- Date:

Infocus - The Federal Minimum Wage in the US

It is customary for investors to think nationally when looking at future inflation trends. However, in this edition of Infocus, EFG Chief Economist Stefan Gerlach looks at evidence of correlation among inflation rates in individual countries and argues that they are best thought of as refecting an underlying global inflation rate.

Forecasts of inflation are important for investment management. For instance, economies in which inflation is expected to rise above the central bank’s inflation target are likely to see tighter monetary policy, leading in the short turn to a stronger exchange rate, a flattening of the yield curve and perhaps weaker equity prices. If the move is instead toward the inflation target, or seen as temporary, such reactions are less likely.

The strong correlations of inflation across countries suggest that it makes more sense to think of it as a global, rather than as a country-specific, phenomenon.1 With business cycles correlated across countries, and global energy price shocks impacting all economies to varying degrees, it is not surprising that inflation in individual countries tends to display common movements.

It is important to recognise that exchange rate flexibility does not prevent such inflation passthrough. For instance, when US dollar prices of oil rise, inflation will increase even in economies whose exchange rates are free to appreciate against the US dollar. The reason is that oil price increases are best seen as relative price changes that exchange rate changes are unable to offset.

The fact that inflation is strongly correlated between countries suggests that inflation in one country is likely to be informative of inflation in another country. It is therefore sensible to forecast inflation for a number of countries in a single, integrated step. Here data from 44 economies are studied for forecast inflation as measured by the headline consumer price index.2

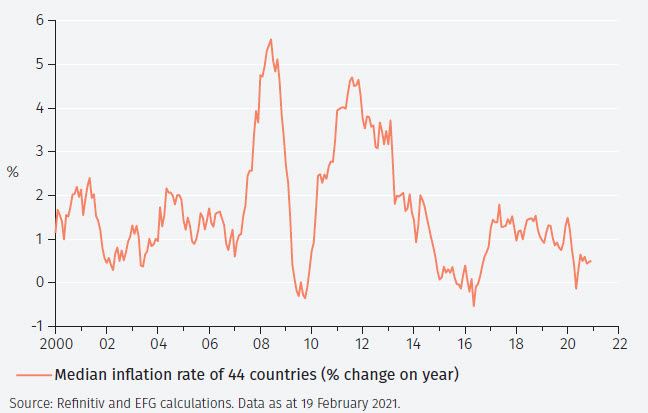

Global inflation

The first question that arises is how to capture the global component of inflation. Here we use the median inflation rate over 12 months in the 44 countries in any month. Figure 1 shows that global inflation fluctuated between 0.5 – 2% until 2007, when an increase in oil prices pushed it up to about 5.5%. The onset of the global financial crisis after the collapse of Lehman Brothers in September 2008 led economic activity, and therefore oil prices and inflation, to collapse. As the global economy recovered in 2010-11, inflation rebounded.

The model

A simple model is used to capture inflation in the 44 economies studied. Since exchange rate changes do not prevent fluctuations of inflation over a few quarters from being transmitted internationally, there is little need to incorporate exchange rate changes in the analysis. To capture the fact that inflation is correlated across countries, the median inflation rate discussed above is used.

The model holds that the domestic inflation rate (measured over 12 months) depends on its level in the previous two months, and on the global (median) inflation rate in the current and the last two months. Since many changes in inflation are better thought of as price-level shocks (for instance, due to changes in exchange rates, taxes or subsidies, or to energy prices) that drop out of the inflation rate after 12 months, the model is specified in such a way as to allow inflation to return partially or completely to its initial level after 12 months. This feature of the model implies that if inflation varied in the last 12 months, the inflation forecasts will also vary over the next 12 months, but will then settle quickly at a fixed level. (More detail about the model is available in the Technical Appendix.)

Next, we estimate the model on data from March 2000 to December 2020. Importantly, we use precisely the same model for all countries, although, of course, the parameter estimates will vary. 3

In the interest of brevity, we do not discuss these estimates. However, the results indicate that, as expected, the global inflation rate is a very important determinant of inflation in individual economies.

