further fiscal stimulus to be agreed by year-end. With good 2021 growth expectations, confidence in a vaccine and seasonality we see any dip as a buying opportunity for US equities.

- A resurgence in European virus cases has reduced growth expectations, but quick lockdowns will give way to proactive opening. We hold a neutral position in European equities, remaining cautious on value investments.

- Although UK equities have been some of the weakest performers year-to-date we maintain our neutral positioning.

- Stock selection in Japan has been quite critical with growth names continuing to perform very well in this environment. We are tactically neutral on Japan but more positive on the longer term prospects.

- A second covid wave has kept oil prices compressed and they face a long path to recovery. Given the economic influence of oil in many Latin American countries and those in EMEA, we remain cautious on these regions.

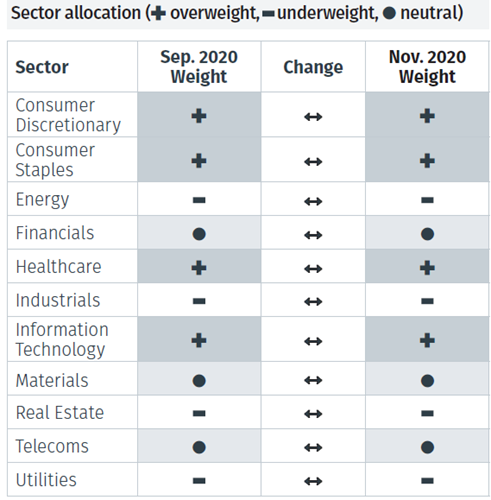

- No sector changes were made this month, although we note that many sectors are in an up-trend. Basic materials continues to show relative momentum so we are positively inclined to the sector.

Fixed Income

- We upgraded hybrid debt and CoCos to overweight on both a tactical and strategic basis, due to low valuations relative to traditional high yield.

- Investment grade bonds are being downgraded to neutral to reflect the greater sensitivity to rates. Interest rate impacts will have a greater effect in the AA to A space given that spreads have tightened substantially but we still favour longer-dated bonds in the BBB area.

- Within sovereign bonds we would caution against overly long duration positions at least until yields are higher and the yield curve has steepened to new cycle highs.

Alternative Investments

- Our call to upgrade industrial metals a few months ago has worked well as prices have picked up and leading indicators have shown signs of improvement.

- Oil prices are recovering but it will likely take a while for them to move back into their historic range. Given high oil inventory levels, we hold an underweight view but if prices continue their recovery we could look to add to exposure.

- We remain underweight on infrastructure as budgets will be constrained and liquidity is poor. However, once there is greater evidence of sustained economic recovery, infrastructure could be an interesting alternative to some fixed income plays.

Currencies

- Our only currency change for the month is a tactical upgrade of the pound to neutral. We are getting increasingly confident of a Brexit deal as the UK government realises that a bad deal at this time will further exacerbate the slowdown.

- Election volatility and the second wave of covid infections mean a more cautious stance in the short-term for the euro and we look to the longer-term moving averages for support.

- Tactically the US dollar and Swiss franc are our least preferred currencies. Our currency models suggest that there is still space for the US dollar to weaken going forward, while the franc could weaken if market volatility abates.

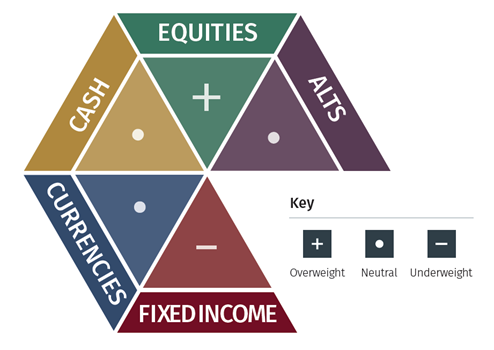

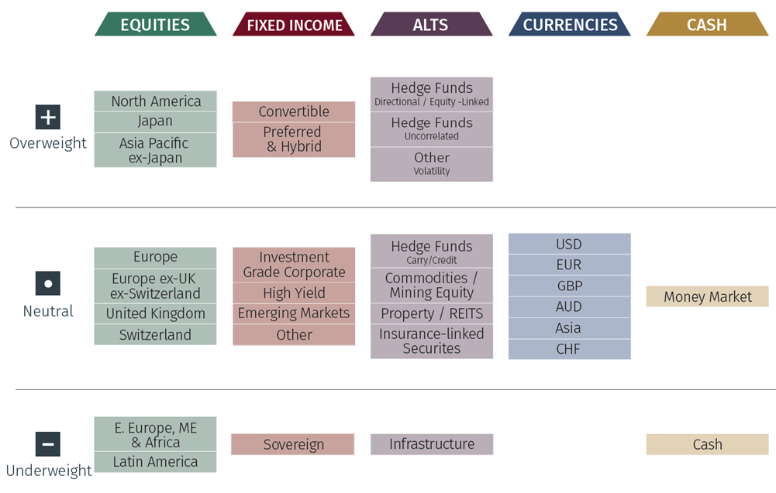

Global Asset Allocation: 12-Month Strategic Outlook

Based on a balanced mandate, the matrix below shows our long-term house view on investment strategy.

Overall Asset Allocation Views

Asset Class Breadown

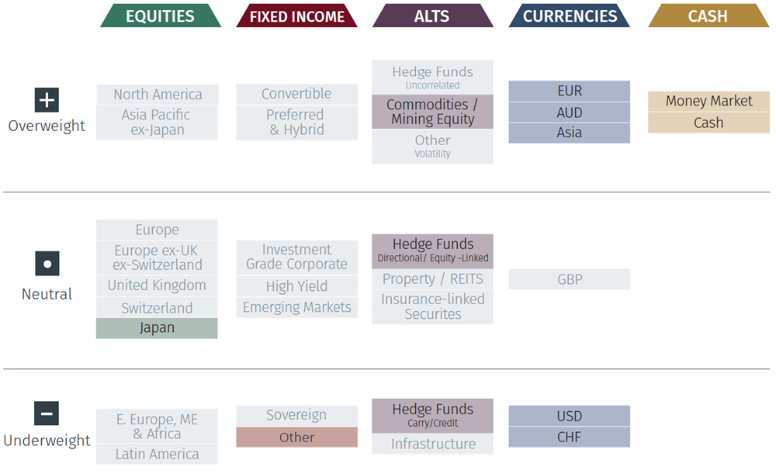

Global Asset Allocation: 3-Month Tactical Outlook

Based on a balanced mandate, the matrix below shows our short-term house view on investment strategy.

Note: The highlighted boxes indicate a difference from our 12-month strategic outlook.

Asset Class Breakdown

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.

ASSET ALLOCATION GRIDS

Please use the button below to download the full article to see asset allocation grids.