- Date:

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed.

The recent burst of inflation in the US and in many other countries has led investors to wonder whether the entire inflation environment has changed. In this Macro Flash Note EFG chief economist Stefan Gerlach looks at the US evidence and argues that, over the last 70 years, surges in inflation have been followed by collapses over the next two years.

The recent surge in inflation has unsettled investors. With US CPI inflation rising from 1.2% in 2020Q4 to 6.7% in 2021Q1, and up to 7.9% in February 2022, that is not surprising. A key concern is whether inflation will plateau at a permanently higher level. If so, that would have direct implications for a range of assets, in particular bond yields and exchange rates.

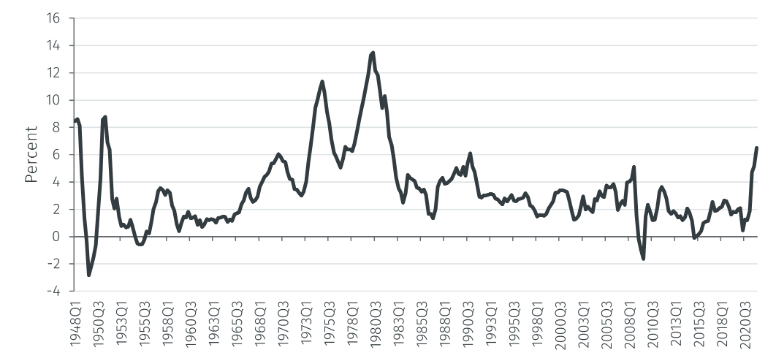

In thinking about this question, it is useful to review the behaviour of inflation in the US, for which current data series for the consumer price index (CPI) is available since 1947. Figure 1 below shows inflation over four quarters.1

Source: Fred, data as of 23 March 2022

Overall, the figure shows that with the notable exception of the period 1973-83, inflation has largely fluctuated in the 0-4% range. That said, there have been several episodes of surging inflation. It surged in the aftermath of World War II as wartime restrictions were ended and pent-up demand led to sharp rises in prices to a new equilibrium level. It increased sharply during the Korean war in 1950-53 and rose gradually in the late 1960s during the war in Vietnam as government spending rose sharply. Two notable features of the figure are the oil price shocks in 1973-74 and 1979-80, which caused inflation to rise above 10% per annum. And, finally, inflation rose dramatically in 2021.

Interestingly, the figure also shows that sharp rises in inflation appear to be followed after some time by a decline. The brief period of deflation in 1949-50 is a case in point. To study the behaviour of inflation around these episodes, the notion of a “surge” must be clarified. Here it is defined as an annual change of year-over-year inflation of at least three percentage points. Since investor concerns are triggered by a seemingly relentless increase in inflation, the criterion must be satisfied for at least two quarters in a row.

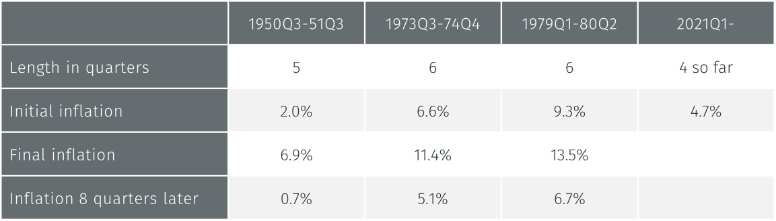

As shown in the table below (and in Figure 2), that definition leads to four inflation surge episodes, staring in 1950, 1973, 1979 and 2021. That on its own is striking – inflation surges are rare events. That, in turn, means that there are few data points, which makes it difficult to draw firm conclusions.

Source: EFG calculations.

It is notable that the inflation surges identified in this period have typically lasted a little more than a year and involved inflation rising by about 5 percentage points. They have thus been a little longer and have involved larger increases in inflation than we have seen in the current episode.

But the key finding is clear: they have been followed by large declines – if not collapses – in inflation.

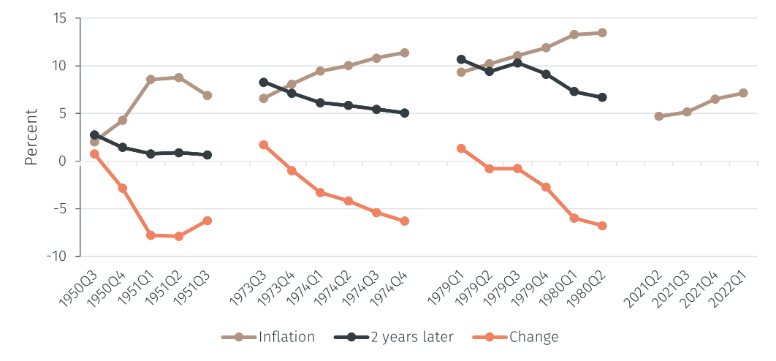

Source: EFG calculations.

This brief review of inflation surges in the US since the late 1940s tells they are rare events, typically last 5-6 quarters and are temporary in that they are followed by a large decline of inflation. Of course, the rarity of such surges implies that little is known about them. There is thus no guarantee that the current surge will conform to the historical record.

1 Inflation is continuously compounded

Important Information

The value of investments and the income derived from them can fall as well as rise, and past performance is no indicator of future performance. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested.

This document does not constitute and shall not be construed as a prospectus, advertisement, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation or particular needs of the recipient. You should seek your own professional advice suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.

Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information may be incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.

The availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.