Historical forecasting performance

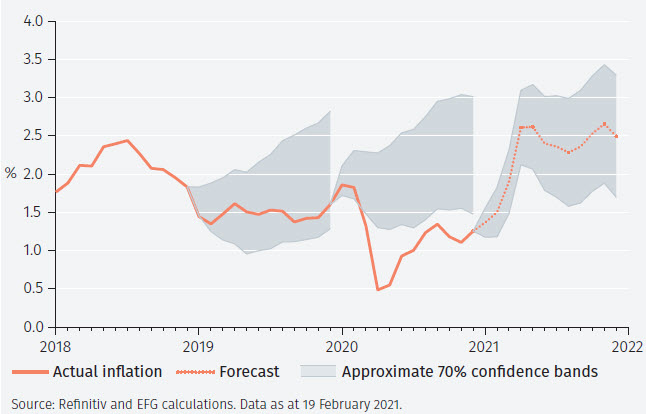

To assess the model’s forecasting performance, Figure 2 shows approximate 70% confidence bands for forecasts of US inflation for 12 months starting in January 2019, 2020 and 2021.

As one would expect, the forecasts capture base effects very well. For instance, since US inflation fell in early 2020, reaching a low in April-May, the model predicts that inflation will rise in early 2021, and reach a peak in April-May as these low observations fall out of the 12-month period used to compute inflation. Similarly, since the US inflation rate reached a second low in November 2020, the model forecasts inflation will rise in November 2021.

These forecasts are all for 12 months to avoid cluttering the graph. If longer-term forecasts had been computed, they would all have anticipated a long-run inflation rate of about 1.8%, since that is the sample average of inflation.

Overall, the figure shows that forecasts up to 12 months are largely driven by base effects.

Forecasts

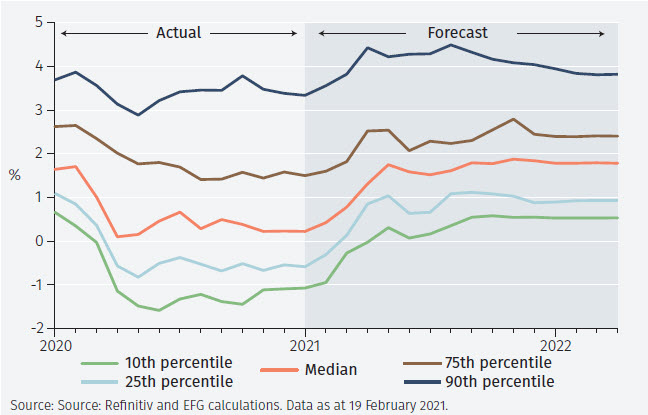

Next, we compute forecasts for all the countries in the sample for the period January 2021 – December 2022. Figure 3 shows the distribution of inflation until December 2020 and, subsequently, of forecasted inflation. The graph displays the median, together with the 10th, 25th, 75th and 90th percentiles of the distribution.

Concentrating on the median, we see that inflation declined sharply from just below 2% in early 2020 as the Covid-19 pandemic struck to just above 0%. The model views this decline as temporary and predicts that inflation will bounce back to just below 2% when these declines start to drop out of the calculation of inflation.

Looking at the results for the percentiles, we see that the entire distribution of inflation shifted lower in early 2020 and is expected to shift back higher in the coming months. This finding provides a powerful illustration of the commonalities of inflation in the group of economies studied.

