- Date:

- Author:

- Joaquin Thul

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

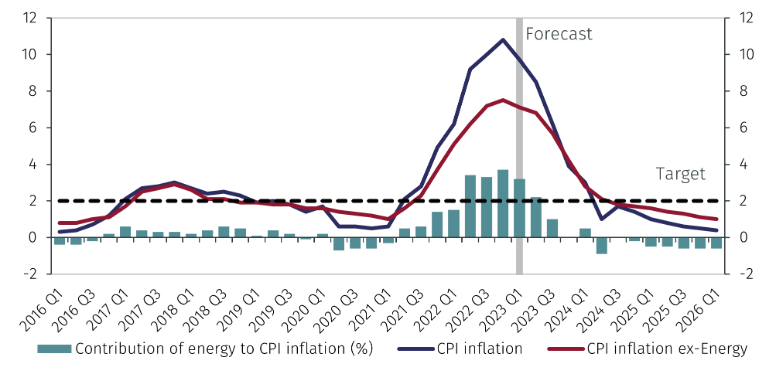

On 2 February the Bank of England’s Monetary Policy Committee (MPC) voted in favour of a 0.5% interest rate increase to 4.0%. This represented the tenth rate increase since December 2021 as the BoE continues to grapple with high levels of inflation. In the press conference after the meeting, BoE Governor Andrew Bailey stressed that the MPC believes it is still too soon to declare victory over inflation as it remains elevated at 10.5% year-on-year (yoy). However, markets believe the central bank is near the end of its tightening cycle.

The quarterly Monetary Policy Report highlighted that although global inflationary pressures remain elevated, they seem to have peaked in many developed economies, including in the United Kingdom. However, the BoE acknowledges that domestic inflation has remained stronger than expected due to persistent wage pressures. It projects CPI inflation to fall back sharply towards the end of 2023 to around 4% due to falling prices of energy and goods prices (see Chart 1).

The report emphasised that the recent rate increases will only impact the economy in the coming quarters. Markets currently anticipate another 0.5% rate hike, with Bank Rate now expected to peak at 4.5% in 2023Q3, that is, below the 5.25% peak expected in November 2022. Incoming data over the next month will be crucial in assessing how quickly inflationary pressures are receding and how much tighter monetary policy needs to be to return inflation to the 2% target.

Source: Bank of England and EFGAM. Data as of 02 February 2023.

One factor driving domestic inflation has been the strength of the labour market, as underlying wage pressures have been stronger than expected. The MPC noted that wage growth in the private sector, which represents around 80% of UK employment, has declined from a peak of 8.9% yoy in July 2022 to 7.2% yoy in November 2022. According to a BoE survey, average pay settlements are expected to slow to under 6% in 2023, driven by a decline in CPI inflation and easing conditions in the labour market as UK economic activity decelerates.

The UK has seen an increase in strikes since last year, with the government arguing that surrendering to wage pressures would worsen the country’s inflation problem. So far, Sunak’s government has been able to push back against union demands, but the latter are unlikely to recede anytime soon. Risks to the BoE’s inflation forecast will therefore remain skewed to the upside if wage growth pressures do not subside.

BoE Governor Andrew Bailey has been questioned in the past for not acting swiftly to contain inflation. Similarly, the perceived dovishness of the MPC reflected by two members voting to leave rates unchanged and the softer rhetoric against inflation compared to the Federal Reserve and the European Central Bank, was reflected in the weakening of sterling by over 1.5% against the US dollar on the day of the announcement.

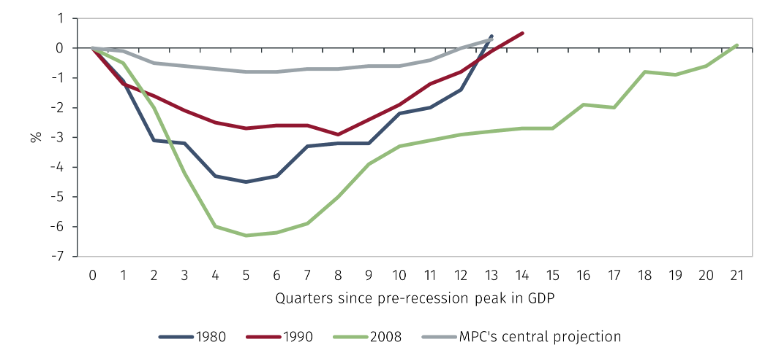

The BoE projects GDP to fall throughout 2023 and in the first quarter of 2024.1 Persistently high energy prices and the expected path of interest rates will weigh on consumer spending driving a decline in output of 0.7% in 2023 and very low but positive growth of 0.2% in 2024. Although the BoE expects the recession this year to be relatively mild, output is not expected to return to pre-pandemic levels until 2026.

Source: Bank of England and EFGAM. Data as of 02 February 2023.

The next actions of the MPC will remain dependent on inflation dynamics. The more dovish rhetoric on inflation from the BoE relative to other major central banks is aligned with market expectations, which also anticipate an end to the tightening cycle in coming quarters. Bond markets welcomed this outlook despite the persistent headwinds to UK growth, with the 10-year gilt yield falling on the day from 3.31% to 3.07% and the 2-year gilt falling from 3.42% to 3.22%. Risks to interest rates remain skewed to the upside, reflecting issues surrounding weak labour supply and the aftermath of Brexit, both of which continue to fuel wage growth, and the risk that the government concedes to some of the unions’ wage demands.

1 A technical recession is defined as at least two consecutive quarters of negative quarterly GDP growth.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.