- Date:

Infocus - Inflation has surged to levels not seen in decades due to rising commodity prices, supply chain bottlenecks and tight labour markets. These factors apply to most developed countries, but not to Switzerland where inflation remains low. In this edition of Infocus, GianLuigi Mandruzzato compares Swiss inflation to that in the US and the eurozone and draws some policy implications.

The eurozone economy is in recession. The energy crisis and resulting high inflation have eroded private sector purchasing power and monetary policy tightening has further weighed on growth. While inflation is high, several factors suggest that it may soon decline sharply. In this edition of Infocus, GianLuigi Mandruzzato looks at the possibility that a deep eurozone recession leads to a quick fall in inflation.

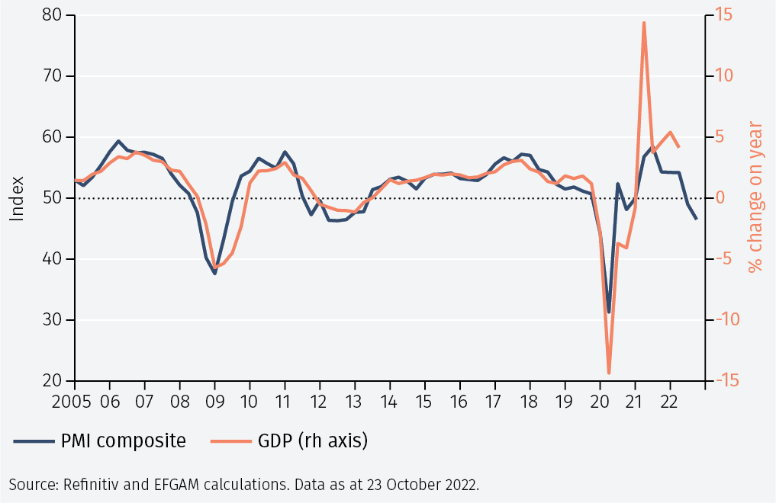

Having been surprisingly strong in the first part of the year, the eurozone economy probably fell into recession over the summer. Since July, the composite PMI index, which summarises activity in the manufacturing and services sectors, has remained below 50, the threshold that signals that economic output is contracting (see Figure 1).

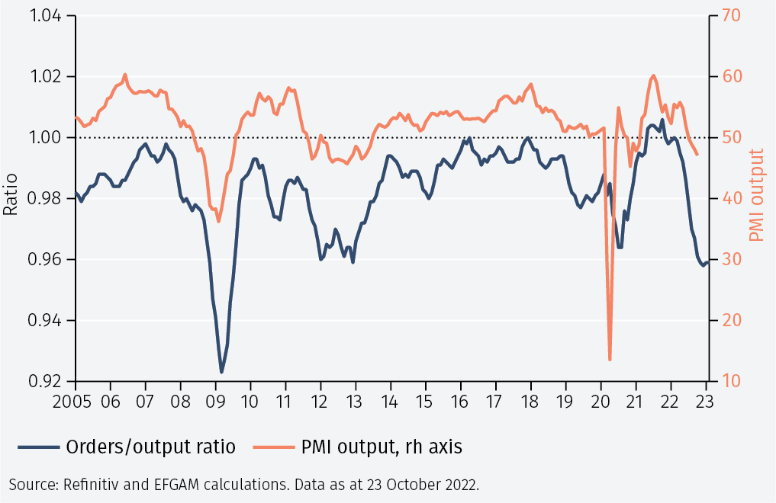

Although the composite PMI level is only slightly below 50, its trend up to October points to a deteriorating outlook (see Figure 2). New orders declined more than output, reflecting the energy crisis, the lockdowns in China and tightening financial conditions. The composite PMI could fall towards 40, a level recorded only after the collapse of Lehman Brothers in 2008 and during the covid pandemic. Overall, there is a high risk that GDP will drop significantly in 2022Q4 and that the contraction will also continue in early 2023, reducing next year’s GDP growth to around zero.

The risks to growth are evident when looking at household confidence. According to the EU Commission’s consumers’ survey, the willingness to buy durable goods is at the most depressed level since the series began in 1985, reflecting the impact of increased prices of basic goods and services on households’ purchasing power (see Figure 3). Furthermore, consumers fear a worsening of the labour market. Finally, the recovery in tourism after the ending of Covid restrictions is largely complete and will provide less stimulus to the economy than in the first part of 2022.

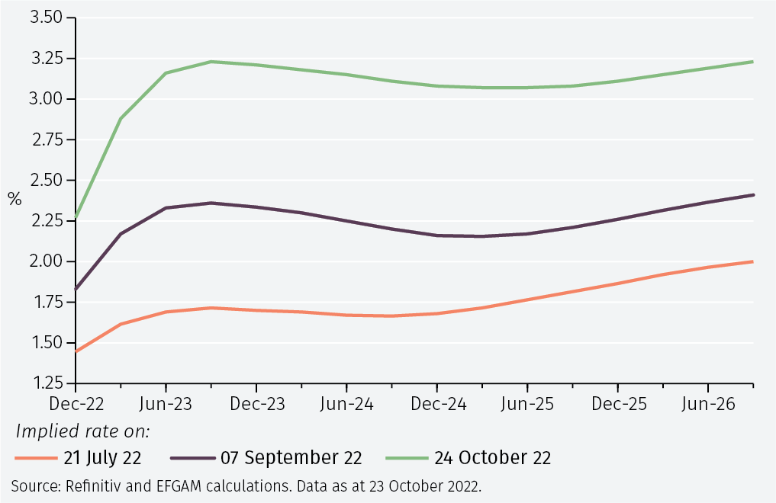

Economic growth will also be constrained by tighter ECB policy. Rate increases of 1.25% between July and September will fully impact growth by mid-2023. Growth will be further restrained by any interest rate increases from October onwards: market participants are expecting rates to reach 3.25% by 2023Q3 (see Figure 4).

Download the PDF to read the full article.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Park House, 116 Park Street, London W1K 6AP, United Kingdom, telephone +44 (0)20 7491 9111.