- Date:

Infocus - Commodity prices and inflation in developed and emerging economies

Many commentators expect inflation to increase after years of being below central banks’ objectives. Rising commodity prices, from oil to agricultural goods, underpin these fears. In this edition of Infocus, GianLuigi Mandruzzato looks at the transmission of commodity price shocks to inflation in developed and emerging countries.

The rise in government bond yields since the beginning of the year is, for many observers, a sign of an imminent increase in inflation. After having declined gradually since the early 1980s, low inflation became entrenched after the Global Financial Crisis, but its reversal may now have begun. In support of this view, some emerging countries, such as Brazil, Russia, and Turkey have already seen inflation rise and their central banks have reacted by raising interest rates.

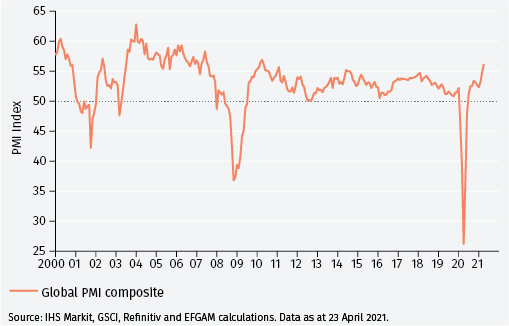

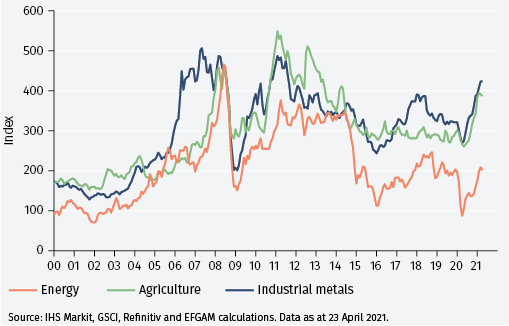

Factors behind the rise in inflation include the exceptional policy measures undertaken by central banks and governments to combat the Covid pandemic and the strong economic recovery that is underway (see Figure 1a) which has (as has been the case in recent years) been associated with rising commodity prices (see Figure 1b).

1a - Global recovery underway

1b - Commodity prices indices

How important are commodity prices for consumer prices? With a few exceptions such as some energy goods and fresh food, raw materials are not sold directly to consumers. Rather, commodities are inputs into manufactured goods that are eventually purchased by households. However, other factors, including the costs of labour and capital and taxation are more important than raw materials in setting the final selling price.

The consumption of non-essential goods and services is higher in wealthier economies, reducing the importance of food and energy purchases in total consumption. This suggests that the impact of commodity price shocks on inflation declines with the level of income and should therefore lower in developed than in emerging economies.

To assess the impact of commodity price shocks on inflation, it is useful to start from the composition of consumer price indices (CPI) in emerging and developed economies.1 The composition of the CPI baskets reflects consumers’ expenditure, as measured by sample surveys among households and are updated annually.

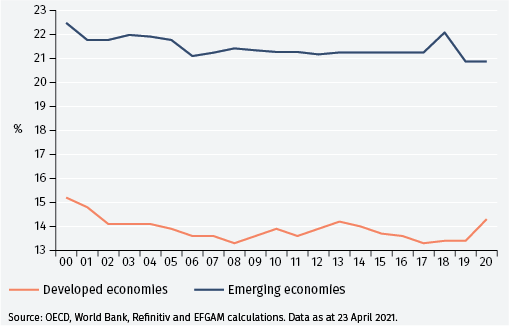

The median weight of food in the 2021 CPI basket, based on 2020 consumption, is about seven percentage points higher in emerging than in developed economies (see Figure 2a).

2a. Food median weights in CPI baskets

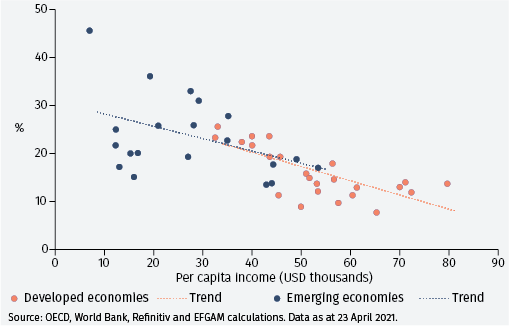

The weight of groceries has fallen since 2000 by about 2 percentage points in both groups. The rebound of the weight of food purchases in the 2021 CPI in developed countries is due to the collapse of non-primary consumption following the restrictions imposed to contain the pandemic. Figure 2b shows that the weight of food expenditure in the CPI baskets is inversely correlated to the level of per capita income across both developed and emerging economies, supporting the view that increased per capita income explains the structural decline in the weight of food purchases in CPI baskets seen in the last two decades.

2b. Income and food weight in CPI baskets

To continue reading please download the full article below.

Footnotes

1 The analysis considers data from 24 developed and 20 emerging economies. The group of developed economies includes: Australia, Austria, Belgium, Canada, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Japan, Latvia, Lithuania, Luxembourg, Netherlands, New Zealand, Norway, Portugal, Spain, Sweden, Switzerland, UK, and US.. Emerging economies group includes: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Israel, Kazakhstan, Mexico, Poland, Russia, Saudi Arabia, South Africa, South Korea, Taiwan, Thailand, and Turkey

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.