- Date:

- Author:

- GianLuigi Mandruzzato

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

The Swiss National Bank raised rates by 0.75% in September, ending the era of negative policy rates. In this Macro Flash Note, GianLuigi Mandruzzato explains why the move was dovish.

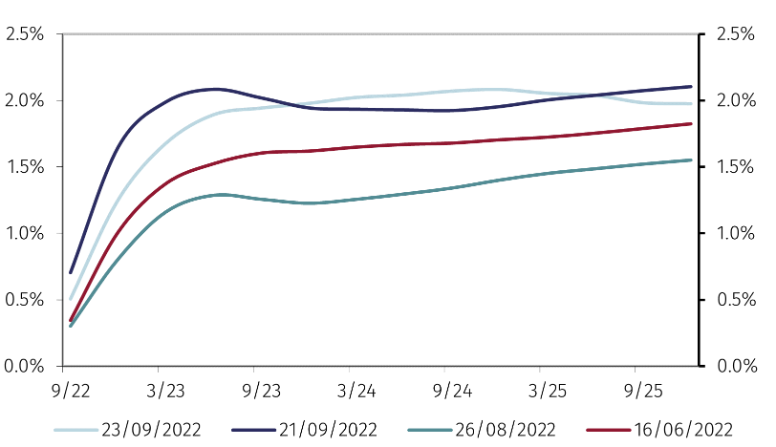

Despite raising rates by an unprecedented 0.75% to 0.5%, the Swiss National Bank (SNB) sent a surprisingly dovish signal to markets. While other central banks, including the US Federal Reserve and the European Central Bank, are keen to indicate that they will continue to increase rates forcefully to counter high inflation, the SNB only reiterated that further rate increases “cannot be ruled out”. Hence, although another rate increase before the end of 2022 remains possible, it is not certain that it will happen and that it will be by another 0.75% as markets expect (see Figure 1).

Source: Refinitiv and EFGAM calculations as at 23 September 2022.

In fact, the SNB set a high bar for new, aggressive rate increases. The new SNB conditional forecast sees quarterly inflation at 3.4% year-on-year until the first quarter of 2023. Inflation is then expected to decline to 1.6% in early 2024 before rising again towards 2% in mid-2025. So, unless inflation exceeds the short-term forecasts, the SNB could conclude at its December meeting that the policy rate needs only a small increase to ensure that inflation falls back and stays within the 0-2% target range in the medium term.

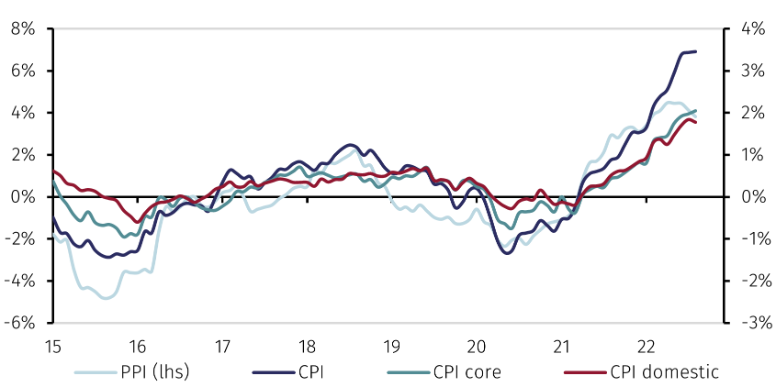

Potential SNB caution rests on good reasons. As explained in the monetary policy assessment, current high inflation mainly reflects exogenous shocks to energy and food prices that are beyond the influence monetary policy. With the increase in interest rates, the SNB aims to prevent the spread of inflationary pressures to other goods and services. It is encouraging that Swiss producer price inflation has recently declined because of weaker commodity prices (see Figure 2). If these trends persist, the high correlation between Swiss producer and consumer prices suggests that CPI inflation will fall in 2023.1

Source: Refinitiv and EFGAM calculations as at 23 September 2022.

Furthermore, the SNB noted that the global economy has slowed “considerably”, representing a downside risk to growth in a small open economy like Switzerland (see Figure 3). The downside risks to growth are exacerbated by the preannounced policy tightening by central banks around the globe.

Source: Refinitiv and EFGAM calculations as at 23 September 2022.

In addition, weaker global demand will help to ease supply chain bottlenecks that have pushed prices higher following the reopening of the global economy after the pandemic.

Finally, the strength of the Swiss franc supports the SNB’s cautious approach. Since mid-June, the trade weighted exchange rate of the franc has risen by more than 5% even after the selloff that followed last week decision. Furthermore, the fundamentals continue to support a rise of the Swiss franc vis-à-vis the other major currencies in the longer run, and that would help to contain inflation in Switzerland.

To conclude, markets expected the SNB to frontload its monetary policy normalisation in September given the expected tightening by other central banks before the next SNB meeting in December. The dovish surprise was best seen in the fall of the Swiss franc that followed the announcement, although it was short-lived at least against the euro. Markets continue to anticipate the SNB will raise rates by another 0.75% by the end of the year, but this is by no means certain.

As President Jordan noted in Jackson Hole, central banks should consider the risk of overtightening, potentially leading to the return of too low inflation, if not deflation.

1 Since 2000, the correlation between PPI and different measures of CPI is high and rises when PPI is lagged by up to 6 months, particularly in relation to core and domestic consumer prices. When sample is restricted to the period beyond 2015, the correlation rises to around 90% with all measures of consumer prices considered.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.