- Date:

- Author:

- GianLuigi Mandruzzato

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

At its meeting on 2 February, the ECB hiked by 50bps, maintaining a restrictive stance. Surprisingly, financial conditions eased during President Lagarde's press conference despite her signalling that there are more rate hikes to come. In this Macro Flash Note, GianLuigi Mandruzzato argues that what happened reflects a loss of the ECB’s credibility to markets.

The European Central Bank’s latest decision to raise interest rates by 0.5% was widely expected as was the indication that the bond portfolio will be reduced by EUR15bn per month from 1 March. Even the forewarning in the policy statement that rates will be raised again by 0.5% in March was already discounted by investors.

But the tone of the ECB statement and of President Lagarde during the press conference was hawkish. Lagarde emphasised that markets should note the ECB's determination to raise interest rates 'as much as necessary' to lower inflation to 2% in a timely manner.

Although not unanticipated, such a hawkish message would normally be expected to depress market sentiment as expected short-term interest rates and long-term government bond yields are adjusted higher. This would also usually result in a strengthening of the euro exchange rate but weigh on equity prices.

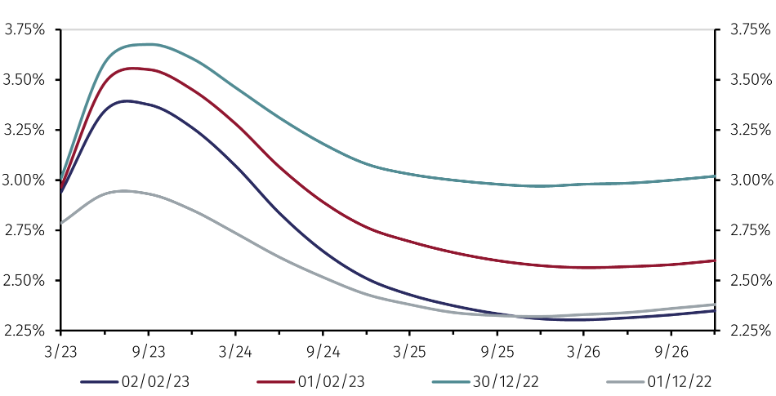

However, last week’s market reaction was the opposite. Futures contracts on short-term interest rates lowered by about 0.25% both the expected peak and the level at which rates are expected to settle in the medium term (see Chart 1). Government bond yields fell violently with German 10-year bonds falling by 20 bps and Italian yields by 40 bps. The rally in equity markets intensified and the EUR/USD exchange rate lost everything it had gained the day before after the Federal Reserve meeting.

Source: Refinitiv and EFGAM calculations. Data as of 02 February 2023.

One interpretation is that the market’s reaction reflects the ECB's loss of credibility due to inconsistencies in its recent communications. An example is the use of forward guidance, including at last week's meeting, accompanied by the statement that decisions will be 'data dependent' and taken 'meeting by meeting'. These messages are inconsistent and lead investors to give less weight to Lagarde's words.

Moreover, by her own admission, the ECB did not correctly anticipate the effects of the war in Ukraine and the energy price shock on eurozone growth and inflation, which explains the delay in raising interest rates. But now that energy prices, including natural gas and electricity, are falling rapidly, the ECB does not seem inclined to recognise the dampening effects on future inflation.

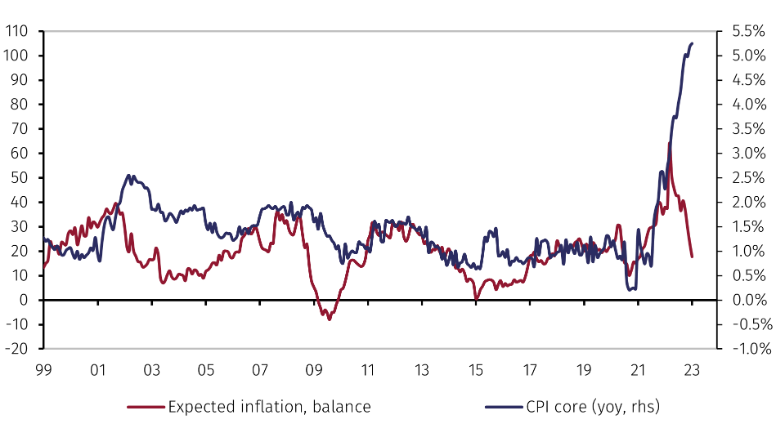

Another example concerns inflation expectations, the increase in which was identified as one of the factors behind the aggressive rate hikes in the latter part of 2022. Now that they are again consistent with inflation close to, if not below, the 2% objective, they are no longer taken much into account (see Chart 2).

