- Date:

Inview Jan 2021

Editorial

Welcome to the January edition of Inview: Global House View. In this publication we consider significant developments in the world’s markets, and discuss our key convictions and themes for the coming months.

As 2021 begins, market commentators are focusing on three matters. The first of these is the resolution of uncertainty arising from Joe Biden winning the US presential election. President Trump is still in office but his tenure will end on 20 January. While more turbulence can be expected during his last days in the White House - as shown by the riots in Washington that attempted to halt President-elect Biden’s victory certification by Congress - the four years of extraordinary confusion and uncertainty in US policy making are coming to an end. This bodes well for the world economy.

The completion of Brexit has also reduced uncertainty. While worst-case scenarios have been avoided, it is clear that the current agreement covers only a minimal range of issues. The hard job of forging broader agreements covering, in particular, services, including financial services that are of crucial importance to the UK economy, is only about to begin. Much will hinge on whether progress can be made also in these areas.

Another factor relates to the development of several vaccines against Covid 19. Since the announcement of successful late stage trials at the end of last November, risky assets have experienced a sharp rally. However, it has become apparent that the introduction of large-scale vaccination programs will be time consuming. With the virus spreading rapidly in many countries, restrictions remain in place and are generally being tightened. It seems that the situation is likely to get worse in the coming weeks and months before it gets better. This poses a downside risk to the short-term outlook for economic activity.

In addition, some commentators fear that rising inflation will complicate the recovery path from the pandemic shock. Commodity prices, including oil, industrial metals, and agricultural goods have risen strongly since last spring. Together with the recent Chinese yuan renminbi appreciation, there is a risk inflationary pressures will rise in developed countries, possibly forcing central banks to scale back stimulus. While this is not our core view it is nonetheless something we are keeping a close eye on. Fortunately current inflation measures are well below central banks’ targets in most countries and the Federal Reserve has indicated a tolerance for inflation to rise above target for a time to compensate for the amount of time inflation has spent below target. Other central banks have adopted a similarly dovish tone to their communications.

What does this environment suggest for the asset allocation of a diversified portfolio? In terms of macro asset classes, a preference for equities over bonds remains warranted even after the strong gains registered last year. Among equity markets, the US and Asia offer the most attractive prospects for the beginning of 2021. The US market is heavy in technology companies that are likely to continue to thrive as people are forced to stay at home for longer. Asian markets, will instead benefit from a faster economic recovery as the pandemic has been, so far at least, contained better there than elsewhere. Among fixed income assets, the most cyclical segments, including convertibles and sub-financials, should be favoured. Finally, to mitigate overall portfolio volatility, exposure to diversifiers like gold, the Swiss franc and the Japanese yen merits consideration.

Global Asset Allocation: Summary

Equities

- US equities continue to be favoured. Following November’s sharp rotation, value and growth stocks performed more in line with one another in December. We continue to have a preference for growth stocks, despite having greatly outperformed value in 2020, given their defensive characteristics.

- The Asia Pacific region should be favoured on a tactical and strategic basis. The region is set to benefit from the improved economic outlook, a recovery in global trade already evident in medical supplies and tech demand, and the weaker dollar.

- With no changes to our asset allocation this month we remain neutral on European equities. Economic growth in the eurozone is expected to be sluggish in the first half of the year but with Poland and Hungary removing their blocks on the EU recovery fund and a supportive ECB we could see a return in earnings confidence as the year progresses.

- Caution around EMEA markets and Latin America is still warranted. While some areas managed to maintain November’s momentum it is hard to see how this can be sustained with a slower recovery.

- All sectors are in an uptrend and relative momentum remains unchanged favouring consumer discretionary, healthcare, and technology.

Fixed Income

- Within fixed income, convertibles again have been a strong performer for the month and the standout for the year as a whole. While we recognise that the rally has been rapid and upside is now more subdued we still favour convertible bonds.

- Spreads have tightened sharply particularly in the higher quality segments with central banks reaffirming their accommodative policy stances. We are neutral on investment grade and high yield bonds.

- Within emerging market bonds we continue to prefer hard currency over local currency, although the weaker dollar could make local currency debt more enticing and encourage us to raise our neutral allocation should the moment arise.

Alternative Investments

- We are strategically and tactical overweight uncorrelated hedge funds. Macro managers offer portfolio diversification while periods of heightened volatility make for a healthy environment for short-term focused CTAs.

- Tactically we are cautious on carry/credit managers with any focus being on convertible arbitrage managers. The broad convertible universe still remains cheap relative to fair value estimates and convertible arbitrage managers are also actively engaging with issuers to fix balance sheets and participating in buybacks.

- Infrastructure remains underweight, waiting for the economic recovery to take pace before we look to upgrade.

Currencies

- The euro has managed to extend its rally against the US dollar and PPP estimates indicate that there is still room for further dollar weakening. We are tactically overweight on the euro.

- While a Brexit agreement has been reached further details need clarification. Also, with ongoing Covid restrictions this somewhat limits growth prospects, so for the time being we are neutral on the pound.

- Right now we are cautiously underweight the Swiss franc - the currency may weaken through 2021 as the global recovery takes shape and volatility abates.

Global Asset Allocation: 12-Month Strategic Outlook

Based on a balanced mandate, the matrix below shows our long-term house view on investment strategy.

Overall Asset Allocation Views

Asset Class Breadown

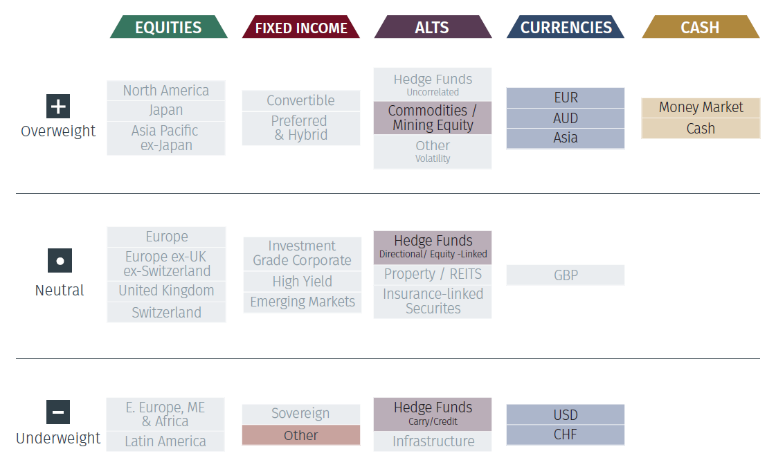

Global Asset Allocation: 3-Month Tactical Outlook

Based on a balanced mandate, the matrix below shows our short-term house view on investment strategy.

Note: The highlighted boxes indicate a difference from our 12-month strategic outlook.

Asset Class Breakdown

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.

ASSET ALLOCATION GRIDS

Please use the button below to download the full article to see asset allocation grids.