- Date:

Inview - In this publication we consider

significant developments in the world’s markets,

and discuss our key convictions and themes for

the coming months.

Editorial

Welcome to the December edition of Inview: Monthly Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

After a long negative phase, financial markets seem to have found their footing again. Even if the scenario remains characterised by a high degree of uncertainty, several elements appear to have finally aligned in favour of a recovery in financial asset prices.

The most important factor remains inflation. It is therefore encouraging that, at least in the US, data has shown a slowdown in recent months, reinforcing the feeling that the peak is behind us. Furthermore, some moderation in wages has been added to the drop in the prices of raw materials, freight rates, and real estate and it is only a matter of time before these translate into a more evident drop in inflation. In Europe, the price of natural gas has dropped significantly since the summer peak, but the risks of a new surge linked to the developments of the war in Ukraine have not completely vanished. Therefore, it remains to be seen how quickly European inflation will moderate from the record levels set recently.

Growth is losing momentum in the US and Europe and even central banks acknowledge the increased risk of a recession in the coming quarters. Although the need to further tighten monetary policy still prevails, the time for central banks to pivot towards a less aggressive stance is drawing closer.

Finally, although it is difficult to anticipate the exact timing, several elements indicate that China is preparing to ease anti-Covid restrictions. For this reason, the world's second largest economy is likely to regain momentum during 2023, making the global economic cycle asynchronous.

The equity markets have reacted to the favourable signals and recovered strongly in recent weeks approaching important technical levels. Bond prices have also risen but yields remain relatively attractive amid slowing growth and inflation. Therefore, it seems advisable to trim the overweight in equities to increase exposure to fixed income securities, in particular highly rated corporate bonds.

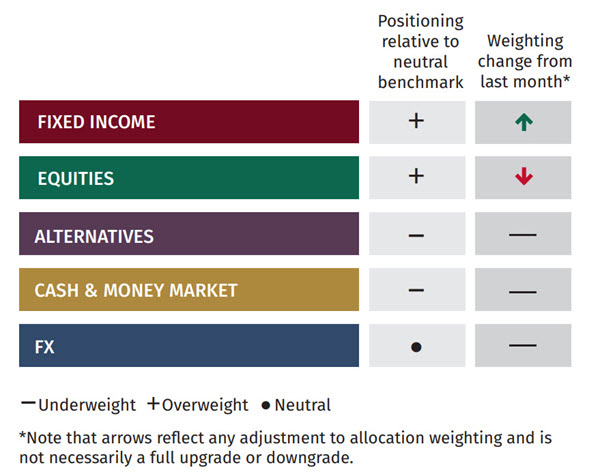

Asset Allocation

Global Allocation

Based on a balanced mandate, the matrix below shows our 6-12 month view on investment strategy

Fixed Income

We are increasing the allocation to fixed income by 2%, taking it marginally above the benchmark neutral position. This is supported by the continuous evidence of a moderation in inflation as well as the deterioration in the outlook for economic growth ahead of the first quarter of 2023.

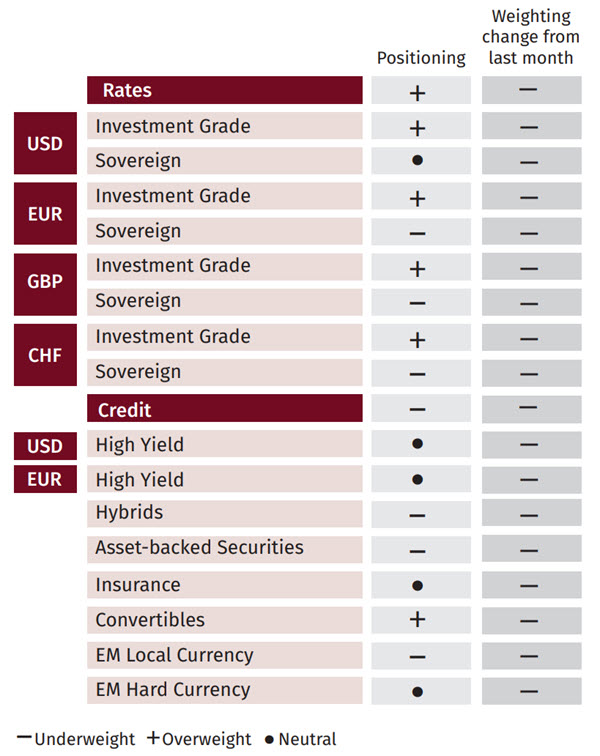

The steep inversion of the US yield curve, marked by the difference between yields on the 10-year Treasury bond and the 3-month note, anticipate a US recession in the next 6-12 months. Spreads in investment grade credit are currently close to the top quartile relative to history. Therefore, we maintain a strong preference for this asset class given attractive yield levels and historical low default rates during periods of economic deceleration.

However, given the recent rally in yields, there is potential to gradually increase the tactical exposure to high yield in the coming months. Additionally, given the weakening of the US dollar, it could soon become attractive to start building a position within emerging markets debt denominated in local currency, where we are currently underweight.

Equities

The previous month we increased our allocation into equities above the neutral benchmark, seeing a short-term tactical rally. With the recent strength in equity markets this call had a positive impact in November. While market momentum continues to be positive, given the strength in the rally we see it as prudent to reduce our equity allocation by 2%, remaining marginally overweight versus the neutral allocation. We expect market sentiment will remain tied to the upcoming central bank meetings in the US, Europe, UK and Switzerland, where more clarity is expected of further direction of monetary policy globally. Key data releases on inflation and unemployment will contribute to uncertainty in the month ahead. Therefore, we remain vigilant of market volatility which could drive intramonth allocation changes, if deemed appropriate.