Source: Refinitiv and EFGAM calculations. Data as of 02 February 2023.

These inconsistencies in the ECB's communications lead market participants to draw their own conclusions regarding the outlook for monetary policy based on incoming data. It is clear that the eurozone economy is slowing while the monetary tightening will only be fully felt from mid-2023.

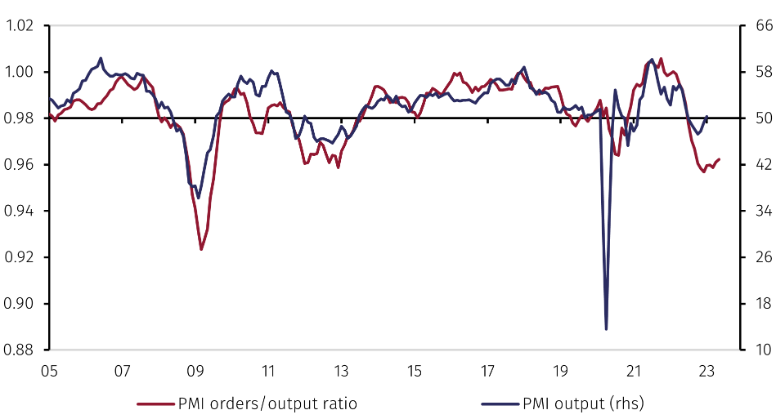

The January PMI survey, despite the Composite index moving back above the 50-threshold indicating expansion, highlights risks for growth in 2023. New and outstanding orders continue to decline, making a rapid rebound in growth unlikely (see Chart 3).

Source: Refinitiv and EFGAM calculations. Data as of 02 February 2023.

Moreover, the 2023Q1 ECB Bank Lending Survey shows that commercial banks are tightening access to credit to the private sector more intensely than after the start of the pandemic. This will lower both growth and inflation.

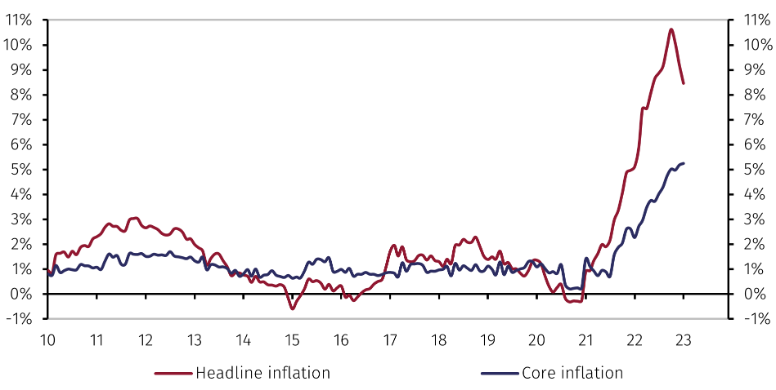

It is also true that inflation in the eurozone is falling much faster than the ECB predicted last December. In January, Eurostat's preliminary estimate put headline inflation at 8.5% year-on-year (yoy), down from 9.2% yoy in December, while core inflation stabilised at 5.2% yoy (see Chart 4).1 In December, the ECB forecast inflation to average 9.1% yoy in 2023Q1 and, as explained by President Lagarde after that meeting, it expected a temporary rebound in January.

Source: Refinitiv and EFGAM calculations. Data as of 02 February 2023.

Unsurprisingly, such marked forecast errors reduce the importance market participants place on the ECB’s guidance beyond perhaps the following meeting.

For longer horizons, investors assess the prospects for monetary policy based on incoming economic data. These point to a high probability of a further slowdown in growth and a more rapid decline in inflation towards the 2% objective than expected at the end of 2022.

This scenario requires neither steep interest rate increases nor a restrictive monetary policy for a prolonged period as anticipated by Lagarde. Rather, markets believe that this better-than-expected inflation scenario will lead the ECB to adopt a less restrictive policy stance than has been announced by President Lagarde. Paradoxically, by contradicting itself once again, the ECB could regain some of its lost credibility.

1 Among the main expenditure items, inflation in services slowed to 4.2% from 4.4% and in energy to 17.2% from 25.5%, while it accelerated in food to 14.1% from 13.8% and in other industrial goods to 6.9% from 6.4%. However, the figures may be revised when German data, the publication of which was delayed, will become available.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.