- Date:

- Author:

- Joaquin Thul

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

The BoE surprised markets last week after the Monetary Policy Committee (MPC) voted, with a narrow majority of 5 votes to 4, to keep its policy rate unchanged at 5.25%. In this Macro Flash Note, Economist Joaquin Thul looks at the reasons behind the BoE’s decision and the outlook for interest rates.

In a surprise move, the Bank of England (BoE) left the policy rate unchanged at 5.25% at its meeting on 21 September, ending a cycle of 14 consecutive rate hikes. The MPC noted that recent indicators of inflation had been mixed. This justified keeping rates on hold to allow for past monetary policy tightening to fully impact the economy.

Source: Bank of England and EFGAM. Data as of 25 September 2023.

The MPC acknowledged that the 8.1% increase in average private sector weekly earnings in the three months to July was 0.8% higher than its August projections. However, this increase did not translate in other measures of UK wage inflation tracked by the BoE and it maintained the expectation that earnings growth will fall to 6% by the end of 2023.

Keeping rates on hold was justified by a recent deterioration in labour market data and a deceleration in economic activity during the last months. In July, the unemployment rate rose from 4.2% to 4.3% and the number of job vacancies fell to less than one million. GDP grew by only 0.2% quarter-on-quarter in Q2-23 and the BoE estimates of growth in the second half of the year have been downgraded.

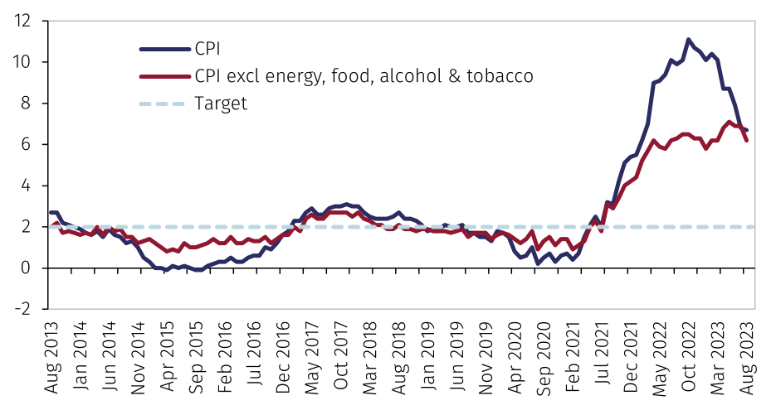

Headline CPI inflation declined slightly from 6.8% to 6.7% in August. Rising prices of motor fuel made the largest upward contribution to monthly inflation, but this was more than offset by the decline in services prices. Therefore, core inflation, excluding energy, food, alcohol, and tobacco, fell more than expected from 6.9% in July to 6.2% in August.

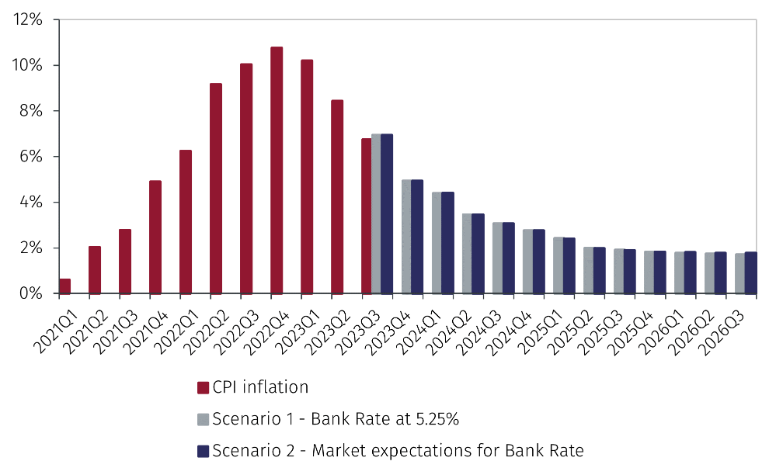

In the weeks before the MPC meeting, senior BoE officials, including Governor Andrew Bailey, Deputy Governor Ben Broadbent and Chief Economist Huw Pill, questioned the need for further rate increases. One argument supporting this view was that, according to the BoE’s models, the forecast path of inflation over the next three years was almost identical regardless of whether the MPC kept rates unchanged at 5.25% (scenario 1) or if they chose to follow market expectations of rates peaking at 6% in 2023 before falling to 4.5% in 2026 (scenario 2). The summary of the BoE’s inflation forecast under both these scenarios is presented in Chart 2.

Source: Bank of England and EFGAM. Data as of 25 September 2023.

The almost unnoticeable differences between these two scenarios supports the decision of keeping rates on hold and that the recent deterioration in data suggests that further rate hike would risk causing a recession.

In any case, the MPC statement does not rule out future rate hikes in future meetings suggesting that members believe risks to inflation remain tilted to the upside. Moreover, the BoE stressed that monetary policy would need to remain restrictive for a sufficiently long time to return inflation to the 2% target.

Source: LSEG Data & Analytics and EFGAM. Data as of 25 September 2023.

To conclude, the dovish tilt from the BoE at its last meeting surprised markets who were expecting another rate hike. Current market expectations see rates on hold until the first half of 2024, with a small probability for further rate hikes in a scenario of persistent inflation (see Chart 3). Overall, the BoE will focus on indicators of services price inflation, labour market strength and wage growth, all of which should slow if economic activity deteriorates in the remainder of 2023. For the time being, future BoE’s decision will be data dependent, not ruling out further policy tightening if required.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.