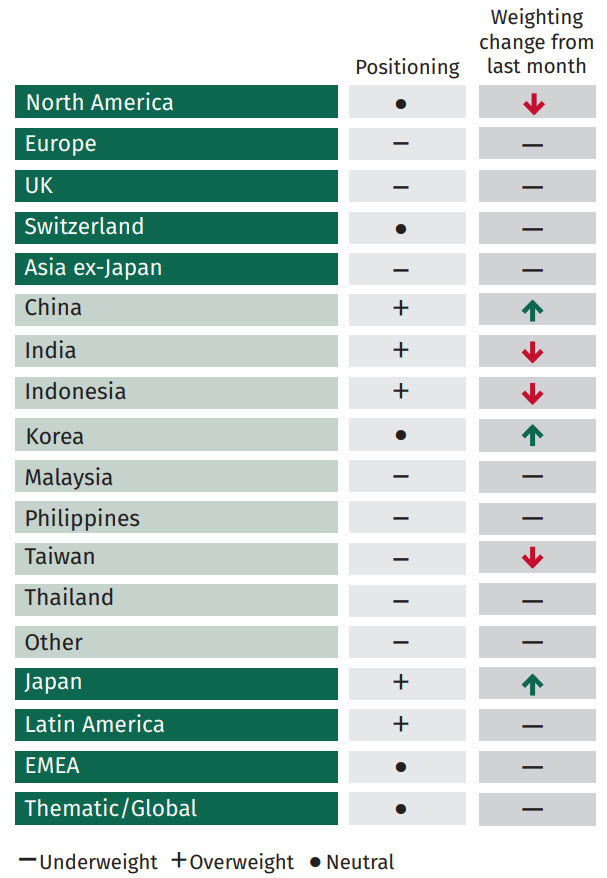

From a regional point of view, we have maintained our underweight positioning in UK and European equities. We believe these two economies are already in, or close to, a recession which could extend into next year. However, European data has been more resilient than previously anticipated, prompting some minor changes in sector positioning. No major adjustments were made to our regional equity allocations this month.

Technical indicators reveal that most sectors in the US are in an uptrend, supporting the recent rally in equity markets. Although we have marginally reduced our US allocation, we maintain a positive view in sectors such as Information Technology and Consumer Discretionary, which we believe could be a sector to follow in the new year. Japan continues to have an above-benchmark allocation, based on the strong outlook for corporate earnings. Within Asia ex-Japan, we are now turning more optimistic on China where the reopening is now a consideration, and government policies appears to be prioritising growth.

Equity Sector Views

UK

Within the UK industrials is our largest sector overweight, taking advantage of the de-rating seen across the sector this year to pick up quality companies. We continue to hold a bias towards defensive compounders over more cyclical industrials for now. Energy is also a preferred sector as we continue to see support for energy prices remaining, particularly as economies begin to re-accelerate, China reopens, and demand for aviation fuel recovers to pre-pandemic levels. There is more caution on consumer staples as we expect them to be tested as consumer purchasing behaviour changes, downtrading increases, and volumes weaken.

US

We remain vigilant on the macro backdrop and therefore risks to corporate earnings. Therefore, an overweight in defensive sectors is held, including healthcare and consumer staples. Within cyclical sectors, we are overweight in consumer discretionary. US consumers are still holding up thanks to pandemic savings, low unemployment rates and limited energy price shocks compared to Europe.

We are also overweight technology – due to our quality growth bias and the concentration of such stocks within the sector.

Asia ex Japan

Within China, there is a bias to re-opening plays such as travel, hotels and general consumer discretionary. We remain defensively positioned with overweights in healthcare and staples given current weak demand trends ex India/Indonesia. There is a property underweight, largely China property as we believe home sales will remain weak and will take long time to recover from improved financing support.

Europe

Technology has moved to our biggest overweight in Europe. Up to the end of third quarter the sector had performed very poorly and overall market positioning has been very underweight. Coupled with the recent move down in European bond yields, we see it as a good time to be adding exposure. Within industrials we have added to capital goods but we remain overweight. We maintain our cautious stance on consumer discretionary and staples given many companies are in the eye of the ‘cost of living’ storm. Therefore, we have marginally reduced our exposure to consumer stocks, taking profits from Consumer Discretionary, Consumer Staples and Healthcare.

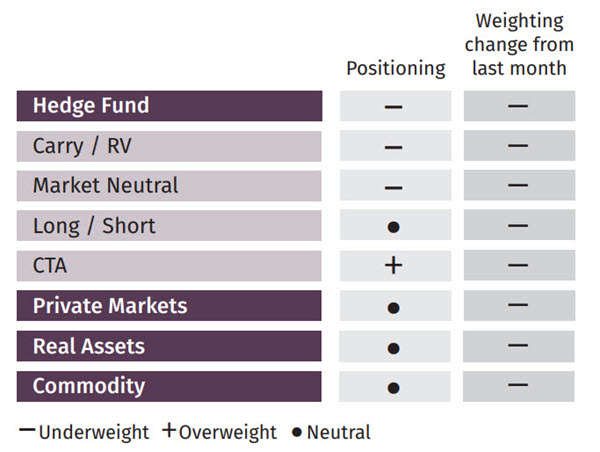

Alternatives

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.