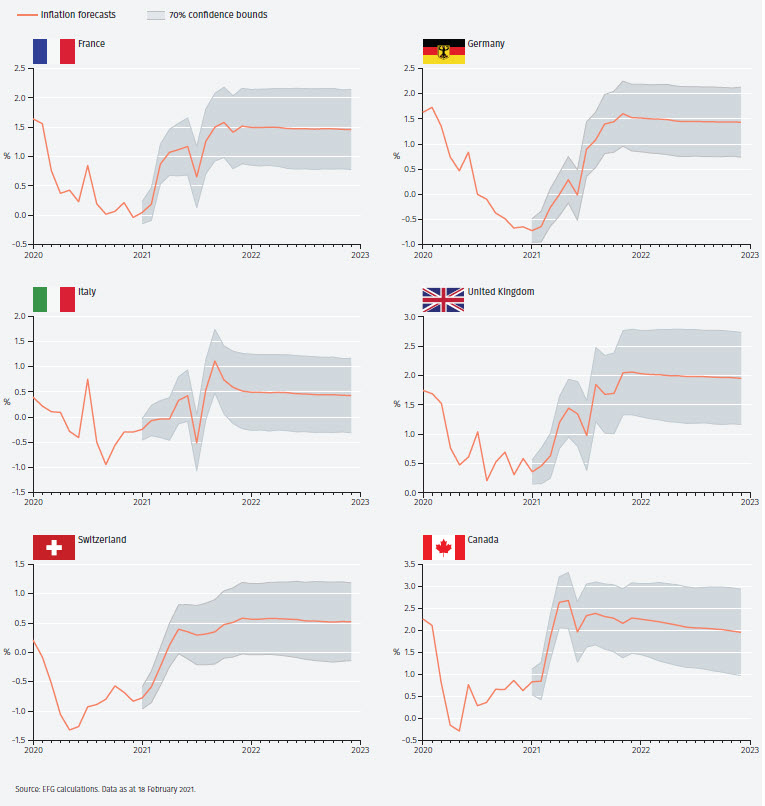

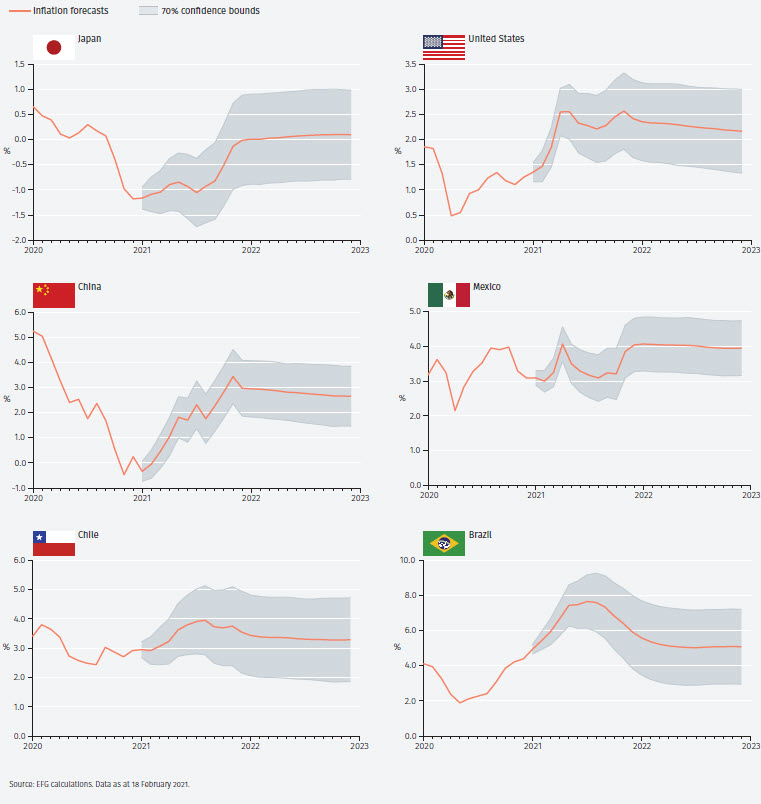

Finally, we focus on forecasts for 12 of the economies studied, together with 70% confidence bounds, shown in the panels of Figures 4 and 5. These provide a detailed view of the likely future developments of inflation in the selected economies.

Conclusions

Inflation rates are strongly correlated across individual economies, indicating that there exists something that can be thought of us an underlying global inflation rate. This finding suggests that when forecasting inflation for a group of countries, incorporating the global inflation rate in the analysis is preferable to forecasting inflation country-by-country.

Using the median inflation rate as a measure of global inflation, we compute such forecasts for a group of 44 countries for the period 2021-22. While the exact forecasts differ from country to country in light of recent inflation developments, an important common finding is that inflation is likely to rebound in the coming months. The sharp declines in inflation in the spring of 2020 related to Covid-19 will drop out of the calculations.

Footnotes

1 See Mateo Ciccarelli and Benoît Mojon (2010), ‘Global Inflation’, Review of Economics and Statistics, 92, 524-535.

2 For the US, the headline measure of the deflator for personal consumption expenditures is used.

3 With 250 observations but merely seven parameters to estimate, little would be gained in efficiency by dropping insignificant parameters.

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.